Part 1—Preliminary

1 Name

This instrument is the ASIC Supervisory Cost Recovery Levy Regulations 2017.

3 Authority

This instrument is made under the ASIC Supervisory Cost Recovery Levy Act 2017.

4 Definitions

Note: A number of expressions used in this instrument are defined in the Act, including the following:

(a) ASIC;

(b) leviable entity.

(1) In this instrument:

Act means the ASIC Supervisory Cost Recovery Levy Act 2017.

amount of credit has the same meaning as in subsection 3(2) of the National Credit Code.

annual determination means the legislative instrument made for a financial year by ASIC under section 73.

Australian credit licence has the same meaning as in the National Consumer Credit Protection Act 2009.

Australian member:

(a) in relation to a notified foreign passport fund—has the same meaning as in the Corporations Act 2001; and

(b) in relation to a regulated former notified fund—means a person who either:

(i) holds an interest in the fund that was acquired in this jurisdiction (within the meaning of the Corporations Act 2001); or

(ii) is ordinarily resident in this jurisdiction (within the meaning of the Corporations Act 2001) and holds an interest in the fund.

basic banking product has the same meaning as in section 910A of the Corporations Act 2001.

credit has the same meaning as in the National Consumer Credit Protection Act 2009.

credit activity has the same meaning as in the National Consumer Credit Protection Act 2009.

credit contract has the same meaning as in the National Consumer Credit Protection Act 2009.

credit provider has the same meaning as in the National Consumer Credit Protection Act 2009.

deal has the same meaning as dealing in section 761A of the Corporations Act 2001.

entity metric: a leviable entity’s entity metric for a sub‑sector for a financial year is the amount worked out for the entity under a provision of Part 3 that specifies an amount to be the entity’s entity metric for the sub‑sector for the financial year.

Note: See also section 12.

financial year means a period of 12 months starting on 1 July.

graduated levy component for a sub‑sector for a financial year has the meaning given by section 10.

large futures exchange has the meaning given by subsection 52(3).

large securities exchange has the meaning given by subsection 51(3).

lot means a single futures contract with predefined terms and values.

medium amount credit contract has the same meaning as in the National Consumer Credit Protection Act 2009.

minimum levy component for a sub‑sector for a financial year means the minimum levy component specified in Part 3 for the sub‑sector.

National Credit Code has the same meaning as in the National Consumer Credit Protection Act 2009.

operator:

(a) in relation to a notified foreign passport fund—has the same meaning as in the Corporations Act 2001; and

(b) in relation to a regulated former notified fund:

(i) if the fund is a regulated CIS—has the same meaning as in the Passport Rules for this jurisdiction; and

(ii) if the fund is no longer a regulated CIS—the entity or entities in control of the fund.

overseas market has the meaning given by subsection 46(3).

over‑the‑counter, in relation to a financial product, means a financial product that cannot be traded on:

(a) a large futures exchange; or

(b) a large securities exchange; or

(c) a market licensed under subsection 795B(2) of the Corporations Act 2001 that operates as an exchange; or

(d) a small futures exchange; or

(e) a small securities exchange; or

(f) a small securities (self‑listing) exchange.

participant has the same meaning as in section 761A of the Corporations Act 2001.

registrable superannuation entity has the same meaning as in the Superannuation Industry (Supervision) Act 1993.

regulated CIS has the same meaning as in Chapter 8A of the Corporations Act 2001.

regulated former notified fund means a fund described in paragraph 5C(2)(b) or (c).

relevant financial products has the same meaning as in section 910A of the Corporations Act 2001.

small amount credit contract has the same meaning as in the National Consumer Credit Protection Act 2009.

small futures exchange has the meaning given by subsection 49(3).

small securities exchange has the meaning given by subsection 48(3).

small securities (self‑listing) exchange has the meaning given by subsection 47(3).

specialised market has the meaning given by subsection 52A(4).

sub‑sector means a group of one or more entities each of which meets the criteria specified in a provision of Part 3 for an entity to form part of the sub‑sector.

Note 1: Within each such provision, the name of the sub‑sector is identified in bold italics.

Note 2: For a list of sub‑sectors, see Schedule 1.

sub‑sector population, in relation to a sub‑sector, for a financial year, means the number of entities specified by ASIC in an annual determination to be the number of entities that form part of the sub‑sector at any time in the financial year.

sub‑sector regulatory costs, in relation to a sub‑sector, for a financial year, means the Australian dollar amount specified by ASIC in a determination made under subsection 10(2) of the Act to be the extent to which ASIC’s regulatory costs for the financial year are attributable to the sub‑sector.

supervisory college means a college of regulators established for a credit rating agency:

(a) that has significant cross border operations; and

(b) that has affiliates or branches in more than one country; and

(c) whose credit ratings are relied on by investors and other users of credit ratings in more than one country.

unregistered managed investment scheme is a managed investment scheme that is not:

(a) a registered scheme; or

(b) a notified foreign passport fund; or

(c) a regulated former notified fund.

(2) Other expressions used in this instrument that are defined in section 9 or 761A of the Corporations Act 2001 have the same meaning as they have in those sections.

Part 2—General provisions

Division 1—Regulatory costs

5 Amounts not included in regulatory costs

For the purposes of paragraph 10(4)(c) of the Act, the following amounts must not be included in the amount of ASIC’s regulatory costs for a financial year:

(a) the cost of operating the Superannuation Complaints Tribunal (as established under the Superannuation (Resolution of Complaints) Act 1993);

(b) the cost of operating the Companies Auditors Disciplinary Board (as established under the Australian Securities and Investments Commission Act 2001);

(c) the cost of operating a committee convened under section 40‑45 of Schedule 2 to the Corporations Act 2001;

(d) the cost of operating and maintaining a public register kept by ASIC under the Corporations Act 2001;

(e) the cost of regulating approved SMSF auditors (within the meaning of the Superannuation Industry (Supervision) Act 1993);

(f) the cost of preliminary investigations and reports by liquidators into the failure of a company with few or no assets;

(g) if the financial year commences before 1 July 2019, the costs associated with achieving the outcome described in Budget Paper No. 2, Budget Measures 2016‑17, Part 2, topic headed “Australian Securities and Investments Commission—improving outcomes in financial services”.

