1 Name

This instrument is the Customs Amendment (Product Specific Rule Modernisation) Regulations 2021.

2 Commencement

(1) Each provision of this instrument specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information |

Column 1 | Column 2 | Column 3 |

Provisions | Commencement | Date/Details |

1. The whole of this instrument | At the same time as the Customs Amendment (Product Specific Rule Modernisation) Act 2021 commences. | 9 April 2021 |

Note: This table relates only to the provisions of this instrument as originally made. It will not be amended to deal with any later amendments of this instrument.

(2) Any information in column 3 of the table is not part of this instrument. Information may be inserted in this column, or information in it may be edited, in any published version of this instrument.

3 Authority

This instrument is made under the Customs Act 1901.

4 Schedules

Each instrument that is specified in a Schedule to this instrument is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this instrument has effect according to its terms.

Schedule 1—Amendments

Part 1—US originating goods

Customs (Australia–US Free Trade Agreement) Regulations 2004

1 Regulation 1.3

Repeal the regulation, substitute:

1.3 Authority

These Regulations are made under the Customs Act 1901.

1.4 Definitions

In these Regulations:

Act means the Customs Act 1901.

Agreement has the meaning given by section 153YA of the Act.

Agreement on Implementation of Article VII of the General Agreement on Tariffs and Trade 1994 means the Agreement of that name set out in Annex 1A of the Marrakesh Agreement Establishing the World Trade Organization, done at Marrakesh on 15 April 1994.

Note: The Marrakesh Agreement Establishing the World Trade Organization is in Australian Treaty Series 1995 No. 8 ([1995] ATS 8) and could in 2021 be viewed in the Australian Treaties Library on the AustLII website (http://www.austlii.edu.au).

non‑originating materials has the meaning given by section 153YA of the Act.

originating materials has the meaning given by section 153YA of the Act.

produce has the meaning given by section 153YA of the Act.

US means the United States of America.

used has the meaning given by section 153YA of the Act.

2 Parts 2 to 5

Repeal the Parts, substitute:

Part 2—Tariff change requirement

2.1 Change in tariff classification requirement for non‑originating materials

For the purposes of subsection 153YD(3) of the Act, a non‑originating material used in the production of goods that does not satisfy a particular change in tariff classification is taken to satisfy the change in tariff classification if:

(a) it was produced entirely in the US, or entirely in the US and Australia, from other non‑originating materials; and

(b) each of those other non‑originating materials satisfies the change in tariff classification, including by one or more applications of this regulation.

Part 3—Regional value content requirement

3.1 Build‑down method

(1) For the purposes of subsection 153YD(7) of the Act, the regional value content of goods under the build‑down method is worked out using the formula:

where:

customs value means the customs value of the goods worked out under Division 2 of Part VIII of the Act.

value of non‑originating materials means the value, worked out under Part 4, of the non‑originating materials that are acquired by the producer and are used by the producer in the production of the goods, other than non‑originating materials produced by the producer.

(2) Regional value content must be expressed as a percentage.

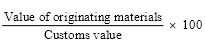

3.2 Build‑up method

(1) For the purposes of subsection 153YD(7) of the Act, the regional value content of goods under the build‑up method is worked out using the formula:

where:

customs value means the customs value of the goods worked out under Division 2 of Part VIII of the Act.

value of originating materials means the value, worked out under Part 4, of the originating materials that are acquired by the producer, or produced by the producer, and are used by the producer in the production of the goods.

(2) Regional value content must be expressed as a percentage.

3.3 Net cost method

(1) For the purposes of subsection 153YD(7) of the Act, the regional value content of goods under the net cost method is worked out using the formula:

where:

net cost means the net cost of the goods worked out in accordance with Articles 5.4 and 5.18 of the Agreement.

value of non‑originating materials means the value, worked out under Part 4, of the non‑originating materials that are acquired by the producer and are used by the producer in the production of the goods, other than non‑originating materials produced by the producer.

(2) Regional value content must be expressed as a percentage.

Part 4—Determination of value

4.1 Value of goods that are originating materials or non‑originating materials

(1) For the purposes of subsection 153YA(2) of the Act, this regulation explains how to work out the value of originating materials or non‑originating materials used in the production of goods.

(2) The value of the materials is as follows:

(a) for materials imported into the US by the producer of the goods—the value of the materials worked out in accordance with the Agreement on Implementation of Article VII of the General Agreement on Tariffs and Trade 1994;

(b) for materials acquired in the US—the value of those materials worked out under paragraph (a) on the assumption that those materials had been imported into the US;

(c) for materials that are produced by the producer of the goods—the sum of:

(i) all the costs incurred in the production of the materials, including general expenses; and

(ii) an amount that is the equivalent of the amount of profit that the producer would make for the materials in the normal course of trade.