5A Amounts included in regulatory costs

For the purposes of paragraph 10(5)(e) of the Act, the amount of ASIC’s regulatory costs for a financial year may include an amount of ASIC’s operating costs for a financial year before the 2017‑18 financial year that:

(a) ASIC is eligible to recover in the 2017‑18 financial year, and later financial years, under item 29 of Schedule 1 to the ASIC Supervisory Cost Recovery Levy (Consequential Amendments) Act 2017; and

(b) ASIC has not previously recovered under that item; and

(c) do not relate to amounts covered by subsection 10(4) of the Act.

Division 1A—Exempt and regulated entities

5B Exempt entities

For the purposes of the definition of exempt entity in section 7 of the Act, the class of persons who, on 30 June in the 2017‑18 financial year or a later financial year, are entities registered under the Australian Charities and Not‑for‑profits Commission Act 2012 is prescribed for that financial year.

5C Regulated entities

(1) For the purposes of paragraph (h) of the definition of regulated entity in section 7 of the Act, the class of persons:

(a) who are persons regulated by ASIC in respect of whom ASIC may exercise a power conferred under section 11 or 12A of the Australian Securities and Investments Commission Act 2001; and

(b) none of whom would, apart from this section, be leviable entities;

is prescribed.

(2) For the purposes of paragraph (h) of the definition of regulated entity in section 7 of the Act, the following classes of persons are prescribed:

(a) the operators of notified foreign passport funds;

(b) the operators of regulated CIS that:

(i) have been removed as notified foreign passport funds under Division 2 of Part 8A.7 of the Corporations Act 2001; and

(ii) still have protected members for the purposes of regulation 8A.7.20 of the Corporations Regulations 2001;

(c) the operators of funds that:

(i) have ceased to be regulated CIS; and

(ii) have been removed as notified foreign passport funds under Division 2 of Part 8A.7 of the Corporations Act 2001; and

(iii) still have protected members for the purposes of regulation 8A.7.20 of the Corporations Regulations 2001.

Division 2—Amount of levy payable

Subdivision 2.1—General

6 Amount of levy

The amount of levy payable by a leviable entity for a financial year is the sum of each levy component the entity has for the financial year.

7 Levy component

When an entity has a levy component

(1) A leviable entity has a levy component for a financial year in respect of each sub‑sector of which the entity forms part at any time in the financial year.

Amount of a levy component

(2) The amount of a leviable entity’s levy component for a financial year in respect of a sub‑sector is:

(a) if a provision of Part 3 provides that the basic levy component applies to the sub‑sector for the financial year—the basic levy component for the entity for the sub‑sector for the financial year; or

(b) otherwise—the amount of the levy component worked out for the entity and the sub‑sector under Part 3.

Note: For the basic levy component, see section 9.

8 Levy component for leviable entities that are deregistered

However, the amount of levy payable by a leviable entity for a financial year is nil if:

(a) the entity is required to lodge a return relating to the financial year with ASIC under section 11 of the ASIC Supervisory Cost Recovery Levy (Collection) Act 2017; and

(b) before the end of the day on which the return is required to be lodged:

(i) the entity is deregistered under Part 5A.1 of the Corporations Act 2001; or

(ii) ASIC publishes a notice regarding the proposed deregistration of the entity under section 601AA or 601AB of that Act; and

(c) the entity’s registration has not been reinstated before the end of that day.

Subdivision 2.2—Levy components

9 Basic levy component

(1) The basic levy component for a leviable entity for a sub‑sector for a financial year is the amount worked out using the formula:

where:

basic rate entity metric means:

(a) unless paragraph (b) applies—the entity’s entity metric for the sub‑sector for the financial year; or

(b) if no provision in Part 3 specifies an amount to be the entity metric for the sub‑sector for the financial year—1.

sub‑sector metric means the number specified by ASIC in an annual determination to be the sum of the amounts of basic rate entity metric for all leviable entities that form part of the sub‑sector for the financial year.

sub‑sector regulatory costs means the sub‑sector regulatory costs in relation to the sub‑sector for the financial year.

(2) However, if a component of the formula is nil or a negative amount, the amount of the basic levy component is nil.

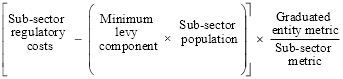

10 Graduated levy component

(1) The graduated levy component for a leviable entity for a sub‑sector for a financial year is the amount worked out using the formula:

where:

graduated entity metric means:

(a) unless paragraph (b) applies—the entity’s entity metric for the sub‑sector for the financial year; or

(b) if a provision of Part 3 specifies a minimum levy threshold for the sub‑sector for the financial year—the difference between the entity’s entity metric for the sub‑sector for the financial year and the minimum levy threshold.

minimum levy component means the minimum levy component for the sub‑sector for the financial year.

sub‑sector metric means the number specified by ASIC in an annual determination to be the sum of the amounts of graduated entity metric for all leviable entities that form part of the sub‑sector for the financial year.

sub‑sector population means the sub‑sector population in relation to the sub‑sector for the financial year.

sub‑sector regulatory costs means the sub‑sector regulatory costs in relation to the sub‑sector for the financial year.

(2) However, if a component of the formula is nil or a negative amount, the amount of the graduated levy component is nil.

11 Pro‑rata of entity metric

(1) This section applies to a leviable entity for a financial year if:

(a) a provision of Part 3 (the pro‑rata provision) that applies to the entity provides that there is a pro‑rata of the entity metric for a sub‑sector for a financial year; and

(b) the number of counted days for the entity for the financial year under the pro‑rata provision is less than the number of days in the financial year.

(2) The entity metric for the leviable entity is to be reduced by multiplying it by the following fraction:

where:

counted days means the number of days counted for the entity under the pro‑rata provision.

12 Rules about amounts

(1) An amount worked out under this Division must be rounded to the nearest whole dollar (rounding 50 cents upwards).

(2) If an entity metric worked out under this instrument is not a whole number, the entity metric must be rounded to the nearest whole number (rounding 0.5 upwards).

(3) If an entity metric is an amount worked out in Australian dollars, the amount of the entity metric is instead the number of dollars in the amount.

(4) If a minimum levy threshold is an amount in Australian dollars, the amount of the threshold is instead the number of dollars in the amount.

Part 3—Sectors, sub‑sectors and levy components

Division 1—Corporate sector

Subdivision 1.1—General

13 Corporate sector

(1) Each section in Subdivisions 1.2 and 1.3 specifies criteria for identifying one or more leviable entities that form part of the sub‑sector mentioned in the section.