(3) In working out the value of particular originating materials under subregulation (2), the following may be included, to the extent that they have not been taken into account under that subregulation:

(a) the costs of freight, insurance, packing and all other costs incurred to transport the materials within the US, or between Australia and the US, to the location of the producer of the goods;

(b) duties, taxes and customs brokerage fees on the materials that:

(i) have been paid in either or both of the US and Australia; and

(ii) have not been waived or refunded; and

(iii) are not refundable or otherwise recoverable;

including any credit against duties or taxes that have been paid or that are payable;

(c) the costs of waste and spoilage resulting from the use of the materials in the production of the goods, reduced by the value of renewable scrap or by‑products.

(4) In working out the value of particular non‑originating materials under subregulation (2), the following may be deducted if they were included under that subregulation:

(a) the costs of freight, insurance, packing and all other costs incurred to transport the non‑originating materials within the US, or between Australia and the US, to the location of the producer of the goods;

(b) duties, taxes and customs brokerage fees on the non‑originating materials that:

(i) have been paid in either or both of the US and Australia; and

(ii) have not been waived or refunded; and

(iii) are not refundable or otherwise recoverable;

including any credit against duties or taxes that have been paid or that are payable;

(c) the costs of waste and spoilage resulting from the use of the non‑originating materials in the production of the goods, reduced by the value of renewable scrap or by‑products;

(d) the costs of processing incurred in either or both of the US and Australia in the production of the non‑originating materials;

(e) the costs of originating materials used in the production of the non‑originating materials in either or both of the US and Australia.

4.2 Value of accessories, spare parts or tools

If paragraphs 153YD(8)(a), (b), (c) and (d) of the Act are satisfied in relation to goods:

(a) the value of the accessories, spare parts or tools must be taken into account for the purposes of working out the regional value content of the goods under Part 3 of these Regulations; and

(b) if the accessories, spare parts or tools are non‑originating materials—for the purposes of Part 3 of these Regulations and regulation 4.1, those accessories, spare parts or tools are taken to be non‑originating materials used in the production of the goods; and

(c) if the accessories, spare parts or tools are originating materials—for the purposes of Part 3 of these Regulations and regulation 4.1, those accessories, spare parts or tools are taken to be originating materials used in the production of the goods.

4.3 Value of packaging material and container

If paragraphs 153YK(1)(a) and (b) of the Act are satisfied in relation to goods and the goods must have a regional value content of not less than a particular percentage worked out in a particular way:

(a) the value of the packaging material or container in which the goods are packaged must be taken into account for the purposes of working out the regional value content of the goods under Part 3 of these Regulations; and

(b) if that packaging material or container is a non‑originating material—for the purposes of Part 3 of these Regulations and regulation 4.1, that packaging material or container is taken to be a non‑originating material used in the production of the goods; and

(c) if that packaging material or container is an originating material—for the purposes of Part 3 of these Regulations and regulation 4.1, that packaging material or container is taken to be an originating material used in the production of the goods.

3 Schedules 1 and 2

Repeal the Schedules.

Part 2—Thai originating goods

Customs (Thailand–Australia Free Trade Agreement) Regulations 2004

4 Regulation 1.3

Repeal the regulation, substitute:

1.3 Authority

These Regulations are made under the Customs Act 1901.

1.4 Definitions

In these Regulations:

Act means the Customs Act 1901.

Agreement on Implementation of Article VII of the General Agreement on Tariffs and Trade 1994 means the Agreement of that name set out in Annex 1A of the Marrakesh Agreement Establishing the World Trade Organization, done at Marrakesh on 15 April 1994.

Note: The Marrakesh Agreement Establishing the World Trade Organization is in Australian Treaty Series 1995 No. 8 ([1995] ATS 8) and could in 2021 be viewed in the Australian Treaties Library on the AustLII website (http://www.austlii.edu.au).

developing country means a country or place listed in Schedule 1 to the Customs Tariff Act 1995, as that Act was in force on 1 January 2005.

Harmonized System has the meaning given by section 153ZA of the Act.

non‑originating materials has the meaning given by section 153ZA of the Act.

originating materials has the meaning given by section 153ZA of the Act.

produce has the meaning given by section 153ZA of the Act.

5 Parts 2 to 4

Repeal the Parts, substitute:

Part 2—Tariff change requirement

2.1 Change in tariff classification requirement for non‑originating materials

For the purposes of subsection 153ZC(3) of the Act, a non‑originating material used in the production of goods that does not satisfy a particular change in tariff classification is taken to satisfy the change in tariff classification if:

(a) it was produced entirely in Thailand, or entirely in Thailand and Australia, from other non‑originating materials; and

(b) each of those other non‑originating materials satisfies the change in tariff classification, including by one or more applications of this regulation.

Part 3—Regional value content requirement

3.1 Regional value content requirement

(1) For the purposes of subsection 153ZC(5) of the Act, the regional value content of goods is worked out using the formula:

where:

customs value means the customs value of the goods worked out under Division 2 of Part VIII of the Act.

value of non‑originating materials means the sum of the value, worked out under Part 4, of the following:

(a) non‑originating materials:

(i) imported into Thailand by the producer of the goods; and

(ii) used in the production of the goods;

(b) non‑originating materials:

(i) imported into Thailand and acquired, in the form in which they were imported, by the producer of the goods; and

(ii) used in the production of the goods;

(c) non‑originating materials imported into Thailand by a producer in Thailand of other non‑originating materials, where the other non‑originating materials:

(i) are produced using the imported non‑originating materials; and

(ii) are supplied directly to the producer of the goods; and

(iii) are used in the production of the goods;

(d) non‑originating materials imported into Thailand and acquired, in the form in which they were imported, by a producer in Thailand of other non‑originating materials, where the other non‑originating materials:

(i) are produced using the imported non‑originating materials; and

(ii) are supplied directly to the producer of the goods; and

(iii) are used in the production of the goods.

(2) Regional value content must be expressed as a percentage.

(3) For the purposes of working out the regional value content of goods under subregulation (1), if:

(a) the goods are classified to any of Chapters 50 to 64 of the Harmonized System; and

(b) non‑originating materials produced in one or more developing countries are used in the production of the goods;

the value of those non‑originating materials may be subtracted from the total value of non‑originating materials used in the production of the goods (up to an amount that is 25% of the customs value of the goods worked out under Division 2 of Part VIII of the Act).

(4) Subregulation (3) ceases to have effect at the end of 31 December 2024.

Part 4—Determination of value

4.1 Value of goods that are non‑originating materials

(1) For the purposes of subsection 153ZA(2) of the Act, the value of non‑originating materials is the value of the materials worked out in accordance with the Agreement on Implementation of Article VII of the General Agreement on Tariffs and Trade 1994.

(2) In working out the value of particular non‑originating materials under subregulation (1), the following must be included, to the extent that they have not been taken into account under that subregulation:

(a) the cost of transporting the non‑originating materials to Thailand from their country of export;

(b) the cost of insurance and other services related to that transport.

4.2 Value of accessories, spare parts or tools

If paragraphs 153ZC(6)(a), (b), (c), (d), (e) and (f) of the Act are satisfied in relation to goods:

(a) the value of the accessories, spare parts or tools covered by paragraph 153ZC(6)(f) of the Act must be taken into account for the purposes of working out the regional value content of the goods under regulation 3.1; and

(b) for the purposes of regulations 3.1 and 4.1, those accessories, spare parts or tools are taken to be non‑originating materials used in the production of the goods.

4.3 Value of packaging material and container

If paragraphs 153ZG(2)(a) and (b) of the Act are satisfied in relation to goods:

(a) the value of the packaging material or container in which the goods are packaged must be taken into account for the purposes of working out the regional value content of the goods under regulation 3.1; and

(b) for the purposes of regulations 3.1 and 4.1, that packaging material or container is taken to be a non‑originating material used in the production of the goods.

6 Schedule 1

Repeal the Schedule.

Part 3—New Zealand originating goods

Customs (New Zealand Rules of Origin) Regulations 2006

7 Regulation 1.3

Repeal the regulation, substitute:

1.3 Authority

These Regulations are made under the Customs Act 1901.

1.4 Definitions

In these Regulations:

Act means the Customs Act 1901.

Agreement has the meaning given by section 153ZIB of the Act.

Agreement on Implementation of Article VII of the General Agreement on Tariffs and Trade 1994 means the Agreement of that name set out in Annex 1A of the Marrakesh Agreement Establishing the World Trade Organization, done at Marrakesh on 15 April 1994.

Note: The Marrakesh Agreement Establishing the World Trade Organization is in Australian Treaty Series 1995 No. 8 ([1995] ATS 8) and could in 2021 be viewed in the Australian Treaties Library on the AustLII website (http://www.austlii.edu.au).

non‑originating materials has the meaning given by section 153ZIB of the Act.

originating materials has the meaning given by section 153ZIB of the Act.

produce has the meaning given by section 153ZIB of the Act.

8 Parts 2 to 5

Repeal the Parts, substitute:

Part 2—Tariff change requirement

2.1 Change in tariff classification requirement for non‑originating materials

For the purposes of subsection 153ZIE(3) of the Act, a non‑originating material used or consumed in the production of goods that does not satisfy a particular change in tariff classification is taken to satisfy the change in tariff classification if:

(a) it was produced entirely in New Zealand, or entirely in New Zealand and Australia, from other non‑originating materials; and

(b) each of those other non‑originating materials satisfies the change in tariff classification, including by one or more applications of this regulation.