(2) The sub‑sectors for which criteria are specified in this Division are in the corporate sector.

(3) A leviable entity may form part of 2 or more sub‑sectors in the corporate sector.

14 Basic levy component applies to sub‑sectors in Subdivision 1.2

The basic levy component applies to each sub‑sector specified in a section of Subdivision 1.2.

Note: For the basic levy component, see section 9.

Subdivision 1.2—Sub‑sectors to which basic levy component applies

15 Auditors of disclosing entities

(1) A leviable entity forms part of the auditors of disclosing entities sub‑sector in a financial year if, at any time in the financial year, the entity is, or has consented to be, an audit entity for a disclosing entity with quoted securities.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is the total of the fees paid or payable to the entity in the financial year for the auditing and review of financial reports that relate to:

(a) a disclosing entity with quoted securities; or

(b) an entity controlled by a disclosing entity with quoted securities.

(3) For the purposes of paragraph (2)(b), the question of whether a disclosing entity controls another entity is to be decided in accordance with the accounting standard AASB 10 Consolidated Financial Statements.

(4) In this section:

prescribed financial market has the same meaning as in the Corporations Act 2001.

quoted, in relation to securities, means quoted on a prescribed financial market.

securities has the meaning given by subsection 92(3) of the Corporations Act 2001 for the purposes of Chapters 6 to 6CA of that Act (disregarding Chapter 6C of that Act).

16 Large proprietary companies

A leviable entity forms part of the large proprietary companies sub‑sector in a financial year if, at any time in the financial year, the entity is a large proprietary company.

17 Public companies (unlisted)

A leviable entity forms part of the public companies (unlisted) sub‑sector in a financial year if, at any time in the financial year, the entity is a public company that is not listed.

18 Registered company auditors

A leviable entity forms part of the registered company auditors sub‑sector in a financial year if, at any time in the financial year, the entity is a registered company auditor.

Subdivision 1.3—Sub‑sectors to which graduated levy component applies

19 Listed corporations

(1) A leviable entity forms part of the listed corporations sub‑sector in a financial year if, at any time in the financial year, the entity is a listed corporation.

Levy component

(2) The amount of a leviable entity’s levy component in respect of the sub‑sector for the financial year is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) the graduated levy component for the entity for the sub‑sector.

Note: For the graduated levy component, see section 10.

Entity metric

(3) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) if the entity’s market capitalisation for the financial year (as worked out under subsection (5)) is less than the maximum levy threshold—the entity’s market capitalisation for the financial year; or

(b) if the entity’s market capitalisation for the financial year (as worked out under subsection (5)) equals or exceeds the maximum levy threshold—the maximum levy threshold.

(4) However:

(a) there is a pro‑rata of the entity metric; and

(b) for the purposes of section 11, the number of counted days is the number of days in the financial year on which the leviable entity was a listed corporation.

(5) A leviable entity’s market capitalisation for a financial year is worked out by:

(a) if the entity is listed on a financial market at the end of the financial year—multiplying:

(i) the price for the entity’s main class of securities at the time the financial market closes on the last trading day on or before 30 June of the financial year; by

(ii) the number of securities in that class at that relevant time; or

(b) if the entity is not listed on a financial market at the end of the financial year—multiplying:

(i) the last price for the entity’s main class of securities on the day before the entity stops being listed on the financial market; by

(ii) the number of securities in that class at that relevant time.

(5A) However, if the leviable entity is an exempt foreign entity under the listing rules of the Australian Stock Exchange Limited, disregard the number of securities of the entity that were not held in Australia, at the relevant time mentioned in paragraph (5)(a) or (5)(b) (whichever is applicable), for the purposes of working out:

(a) the main class of securities mentioned in subparagraph (5)(a)(i) or (5)(b)(i); and

(b) the number of securities mentioned in subparagraph (5)(a)(ii) or (5)(b)(ii).

(6) The maximum levy threshold for the sub‑sector is $20,000,000,000.

(7) The minimum levy component for the sub‑sector is $4,000.

(8) The minimum levy threshold for the sub‑sector is $5,000,000.

(9) In this section:

securities has the meaning given by subsection 92(3) of the Corporations Act 2001 for the purposes of Chapters 6 to 6CA of that Act (disregarding Chapter 6C of that Act).

20 Registered liquidators

(1) A leviable entity forms part of the registered liquidators sub‑sector in a financial year if, at any time in the financial year, the entity is a registered liquidator.

Levy component

(2) The amount of a leviable entity’s levy component in respect of the sub‑sector for the financial year is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) the graduated levy component for the entity for the sub‑sector.

Note: For the graduated levy component, see section 10.

Entity metric

(3) The leviable entity’s entity metric for the sub‑sector for the financial year is the sum of:

(a) the number of the following appointments under Chapter 5 of the Corporations Act 2001 accepted by the entity in the financial year:

(i) an appointment as a controller;

(ii) an appointment as a liquidator;

(iii) an appointment as a managing controller;

(iv) an appointment as a receiver;

(v) an appointment as a receiver and manager;

(vi) an appointment as a scheme manager;

(vii) an appointment as a voluntary administrator;

(viii) an appointment as an administrator of a deed of company arrangement; and

(b) the number of appointments of the kind mentioned in subparagraph (a)(i) to (viii) that were accepted in an earlier financial year and that the entity is still acting in at the start of the financial year for which the levy component is to be calculated; and

(c) the number of the following events that are published on the publication website maintained by ASIC under regulation 5.6.75 of the Corporations Regulations 2001 for the entity in the financial year:

(i) notice of meetings;

(ii) notice of disclaimer of property;

(iii) notice to submit particulars of debt or claims;

(iv) notice to creditors to submit formal proof;

(v) notice of intention to declare dividend; and

(d) the number of the following documents lodged with ASIC by the entity in the financial year:

(i) a notice of the outcome of a proposal to pass a resolution without a meeting (however, if more than one proposal to pass a resolution without a meeting in relation to the same administration is decided on the same day, count the proposals as a single lodgement);

(ii) an executed deed of company arrangement (however, if the deed involves more than one company under external administration, count the deed as a single lodgement).

(4) The minimum levy component for the sub‑sector is $2,500.

Division 2—Deposit‑taking and credit sector

Subdivision 2.1—General

21 Deposit‑taking and credit sector

(1) Each section in Subdivisions 2.2 and 2.3 specifies criteria for identifying one or more leviable entities that form part of the sub‑sector mentioned in the section.

(2) The sub‑sectors for which criteria are specified in this Division are in the deposit‑taking and credit sector.

(3) A leviable entity may form part of 2 or more sub‑sectors in the deposit‑taking and credit sector.

22 Basic levy component applies to sub‑sectors in Subdivision 2.2

The basic levy component applies to each sub‑sector specified in a section of Subdivision 2.2.

Note: For the basic levy component, see section 9.

Subdivision 2.2—Sub‑sectors to which basic levy component applies

23 Margin lenders

(1) A leviable entity forms part of the margin lenders sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australian financial services licence that authorises the holder to deal in a financial product by issuing margin lending facilities.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is the number of days in the financial year on which the entity holds a licence of the kind mentioned in subsection (1).

24 Small and medium amount credit providers

(1) A leviable entity forms part of the small and medium amount credit providers sub‑sector in a financial year if, at any time in the financial year, the entity:

(a) holds an Australian credit licence that authorises the holder to engage in credit activities as a credit provider; and

(b) provides credit under a small amount credit contract or a medium amount credit contract.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is the gross amount of credit provided by the entity in the financial year under small amount credit contracts or medium amount credit contracts.

Subdivision 2.3—Sub‑sectors to which graduated levy component applies

25 Credit intermediaries

(1) A leviable entity forms part of the credit intermediaries sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australian credit licence that authorises the entity to engage in credit activities other than as a credit provider.

Levy component

(2) The amount of a leviable entity’s levy component in respect of the sub‑sector for the financial year is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) the graduated levy component for the entity for the sub‑sector.

Note: For the graduated levy component, see section 10.

Entity metric

(3) The leviable entity’s entity metric for the sub‑sector for the financial year is the number of credit representatives (within the meaning of the National Consumer Credit Protection Act 2009) the entity has at the end of the financial year.

(4) However:

(a) there is a pro‑rata of the entity metric; and

(b) for the purposes of section 11, the number of counted days is the number of days in the financial year on which the leviable entity holds a licence of the kind mentioned in subsection (1).

(5) The minimum levy component for the sub‑sector is $1,000.

26 Credit providers

(1) A leviable entity forms part of the credit providers sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australian credit licence that authorises the holder to engage in credit activities as a credit provider.

Levy component

(2) The amount of a leviable entity’s levy component in respect of the sub‑sector for the financial year is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) if the entity’s entity metric for the sub‑sector for the financial year exceeds the minimum levy threshold—the graduated levy component for the entity for the sub‑sector.

Note: For the graduated levy component, see section 10.

Entity metric

(3) The leviable entity’s entity metric for the sub‑sector for the financial year is the gross amount of credit provided by the entity in the financial year under credit contracts (other than small amount credit contracts or medium amount credit contracts).

(4) The minimum levy component for the sub‑sector is $2,000.

(5) The minimum levy threshold for the sub‑sector is $100,000,000.

27 Deposit product providers

(1) A leviable entity forms part of the deposit product providers sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australian financial services licence that authorises the holder to deal in a financial product by issuing deposit products.

Levy component

(2) The amount of a leviable entity’s levy component in respect of the sub‑sector for the financial year is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) if the entity’s entity metric for the sub‑sector for the financial year exceeds the minimum levy threshold—the graduated levy component for the entity for the sub‑sector.

Note: For the graduated levy component, see section 10.

Entity metric

(3) The leviable entity’s entity metric for the sub‑sector for the financial year is the total value of deposits held at the end of the financial year in deposit products issued by the entity (whether the deposit product was issued in the financial year or an earlier financial year).

(4) However:

(a) there is a pro‑rata of the entity metric; and

(b) for the purposes of section 11, the number of counted days is the number of days in the financial year on which the leviable entity holds a licence of the kind mentioned in subsection (1).

(5) The minimum levy component for the sub‑sector is $2,000.

(6) The minimum levy threshold for the sub‑sector is $10,000,000.

28 Payment product providers

(1) A leviable entity forms part of the payment product providers sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australian financial services licence that authorises the holder to deal in a financial product through which, or through the acquisition of which, non‑cash payments can be made.

Note: For non‑cash payments, see section 763D of the Corporations Act 2001.

Levy component—financial year starting on 1 July 2017

(2) The basic levy component applies in respect of the sub‑sector for the financial year starting on 1 July 2017.

Note: For the basic levy component, see section 9.

Entity metric—financial year starting on 1 July 2017

(3) The leviable entity’s entity metric for the sub‑sector for the financial year starting on 1 July 2017 is the number of days in the financial year on which the entity holds a licence of the kind mentioned in subsection (1).

Levy component—financial year starting on or after 1 July 2018

(4) The amount of a leviable entity’s levy component in respect of the sub‑sector for a financial year starting on or after 1 July 2018 is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) the graduated levy component for the entity for the sub‑sector.

Note: For the graduated levy component, see section 10.

Entity metric—financial year starting on or after 1 July 2018

(5) The leviable entity’s entity metric for the sub‑sector for a financial year starting on or after 1 July 2018 is the gross revenue received in the financial year by the entity in connection with non‑cash payment products issued by the entity less expenses incurred in the financial year from dealing in non‑cash payment facilities.

(6) The minimum levy component for the sub‑sector is $2,000.

Division 3—Investment management, superannuation and related services sector

Subdivision 3.1—General

29 Investment management, superannuation and related services sector

(1) Each section in Subdivisions 3.2 and 3.3 specifies criteria for identifying one or more leviable entities that form part of the sub‑sector mentioned in the section.

(2) The sub‑sectors for which criteria are specified in this Division are in the investment management, superannuation and related services sector.

(3) A leviable entity may form part of 2 or more sub‑sectors in the investment management, superannuation and related services sector.

30 Basic levy component applies to sub‑sectors in Subdivision 3.2

The basic levy component applies to each sub‑sector specified in a section of Subdivision 3.2.

Note: For the basic levy component, see section 9.

Subdivision 3.2—Sub‑sectors to which basic levy component applies

31 Custodians

A leviable entity forms part of the custodians sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australian financial services licence that authorises the holder to provide a custodial or depository service.