Part 3—Regional value content requirement

3.1 Build‑down method

(1) For the purposes of subsection 153ZIE(5) of the Act, the regional value content of goods under the build‑down method is worked out using the formula:

where:

customs value means the customs value of the goods worked out under Division 2 of Part VIII of the Act.

value of non‑originating materials means the value, worked out under Part 4, of the non‑originating materials that are acquired by the producer and are used or consumed by the producer in the production of the goods, other than non‑originating materials produced by the producer.

(2) Regional value content must be expressed as a percentage.

3.2 Build‑up method

(1) For the purposes of subsection 153ZIE(5) of the Act, the regional value content of goods under the build‑up method is worked out using the formula:

where:

customs value means the customs value of the goods worked out under Division 2 of Part VIII of the Act.

value of originating materials means the value, worked out under Part 4, of the originating materials that are acquired by the producer, or produced by the producer, and are used or consumed by the producer in the production of the goods.

(2) Regional value content must be expressed as a percentage.

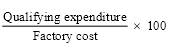

3.3 Factory cost method

(1) For the purposes of subsection 153ZIE(5) of the Act, the regional value content of goods under the factory cost method is worked out using the formula:

where:

factory cost means the factory cost of producing the goods worked out in accordance with paragraph 5 of Article 3 of the Agreement.

qualifying expenditure means the qualifying expenditure on the goods worked out in accordance with paragraph 5 of Article 3 of the Agreement.

(2) Regional value content must be expressed as a percentage.

Part 4—Determination of value

4.1 Value of goods that are originating materials or non‑originating materials

(1) For the purposes of subsection 153ZIB(3) of the Act, this regulation explains how to work out the value of originating materials or non‑originating materials used or consumed in the production of goods.

(2) The value of the materials is as follows:

(a) for materials imported into New Zealand by the producer of the goods—the value of the materials worked out in accordance with the Agreement on Implementation of Article VII of the General Agreement on Tariffs and Trade 1994;

(b) for materials acquired in New Zealand—the sum of:

(i) the cost of acquisition; and

(ii) the cost of transporting the materials to the producer of the goods, where that cost is not included in the cost of acquisition;

(c) for materials that are produced by the producer of the goods—the sum of:

(i) all the costs incurred in the production of the materials, including general expenses; and

(ii) an amount that is the equivalent of the amount of profit that the producer would make for the materials in the normal course of trade.

(3) In working out the value of particular originating materials under subregulation (2), the following may be included, to the extent that they have not been taken into account under that subregulation:

(a) the costs of freight, insurance, packing and all other costs incurred to transport the materials within New Zealand, or between Australia and New Zealand, to the location of the producer of the goods;

(b) duties, taxes and customs brokerage fees on the materials that:

(i) have been paid in either or both of New Zealand and Australia; and

(ii) have not been waived or refunded; and

(iii) are not refundable or otherwise recoverable;

including any credit against duties or taxes that have been paid or that are payable;

(c) the costs of waste and spoilage resulting from the use of the materials in the production of the goods, reduced by the value of renewable scrap or by‑products.

(4) In working out the value of particular non‑originating materials under subregulation (2), the following are to be deducted if they were included under that subregulation:

(a) the costs of freight, insurance, packing and all other costs incurred to transport the non‑originating materials within New Zealand, or between Australia and New Zealand, to the location of the producer of the goods;

(b) duties, taxes and customs brokerage fees on the non‑originating materials that:

(i) have been paid in either or both of New Zealand and Australia; and

(ii) have not been waived or refunded; and

(iii) are not refundable or otherwise recoverable;

including any credit against duties or taxes that have been paid or that are payable;

(c) the costs of waste and spoilage resulting from the use of the non‑originating materials in the production of the goods, reduced by the value of renewable scrap or by‑products;

(d) the costs of processing incurred in either or both of New Zealand and Australia in the production of the non‑originating materials;

(e) the costs of originating materials used or consumed in the production of the non‑originating materials in either or both of New Zealand and Australia.

4.2 Value of accessories, spare parts or tools

If paragraphs 153ZIE(6)(a), (b), (c), (d) and (e) of the Act are satisfied in relation to goods:

(a) the value of the accessories, spare parts or tools must be taken into account for the purposes of working out the regional value content of the goods under Part 3 of these Regulations; and

(b) if the accessories, spare parts or tools are non‑originating materials—for the purposes of Part 3 of these Regulations and regulation 4.1, those accessories, spare parts or tools are taken to be non‑originating materials used or consumed in the production of the goods; and

(c) if the accessories, spare parts or tools are originating materials—for the purposes of Part 3 of these Regulations and regulation 4.1, those accessories, spare parts or tools are taken to be originating materials used or consumed in the production of the goods.