32 Managed discretionary account providers

(1) A leviable entity forms part of the managed discretionary account providers sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australian financial services licence that authorises the holder to deal in a financial product by issuing financial products in respect of:

(a) interests in managed investment schemes limited to MDA services (within the meaning of the ASIC Corporations (Managed Discretionary Account Services) Instrument 2016/968); or

(b) miscellaneous financial investment products limited to MDA services;

whether or not the licence also authorises the holder to deal in other financial products.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is the number of days in the financial year on which the entity holds a licence of the kind mentioned in subsection (1).

33 Traditional trustee company service providers

(1) A leviable entity forms part of the traditional trustee company service providers sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australian financial services licence that authorises the holder to provide traditional trustee company services.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is the number of days in the financial year on which the entity holds a licence of the kind mentioned in subsection (1).

Subdivision 3.3—Sub‑sectors to which graduated levy component applies

34 Operators of investor directed portfolio services

(1) A leviable entity forms part of the operators of investor directed portfolio services sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australian financial services licence that authorises the holder to operate an IDPS (within the meaning of section 21 of ASIC Class Order [CO 13/763]).

Levy component

(2) The amount of a leviable entity’s levy component in respect of the sub‑sector for a financial year is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) the graduated levy component for the entity for the sub‑sector.

Note: For the graduated levy component, see section 10.

Entity metric

(3) The leviable entity’s entity metric for the sub‑sector for the financial year is the sum of the following amounts:

(a) the amount of gross revenue received from IDPS activities undertaken under the entity’s licence in the financial year;

(b) any amount (to the extent that it is not covered under paragraph (a)) paid or payable in the financial year from the IDPS for the performance of obligations imposed on an entity as an operator of the IDPS (even if those obligations are performed by another entity).

(4) Revenue is to be calculated for the purposes of this section in accordance with accounting standards in force at the relevant time (even if the standard does not otherwise apply to the financial year or some or all of the entities concerned).

(5) The minimum levy component for the sub‑sector is $10,000.

35 Responsible entities

(1) A leviable entity forms part of the responsible entities sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australian financial services licence that authorises the holder to operate a registered scheme.

Levy component

(2) The amount of a leviable entity’s levy component in respect of the sub‑sector for the financial year is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) if the entity’s entity metric for the sub‑sector for the financial year exceeds the minimum levy threshold—the graduated levy component for the entity for the sub‑sector.

Note: For the graduated levy component, see section 10.

Entity metric

(3) The leviable entity’s entity metric for the sub‑sector for the financial year is the total value of assets in all registered schemes operated by the entity at the end of the financial year, disregarding:

(a) any assets that are an interest in another registered scheme operated by the entity; and

(b) if the entity also forms part of the wholesale trustees sub‑sector in the financial year—any assets that are an interest in an unregistered managed investment scheme issued by the entity.

(4) However:

(a) there is a pro‑rata of the entity metric; and

(b) for the purposes of section 11, the number of counted days is the number of days in the financial year on which the leviable entity holds a licence of the kind mentioned in subsection (1).

(5) The minimum levy component for the sub‑sector is $7,000.

(6) The minimum levy threshold for the sub‑sector is $10,000,000.

35A Operators of notified foreign passport funds and regulated former notified funds

(1) A leviable entity forms part of the operators of notified foreign passport funds and regulated former notified funds sub‑sector in a financial year if, at any time in the financial year, the entity is the operator of:

(a) a notified foreign passport fund; or

(b) regulated former notified fund.

Levy component

(2) The amount of a leviable entity’s levy component in respect of the sub‑sector for the financial year is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) the graduated levy component for the entity for the sub‑sector.

Note: For the graduated levy component, see section 10.

Entity metric

(3) If the leviable entity is the operator of a notified foreign fund, the leviable entity’s entity metric for the sub‑sector for the financial year is the total value of Australian assets in all notified foreign passport funds operated by the entity at the end of the financial year, disregarding:

(a) any assets that are an interest in another notified foreign passport fund operated by the entity; and

(b) any assets that are an interest in a regulated former notified fund operated by the entity; and

(c) if the entity also forms part of the wholesale trustees sub‑sector—any assets that are an interest in an unregistered managed investment scheme issued by the entity.

(4) If the leviable entity is the operator of a regulated former notified fund, the leviable entity’s entity metric for the sub‑sector for the financial year is the total value of Australian assets in all regulated former notified funds at the end of the financial year, disregarding:

(a) any assets that are an interest in another regulated former notified fund operated by the entity; and

(b) any assets that are an interest in a notified foreign passport fund operated by the entity; and

(c) if the entity also forms part of the wholesale trustees sub‑sector—any assets that are an interest in an unregistered managed investment scheme issued by the entity.

(5) For the purposes of this section:

redemption price of an interest in a notified foreign passport fund or regulated former notified fund at a particular time is the amount that would be the redemption price for the interest at that time under subsection 50(1) of the Passport Rules for this jurisdiction if that subsection applied to the operator in relation to the fund, assuming that:

(a) the member who holds the interest makes a request, immediately before that time, for a redemption of the interest; and

(b) the amount is calculated using a valuation of the assets of the fund at that time; and

(c) redemption fees and transaction costs associated with redemption are ignored.

total value of Australian assets in a notified foreign passport fund or regulated former notified fund at a particular time is an amount equal to the sum of what would be the redemption prices of all interests in the fund held by Australian members of the fund at that time, if those interests were redeemed at that time.

(6) However:

(a) there is a pro‑rata of the entity metric for the sub‑sector for the financial year; and

(b) for the purposes of section 11, the number of counted days is the number of days in the financial year on which the leviable entity is:

(i) if the leviable entity is an operator of a notified foreign passport fund—the operator of the fund; or

(ii) if the leviable entity is an operator of a regulated former notified fund—the operator of the fund as a notified foreign passport fund or a regulated former notified fund.

(7) The minimum levy component for the sub‑sector is $1,000.

36 Superannuation trustees

(1) A leviable entity forms part of the superannuation trustees sub‑sector in a financial year if, at any time in the financial year, the entity is an RSE licensee (within the meaning of the Superannuation Industry (Supervision) Act 1993).

Levy component

(2) The amount of a leviable entity’s levy component in respect of the sub‑sector for the financial year is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) if the entity’s entity metric for the sub‑sector for the financial year exceeds the minimum levy threshold—the graduated levy component for the entity for the sub‑sector.

Note: For the graduated levy component, see section 10.

Entity metric

(3) The leviable entity’s entity metric for the sub‑sector for the financial year is the total value of assets in all registrable superannuation entities operated by the entity at the end of the financial year, disregarding:

(a) any assets that are an interest in another registrable superannuation entity operated by the entity; and

(b) any assets that are employer sponsored receivables.

(4) However:

(a) there is a pro‑rata of the entity metric; and

(b) for the purposes of section 11, the number of counted days is the number of days in the financial year on which the leviable entity was an RSE licensee.

(5) The minimum levy component for the sub‑sector is $18,000.

(6) The minimum levy threshold for the sub‑sector is $250,000,000.

37 Wholesale trustees

(1) A leviable entity forms part of the wholesale trustees sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australia financial services licence that authorises the holder to deal in a financial product by issuing interests in, or arranging for the issue of interests in, a managed investment scheme to wholesale clients.

Levy component—financial year starting on 1 July 2017

(2) The basic levy component applies in respect of the sub‑sector for the financial year starting on 1 July 2017.

Note: For the basic levy component, see section 9.

Entity metric—financial year starting on 1 July 2017

(3) The leviable entity’s entity metric for the sub‑sector for the financial year starting on 1 July 2017 is the number of days in the financial year on which the entity holds a licence of a kind mentioned in subsection (1).

Levy component—financial year starting on or after 1 July 2018

(4) The amount of a leviable entity’s levy component in respect of the sub‑sector for a financial year starting on or after 1 July 2018 is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) the graduated levy component for the entity for the sub‑sector.

Note: For the graduated levy component, see section 10.

Entity metric—financial year starting on or after 1 July 2018

(5) The leviable entity’s entity metric for the sub‑sector for a financial year starting on or after 1 July 2018 is the total value of assets at the end of the financial year in all unregistered managed investment schemes issued by the entity, disregarding:

(a) any assets that are an interest in another unregistered managed investment scheme issued by the entity; and

(b) if the entity also forms part of the responsible entities sub‑sector in the financial year—any assets that are an interest in a registered scheme operated by the entity; and

(c) if the entity also forms part of the operators of notified foreign passport funds and regulated former passport funds sub‑sector in the financial year—any assets that are an interest in a notified foreign passport fund or a regulated former notified fund issued by the entity.

(6) However:

(a) there is a pro‑rata of the entity metric for the sub‑sector for a financial year starting on or after 1 July 2018; and

(b) for the purposes of section 11, the number of counted days is the number of days in the financial year on which the leviable entity holds a licence of the kind mentioned in subsection (1).

(7) The minimum levy component for the sub‑sector is $1,000.

Division 4—Financial advice sector

Subdivision 4.1—General

38 Financial advice sector

(1) Each section in Subdivisions 4.2 and 4.3 specifies criteria for identifying one or more leviable entities that form part of the sub‑sector mentioned in the section.

(2) The sub‑sectors for which criteria are specified in this Division are in the financial advice sector.

(3) A leviable entity may form part of 2 or more sub‑sectors in the financial advice sector.

39 Basic levy component applies to sub‑sectors in Subdivision 4.2

The basic levy component applies to each sub‑sector specified in a section of Subdivision 4.2.

Note: For the basic levy component, see section 9.

Subdivision 4.2—Sub‑sectors to which basic levy component applies

40 Licensees that provide only general advice to retail or wholesale clients

A leviable entity forms part of the licensees that provide only general advice to retail or wholesale clients sub‑sector in a financial year if:

(a) the entity holds, at any time in the financial year, an Australian financial services licence; and

(b) the licence authorises the holder to provide financial product advice that is only general advice.

41 Licensees that provide personal advice to only wholesale clients

A leviable entity forms part of the licensees that provide personal advice to only wholesale clients sub‑sector in a financial year if the entity holds, at any time in the financial year, an Australian financial services licence that authorises the holder to provide financial product advice to only wholesale clients.

42 Licensees that provide personal advice to retail clients on only products that are not relevant financial products

(1) A leviable entity forms part of the licensees that provide personal advice to retail clients on only products that are not relevant financial products sub‑sector in a financial year if:

(a) the entity holds, at any time in the financial year, an Australian financial services licence; and

(b) the licence authorises the holder to provide financial product advice (including a class of product advice) to retail clients, on only one or more of the following products:

(i) basic banking products;

(ii) general insurance products;

(iii) consumer credit insurance (within the meaning of section 910A of the Corporations Act 2001).

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is the number of days in the financial year on which the entity holds a licence of the kind mentioned in subsection (1).

Subdivision 4.3—Sub‑sectors to which graduated levy component applies

43 Licensees that provide personal advice on relevant financial products to retail clients

(1) A leviable entity forms part of the licensees that provide personal advice on relevant financial products to retail clients sub‑sector in a financial year if:

(a) the entity holds, at any time in the financial year, an Australian financial services licence; and

(b) the licence authorises the holder to provide financial product advice (including a class of product advice) on relevant financial products to retail clients.

Levy component

(2) The amount of a leviable entity’s levy component in respect of the sub‑sector for a financial year is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) the graduated levy component for the entity for the sub‑sector.

Note: For the graduated levy component, see section 10.

Entity metric

(3) The leviable entity’s entity metric for the sub‑sector for the financial year is the number of relevant providers (within the meaning of section 910A of the Corporations Act 2001) that:

(a) are registered on the Register of Relevant Providers (within the meaning of section 910A of that Act) at the end of the financial year; and

(b) are authorised to provide personal advice to retail clients on behalf of the entity.

(4) For the purposes of working out the number of relevant providers under subsection (3) for an entity that also forms part of the large futures exchange participants sub‑sector (see section 64), the large securities exchange participants sub‑sector (see section 65) or the securities dealer sub‑sector (see section 67) at any time in the financial year, disregard relevant providers that only provide the following kinds of advice:

(a) advice on financial products that are admitted to quotation;

(b) advice on financial products that are traded on a prescribed foreign financial market (within the meaning of subregulation 7.7A.12D(2) of the Corporations Regulations 2001);

(c) advice on basic banking products.

(5) However:

(a) there is a pro‑rata of the entity metric; and

(b) for the purposes of section 11, the number of counted days is the number of days in the financial year on which the leviable entity holds a licence of the kind mentioned in subsection (1).

(6) The minimum levy component for the sub‑sector is $1,500.

Division 5—Market infrastructure and intermediaries sector

Subdivision 5.1—General

44 Market infrastructure and intermediaries sector

(1) Each section in Subdivisions 5.2 and 5.3 specifies criteria for identifying one or more leviable entities that form part of the sub‑sector mentioned in the section.