4.3 Value of packaging material and container

If paragraphs 153ZIF(1)(a) and (b) of the Act are satisfied in relation to goods and the goods must have a regional value content of not less than a particular percentage worked out in a particular way:

(a) the value of the packaging material or container in which the goods are packaged must be taken into account for the purposes of working out the regional value content of the goods under Part 3 of these Regulations; and

(b) if that packaging material or container is a non‑originating material—for the purposes of Part 3 of these Regulations and regulation 4.1, that packaging material or container is taken to be a non‑originating material used or consumed in the production of the goods; and

(c) if that packaging material or container is an originating material—for the purposes of Part 3 of these Regulations and regulation 4.1, that packaging material or container is taken to be an originating material used or consumed in the production of the goods.

9 Schedule 1

Repeal the Schedule.

Part 4—Chilean originating goods

Customs (Chilean Rules of Origin) Regulations 2008

10 Regulation 1.3

Repeal the regulation, substitute:

1.3 Authority

These Regulations are made under the Customs Act 1901.

1.4 Definitions

In these Regulations:

Act means the Customs Act 1901.

Agreement on Implementation of Article VII of the General Agreement on Tariffs and Trade 1994 means the Agreement of that name set out in Annex 1A of the Marrakesh Agreement Establishing the World Trade Organization, done at Marrakesh on 15 April 1994.

Note: The Marrakesh Agreement Establishing the World Trade Organization is in Australian Treaty Series 1995 No. 8 ([1995] ATS 8) and could in 2021 be viewed in the Australian Treaties Library on the AustLII website (http://www.austlii.edu.au).

non‑originating materials has the meaning given by section 153ZJB of the Act.

originating materials has the meaning given by section 153ZJB of the Act.

produce has the meaning given by section 153ZJB of the Act.

territory of Australia has the meaning given by section 153ZJB of the Act.

territory of Chile has the meaning given by section 153ZJB of the Act.

11 Parts 2 to 4

Repeal the Parts, substitute:

Part 2—Tariff change requirement

2.1 Change in tariff classification requirement for non‑originating materials

For the purposes of subsection 153ZJE(3) of the Act, a non‑originating material used in the production of goods that does not satisfy a particular change in tariff classification is taken to satisfy the change in tariff classification if:

(a) it was produced entirely in the territory of Chile, or entirely in the territory of Chile and the territory of Australia, from other non‑originating materials; and

(b) each of those other non‑originating materials satisfies the change in tariff classification, including by one or more applications of this regulation.

Part 3—Regional value content requirement

3.1 Regional value content requirement

(1) For the purposes of subsection 153ZJE(5) of the Act, the regional value content of goods is worked out using the formula:

where:

customs value means the customs value of the goods worked out under Division 2 of Part VIII of the Act.

value of non‑originating materials means the value, worked out under Part 4, of the non‑originating materials that are acquired by the producer and are used by the producer in the production of the goods, other than non‑originating materials produced by the producer.

(2) Regional value content must be expressed as a percentage.

Part 4—Determination of value

4.1 Value of goods that are non‑originating materials

(1) For the purposes of subsection 153ZJB(3) of the Act, the value of non‑originating materials used in the production of goods is:

(a) for non‑originating materials imported into the territory of Chile by the producer of the goods—the value of the materials worked out in accordance with the Agreement on Implementation of Article VII of the General Agreement on Tariffs and Trade 1994; or

(b) for non‑originating materials acquired in the territory of Chile—the value of those materials worked out under paragraph (a) on the assumption that those materials had been imported into the territory of Chile.

(2) For the purposes of paragraph (1)(a), in working out the value of particular non‑originating materials, the following are to be deducted:

(a) the costs of freight, insurance, packing and all other costs incurred to transport the non‑originating materials within the territory of Chile to the location of the producer of the goods;

(b) duties, taxes and customs brokerage fees on the non‑originating materials that:

(i) have been paid in the territory of Chile; and

(ii) have not been waived or refunded; and

(iii) are not refundable or otherwise recoverable;

including any credit against duties or taxes that have been paid or that are payable;

(c) if the non‑originating materials were imported from the territory of Australia:

(i) the costs of waste and spoilage resulting from the use of the non‑originating materials in the production of the goods in the territory of Chile;

(ii) the costs of processing incurred in the territory of Australia in the production of the non‑originating materials;

(iii) the costs of originating materials used in the production of the non‑originating materials in the territory of Australia.

(3) For the purposes of paragraph (1)(b), in working out the value of particular non‑originating materials, the following are to be deducted:

(a) the costs of freight, insurance, packing and all other costs incurred to transport the non‑originating materials within the territory of Chile to the location of the producer of the goods;

(b) duties, taxes and customs brokerage fees on the non‑originating materials that:

(i) have been paid in the territory of Chile; and

(ii) have not been waived or refunded; and

(iii) are not refundable or otherwise recoverable;

including any credit against duties or taxes that have been paid or that are payable;

(c) the costs of waste and spoilage resulting from the use of the non‑originating materials in the production of the goods in the territory of Chile;

(d) the costs of processing incurred in either or both of the territory of Chile and the territory of Australia in the production of the non‑originating materials;

(e) the costs of originating materials used in the production of the non‑originating materials in either or both of the territory of Chile and the territory of Australia.

4.2 Value of accessories, spare parts, tools or instructional or other information resources

If paragraphs 153ZJE(6)(a), (b), (c), (d) and (e) of the Act are satisfied in relation to goods:

(a) the value of the accessories, spare parts, tools or instructional or other information resources covered by paragraph 153ZJE(6)(e) of the Act must be taken into account for the purposes of working out the regional value content of the goods under regulation 3.1; and

(b) for the purposes of regulations 3.1 and 4.1, those accessories, spare parts, tools or instructional or other information resources are taken to be non‑originating materials used in the production of the goods.

4.3 Value of packaging material and container

If paragraphs 153ZJF(2)(a) and (b) of the Act are satisfied in relation to goods:

(a) the value of the packaging material or container in which the goods are packaged must be taken into account for the purposes of working out the regional value content of the goods under regulation 3.1; and

(b) for the purposes of regulations 3.1 and 4.1, that packaging material or container is taken to be a non‑originating material used in the production of the goods.

12 Schedule 1

Repeal the Schedule.

Part 5—Malaysian originating goods

Customs (Malaysian Rules of Origin) Regulation 2012

13 Section 1.3

Repeal the section, substitute:

1.3 Authority

This regulation is made under the Customs Act 1901.

1.4 Definitions

In this regulation:

Act means the Customs Act 1901.

Agreement has the meaning given by section 153ZLB of the Act.

Agreement on Implementation of Article VII of the General Agreement on Tariffs and Trade 1994 means the Agreement of that name set out in Annex 1A of the Marrakesh Agreement Establishing the World Trade Organization, done at Marrakesh on 15 April 1994.

Note: The Marrakesh Agreement Establishing the World Trade Organization is in Australian Treaty Series 1995 No. 8 ([1995] ATS 8) and could in 2021 be viewed in the Australian Treaties Library on the AustLII website (http://www.austlii.edu.au).

Australian originating goods has the meaning given by section 153ZLB of the Act.

Declaration of Origin has the meaning given by section 153ZLB of the Act.

Harmonized System has the meaning given by section 153ZLB of the Act.

non‑originating materials has the meaning given by section 153ZLB of the Act.

originating materials has the meaning given by section 153ZLB of the Act.

produce has the meaning given by section 153ZLB of the Act.

territory of Australia has the meaning given by section 153ZLB of the Act.

territory of Malaysia has the meaning given by section 153ZLB of the Act.

14 Parts 2 to 4

Repeal the Parts, substitute:

Part 2—Tariff change requirement

2.1 Change in tariff classification requirement for non‑originating materials

For the purposes of subsection 153ZLE(3) of the Act, a non‑originating material used in the production of goods that does not satisfy a particular change in tariff classification is taken to satisfy the change in tariff classification if:

(a) it was produced entirely in the territory of Malaysia, or entirely in the territory of Malaysia and the territory of Australia, from other non‑originating materials; and

(b) each of those other non‑originating materials satisfies the change in tariff classification, including by one or more applications of this section.

Part 3—Regional value content requirement

3.1 Build‑down method

(1) For the purposes of subsection 153ZLE(6) of the Act, the regional value content of goods under the build‑down method is worked out using the formula:

where:

customs value means the customs value of the goods worked out under Division 2 of Part VIII of the Act.

value of non‑originating materials means the value, worked out under Part 4, of the non‑originating materials used in the production of the goods.

(2) Regional value content must be expressed as a percentage.

3.2 Build‑up method

(1) For the purposes of subsection 153ZLE(6) of the Act, the regional value content of goods under the build‑up method is worked out using the formula:

where:

customs value means the customs value of the goods worked out under Division 2 of Part VIII of the Act.

value of originating materials means the value, worked out under Part 4, of the originating materials that are acquired by the producer, or produced by the producer, and are used by the producer in the production of the goods.

(2) Regional value content must be expressed as a percentage.

Part 4—Determination of value

4.1 Value of goods that are originating materials or non‑originating materials

(1) For the purposes of subsection 153ZLB(3) of the Act, this section explains how to work out the value of originating materials or non‑originating materials used in the production of goods.