(2) The sub‑sectors for which criteria are specified in this Division are in the market infrastructure and intermediaries sector.

(3) A leviable entity may form part of 2 or more sub‑sectors in the market infrastructure and intermediaries sector unless otherwise specified in this Division.

45 Basic levy component applies to sub‑sectors in Subdivision 5.2

The basic levy component applies to each sub‑sector specified in a section of Subdivision 5.2.

Note: For the basic levy component, see section 9.

Subdivision 5.2—Sub‑sectors to which basic levy component applies

46 Overseas market operators

(1) A leviable entity forms part of the overseas market operators sub‑sector in a financial year if, at any time in the financial year, the entity operates an overseas market.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) unless paragraph (b) applies—the number of days in the financial year on which the entity operated the market; or

(b) if the entity operated 2 or more overseas markets in the financial year—the sum of the days worked out under paragraph (a) for each of those markets.

(3) A licensed market is an overseas market if the market is licensed under subsection 795B(2) of the Corporations Act 2001.

47 Small securities exchange operators with self‑listing function only

(1) A leviable entity forms part of the small securities exchange operators with self‑listing function only sub‑sector in a financial year if, at any time in the financial year, the entity is the operator of a small securities (self‑listing) exchange.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) unless paragraph (b) applies—the number of days in the financial year on which the entity operated the exchange; or

(b) if the entity operated 2 or more small securities (self‑listing) exchanges in the financial year—the sum of the days worked out under paragraph (a) for each of those exchanges.

(3) A licensed market is a small securities (self‑listing) exchange, in relation to a financial year, if:

(a) the market is not an overseas market; and

(b) only ordinary shares of the market operator can be traded on the market; and

(c) less than 10 million transactions in ordinary shares of the market operator are entered into on the market in the financial year.

48 Small securities exchange operators

(1) A leviable entity forms part of the small securities exchange operators sub‑sector in a financial year if, at any time in the financial year, the entity is the operator of a small securities exchange.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) unless paragraph (b) applies—the number of days in the financial year on which the entity operated the exchange; or

(b) if the entity operated 2 or more small securities exchanges in the financial year—the sum of the days worked out under paragraph (a) for each of those exchanges.

(3) A licensed market is a small securities exchange, in relation to a financial year, if:

(a) less than 10 million transactions in securities are entered into on the market in the financial year; and

(aa) the market is a prescribed financial market; and

(b) the market is not:

(i) an overseas market; or

(ii) a small securities (self‑listing) exchange.

(4) For the purposes of paragraph (3)(a), securities has the meaning given by section 761A of the Corporations Act 2001 for the purposes of Chapter 7 of that Act (disregarding Part 7.11 of that Chapter).

49 Small futures exchange operators

(1) A leviable entity forms part of the small futures exchange operators sub‑sector in a financial year if, at any time in the financial year, the entity is the operator of a small futures exchange.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) unless paragraph (b) applies—the number of days in the financial year on which the entity operated the exchange; or

(b) if the entity operated 2 or more small futures exchanges in the financial year—the sum of the days worked out under paragraph (a) for each of those exchanges.

(3) A licensed market is a small futures exchange, in relation to a financial year, if:

(a) less than 10 million transactions in futures contracts are entered into on the market in the financial year; and

(b) the market is not:

(i) an overseas market; or

(ii) a small securities (self‑listing) exchange; or

(iii) a small securities exchange.

51 Large securities exchange operators

(1) A leviable entity forms part of the large securities exchange operators sub‑sector in a financial year if, at any time in the financial year, the entity is the operator of a large securities exchange.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) unless paragraph (b) applies—the total value of all transactions that:

(i) are entered into on, or reported to, the large securities exchange operated by the entity in the financial year; and

(ii) are within the operating rules of the exchange; and

(iii) are not invalid or cancelled; or

(b) if the entity operated 2 or more large securities exchanges in the financial year—the sum of the amounts worked out under paragraph (a) for each of those exchanges.

(3) A licensed market is a large securities exchange, in relation to a financial year, if:

(a) 10 million or more transactions in securities are entered into on the market in the financial year; and

(b) the market is not an overseas market.

(4) For the purposes of paragraph (3)(a), securities has the meaning given by section 761A of the Corporations Act 2001 for the purposes of Chapter 7 of that Act (disregarding Part 7.11 of that Chapter).

52 Large futures exchange operators

(1) A leviable entity forms part of the large futures exchange operators sub‑sector in a financial year if, at any time in the financial year, the entity is the operator of a large futures exchange.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) unless paragraph (b) applies—the number of days in the financial year on which the entity operated the exchange; or

(b) if the entity operated 2 or more large futures exchanges in the financial year—the sum of the days worked out under paragraph (a) for each of those exchanges.

(3) A licensed market is a large futures exchange, in relation to a financial year, if:

(a) 10 million or more futures transactions are entered into on the market in the financial year; and

(b) the market is not:

(i) an overseas market; or

(ii) a large securities exchange.

52A New specialised market operators

(1) A leviable entity forms part of the new specialised market operators sub‑sector in a financial year if:

(a) the entity was first granted an Australian market licence to operate a specialised market in that financial year or the previous 2 financial years; and

(b) the entity had not held an Australian market licence at any time before the entity was first was granted the licence mentioned in paragraph (a); and

(c) the specialised market had not been operated by any entity in Australia or outside Australia before the entity was first granted an Australian market licence to operate the specialised market; and

(d) at any time in the financial year, the entity is the operator of the specialised market.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is the number of days in the financial year on which the entity operated the specialised market.

(3) For the purposes of subsection (2), if the entity was first granted an Australian market licence to operate a specialised market in the financial year before the previous financial year, disregard the days between:

(a) the day that is 24 months after the day on which the entity was first granted an Australian market licence to operate the specialised market; and

(b) 30 June of the financial year mentioned in paragraph (1)(d).

(4) A licensed market is a specialised market, in relation to a financial year, if:

(a) the market is licensed under subsection 795B(1) of the Corporations Act 2001 in the financial year; and

(b) the market is not:

(i) an overseas market; or

(ii) a small securities (self‑listing) exchange; or

(iii) a small securities exchange; or

(iv) a small futures exchange; or

(v) a large securities exchange; or

(vi) a large futures exchange.