(2) The value of the materials is as follows:

(a) for materials imported into the territory of Malaysia by the producer of the goods—the value of the materials worked out in accordance with the Agreement on Implementation of Article VII of the General Agreement on Tariffs and Trade 1994;

(b) for materials acquired in the territory of Malaysia—the earliest ascertainable price paid or payable for the materials;

(c) for materials that are produced by the producer of the goods—the sum of:

(i) all the costs incurred in the production of the materials, including general expenses; and

(ii) an amount that is the equivalent of the amount of profit that the producer would make for the materials in the normal course of trade.

(3) In working out the value of particular originating materials under subsection (2), the following may be included, to the extent that they have not been taken into account under that subsection:

(a) the costs of freight, insurance, packing and all other costs incurred to transport the materials within the territory of Malaysia, or between the territory of Australia and the territory of Malaysia, to the location of the producer of the goods;

(b) duties, taxes and customs brokerage fees on the materials that:

(i) have been paid in either or both of the territory of Malaysia and the territory of Australia; and

(ii) have not been waived or refunded; and

(iii) are not refundable or otherwise recoverable;

including any credit against duties or taxes that have been paid or that are payable;

(c) the costs of waste and spoilage resulting from the use of the materials in the production of the goods, reduced by the value of renewable scrap or by‑products.

(4) In working out the value of particular non‑originating materials under subsection (2), the following may be deducted if they were included under that subsection:

(a) the costs of freight, insurance, packing and all other costs incurred to transport the non‑originating materials within the territory of Malaysia, or between the territory of Australia and the territory of Malaysia, to the location of the producer of the goods;

(b) duties, taxes and customs brokerage fees on the non‑originating materials that:

(i) have been paid in either or both of the territory of Malaysia and the territory of Australia; and

(ii) have not been waived or refunded; and

(iii) are not refundable or otherwise recoverable;

including any credit against duties or taxes that have been paid or that are payable;

(c) the costs of waste and spoilage resulting from the use of the non‑originating materials in the production of the goods, reduced by the value of renewable scrap or by‑products;

(d) the costs of processing incurred in either or both of the territory of Malaysia and the territory of Australia in the production of the non‑originating materials;

(e) the costs of originating materials used in the production of the non‑originating materials in either or both of the territory of Malaysia and the territory of Australia.

4.2 Value of accessories, spare parts, tools or instructional or other information materials

If paragraphs 153ZLE(7)(a), (b), (c) and (d) of the Act are satisfied in relation to goods:

(a) the value of the accessories, spare parts, tools or instructional or other information materials must be taken into account for the purposes of working out the regional value content of the goods under Part 3 of this regulation; and

(b) if the accessories, spare parts, tools or instructional or other information materials are non‑originating materials—for the purposes of sections 3.1 and 4.1 of this regulation, those accessories, spare parts, tools or instructional or other information materials are taken to be non‑originating materials used in the production of the goods; and

(c) if the accessories, spare parts, tools or instructional or other information materials are originating materials—for the purposes of sections 3.2 and 4.1 of this regulation, those accessories, spare parts, tools or instructional or other information materials are taken to be originating materials used in the production of the goods.

4.3 Value of packaging material and container

(1) If paragraphs 153ZLF(1)(a) and (b) of the Act are satisfied in relation to goods and the goods must have a regional value content of not less than a particular percentage worked out in a particular way:

(a) the value of the packaging material or container in which the goods are packaged must be taken into account for the purposes of working out the regional value content of the goods under Part 3 of this regulation; and

(b) if that packaging material or container is a non‑originating material—for the purposes of sections 3.1 and 4.1 of this regulation, that packaging material or container is taken to be a non‑originating material used in the production of the goods; and

(c) if that packaging material or container is an originating material—for the purposes of sections 3.2 and 4.1 of this regulation, that packaging material or container is taken to be an originating material used in the production of the goods.

(2) However, if the packaging material or container is not customary for the goods, the packaging material or container must be taken into account as a non‑originating material for the purposes of working out the regional value content of the goods.

15 Schedule 1

Repeal the Schedule.

Part 6—Korean originating goods

Customs (Korean Rules of Origin) Regulation 2014

16 Section 4

Repeal the following definitions:

(a) definition of chapter;

(b) definition of heading;

(c) definition of Korean originating goods;

(d) definition of subheading.

17 Section 4

Insert:

territory of Australia has the meaning given by section 153ZMB of the Act.

territory of Korea has the meaning given by section 153ZMB of the Act.

18 Parts 2 to 4

Repeal the Parts, substitute:

Part 2—Tariff change requirement

5 Change in tariff classification requirement for non‑originating materials

For the purposes of subsection 153ZME(3) of the Act, a non‑originating material used in the production of goods that does not satisfy a particular change in tariff classification is taken to satisfy the change in tariff classification if:

(a) it was produced entirely in the territory of Korea, or entirely in the territory of Korea and the territory of Australia, from other non‑originating materials; and

(b) each of those other non‑originating materials satisfies the change in tariff classification, including by one or more applications of this section.

Part 3—Regional value content requirement

6 Build‑down method

(1) For the purposes of subsection 153ZME(7) of the Act, the regional value content of goods under the build‑down method is worked out using the formula:

where:

customs value means the customs value of the goods worked out under Division 2 of Part VIII of the Act.

value of non‑originating materials means the value, worked out under Part 4, of the non‑originating materials used in the production of the goods.

(2) Regional value content must be expressed as a percentage.

7 Build‑up method

(1) For the purposes of subsection 153ZME(7) of the Act, the regional value content of goods under the build‑up method is worked out using the formula:

where:

customs value means the customs value of the goods worked out under Division 2 of Part VIII of the Act.

value of originating materials means the value, worked out under Part 4, of the originating materials used in the production of the goods.

(2) Regional value content must be expressed as a percentage.

Part 4—Determination of value

8 Value of goods that are originating materials or non‑originating materials

(1) For the purposes of subsection 153ZMB(3) of the Act, this section explains how to work out the value of originating materials or non‑originating materials used in the production of goods.

(2) The value of the materials is as follows:

(a) for materials imported into the territory of Korea by the producer of the goods—the value of the materials worked out in accordance with the Agreement on Implementation of Article VII of the General Agreement on Tariffs and Trade 1994;

(b) for materials acquired in the territory of Korea—the earliest ascertainable cost of acquisition of the materials;

(c) for materials that are produced by the producer of the goods—the sum of:

(i) all the costs incurred in the production of the materials, including general expenses; and

(ii) an amount that is the equivalent of the amount of profit that the producer would make for the materials in the normal course of trade.

(3) In working out the value of particular originating materials under subsection (2), the following may be included, to the extent that they have not been taken into account under that subsection:

(a) the costs of freight, insurance, packing and all other costs incurred to transport the materials within the territory of Korea, or between the territory of Australia and the territory of Korea, to the location of the producer of the goods;

(b) duties, taxes and customs brokerage fees on the materials that:

(i) have been paid in either or both of the territory of Korea and the territory of Australia; and

(ii) have not been waived or refunded; and

(iii) are not refundable or otherwise recoverable;

including any credit against duties or taxes that have been paid or that are payable.

(4) In working out the value of particular non‑originating materials under subsection (2), the following may be deducted if they were included under that subsection:

(a) the costs of originating materials used in the production of the non‑originating materials in the territory of Korea;

(b) the costs of freight, insurance, packing and all other costs incurred to transport the non‑originating materials within the territory of Korea, or between the territory of Australia and the territory of Korea, to the location of the producer of the goods;

(c) duties, taxes and customs brokerage fees on the non‑originating materials that:

(i) have been paid in either or both of the territory of Korea and the territory of Australia; and

(ii) have not been waived or refunded; and

(iii) are not refundable or otherwise recoverable;

including any credit against duties or taxes that have been paid or that are payable;

(d) the costs of processing incurred in either or both of the territory of Korea and the territory of Australia in the production of the non‑originating materials.

9 Value of accessories, spare parts or tools

If paragraphs 153ZME(8)(a), (b), (c) and (d) of the Act are satisfied in relation to goods:

(a) the value of the accessories, spare parts or tools must be taken into account for the purposes of working out the regional value content of the goods under Part 3 of this instrument; and

(b) if the accessories, spare parts or tools are non‑originating materials—for the purposes of sections 6 and 8 of this instrument, those accessories, spare parts or tools are taken to be non‑originating materials used in the production of the goods; and

(c) if the accessories, spare parts or tools are originating materials—for the purposes of sections 7 and 8 of this instrument, those accessories, spare parts or tools are taken to be originating materials used in the production of the goods.

10 Value of packaging material and container

If paragraphs 153ZMF(1)(a) and (b) of the Act are satisfied in relation to goods and the goods must have a regional value content of not less than a particular percentage worked out in a particular way:

(a) the value of the packaging material or container in which the goods are packaged must be taken into account for the purposes of working out the regional value content of the goods under Part 3 of this instrument; and

(b) if that packaging material or container is a non‑originating material—for the purposes of sections 6 and 8 of this instrument, that packaging material or container is taken to be a non‑originating material used in the production of the goods; and

(c) if that packaging material or container is an originating material—for the purposes of sections 7 and 8 of this instrument, that packaging material or container is taken to be an originating material used in the production of the goods.

19 Schedule 1

Repeal the Schedule.