52B Established specialised market operators

(1) A leviable entity forms part of the established specialised market operators sub‑sector in a financial year if:

(a) at any time in the financial year the entity is the operator of a specialised market; and

(b) one or more of the following apply:

(i) the entity was first granted an Australian market licence to operate the specialised market in a financial year before the previous financial year;

(ii) the specialised market had been operated by any entity in Australia or outside Australia before the entity was first granted an Australian market licence to operate the specialised market;

(iii) the entity held an Australian market licence before the entity was first was granted an Australian market licence to operate the specialised market.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) unless paragraph (b) applies—the number of days in the financial year on which the entity operated the specialised market; or

(b) if the entity operated 2 or more such specialised markets in the financial year—the sum of the days worked out under paragraph (a) for each of those markets.

(3) For the purposes of paragraph (2)(a), if the entity was first granted an Australian market licence to operate a specialised market in the financial year before the previous financial year and subparagraphs (1)(b)(ii) and (iii) do not apply to the entity, disregard the days between:

(a) 1 July of the financial year mentioned in paragraph (1)(a); and

(b) the day that is 24 months after the day on which the entity was first granted an Australian market licence to operate the specialised market.

53 Exempt market operators

(1) A leviable entity forms part of the exempt market operators sub‑sector in a financial year if, at any time in the financial year, the entity is the operator of a financial market that is exempt from the operation of the whole of Part 7.2 of the Corporations Act 2001 (other than because of an exemption granted to a class of financial market under section 791C of that Act).

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) unless paragraph (b) applies—the number of days in the financial year on which the entity operated the market; or

(b) if the entity operated 2 or more exempt markets in the financial year—the sum of the days worked out under paragraph (a) for each of those markets.

54 Tier 1 clearing and settlement facility operators

(1) A leviable entity forms part of the Tier 1 clearing and settlement facility operators sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australian CS facility licence that was granted in relation to a clearing and settlement facility that:

(a) is systemically important in Australia; and

(b) has a strong connection to the Australian financial system.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) unless paragraph (b) applies—the number of days in the financial year on which the entity operated the facility; or

(b) if the entity operated 2 or more clearing and settlement facilities of the kind mentioned in subsection (1) in the financial year—the sum of the days worked out under paragraph (a) for each of those facilities.

55 Tier 2 clearing and settlement facility operators

(1) A leviable entity forms part of the Tier 2 clearing and settlement facility operators sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australian CS facility licence that was granted under subsection 824B(2) of the Corporations Act 2001 in relation to a clearing and settlement facility that:

(a) is systemically important in Australia; and

(b) has no strong connection to the Australian financial system.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) unless paragraph (b) applies—the number of days in the financial year on which the entity operated the facility; or

(b) if the entity operated 2 or more clearing and settlement facilities of the kind mentioned in subsection (1) in the financial year—the sum of the days worked out under paragraph (a) for each of those facilities.

56 Tier 3 clearing and settlement facility operators

(1) A leviable entity forms part of the Tier 3 clearing and settlement facility operators sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australian CS facility licence that was granted in relation to a clearing and settlement facility that:

(a) is not systemically important in Australia; and

(b) has no strong connection to the Australian financial system.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) unless paragraph (b) applies—the number of days in the financial year on which the entity operated the facility; or

(b) if the entity operated 2 or more clearing and settlement facilities of the kind mentioned in subsection (1) in the financial year—the sum of the days worked out under paragraph (a) for each of those facilities.

57 Tier 4 clearing and settlement facility operators

(1) A leviable entity forms part of the Tier 4 clearing and settlement facility operators sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australian CS facility licence that authorises the entity to operate a clearing and settlement facility for the sole purpose of clearing and settling trades in the entity’s own shares.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) unless paragraph (b) applies—the number of days in the financial year on which the entity operated the facility; or

(b) if the entity operated 2 or more clearing and settlement facilities of the kind mentioned in subsection (1) in the financial year—the sum of the days worked out under paragraph (a) for each of those facilities.

58 Exempt CS facility operators

(1) A leviable entity forms part of the exempt CS facility operators sub‑sector in a financial year if, at any time in the financial year, the entity is the operator of a clearing and settlement facility that is exempt from the operation of the whole of Part 7.3 of the Corporations Act 2001.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) unless paragraph (b) applies—the number of days in the financial year on which the entity operated the facility; or

(b) if the entity operated 2 or more clearing and settlement facilities of the kind mentioned in subsection (1) in the financial year—the sum of the days worked out under paragraph (a) for each of those facilities.

59 Australian derivative trade repository operators

(1) A leviable entity forms part of the Australian derivative trade repository operators sub‑sector in a financial year if, at any time in the financial year, the entity operates a licensed derivative trade repository.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) unless paragraph (b) applies—the number of days in the financial year on which the entity operated the repository; or

(b) if the entity operated 2 or more licensed derivative trade repositories in the financial year—the sum of the days worked out under paragraph (a) for each of those facilities.

61 Retail over‑the‑counter derivatives issuers

(1) A leviable entity forms part of the retail over‑the‑counter derivatives issuers sub‑sector in a financial year if:

(a) the entity holds, at any time in the financial year, an Australian financial services licence that authorises the holder to provide both of the following financial services to retail clients:

(i) dealing in a financial product by issuing derivatives;

(ii) making a market for derivatives; and

(b) the entity is not a body regulated by APRA.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is the number of days in the financial year on which the entity holds a licence of the kind mentioned in subsection (1).

62 Wholesale electricity dealers

A leviable entity forms part of the wholesale electricity dealers sub‑sector in a financial year if, at any time in the financial year:

(a) the entity incurs liabilities as part of the ordinary business operations of the entity in dealing in, or making a market in, over‑the‑counter derivatives that relate to the wholesale price of electricity; and

(b) the entity is not:

(i) a body regulated by APRA; or

(ii) a participant in a financial market.

62A Benchmark administrators

(1) A leviable entity forms part of the benchmark administrators sub‑sector in a financial year if, at any time in the financial year, the entity holds a benchmark administrator licence to administer a financial benchmark.

Entity metric

(2) The leviable entity’s entity metric for the sub‑sector for the financial year is:

(a) unless paragraph (b) applies—the number of days in the financial year on which the entity administered the financial benchmark specified in the benchmark administrator licence; or

(b) if the entity administered 2 or more financial benchmarks specified in the benchmark administrator licence in the financial year—the sum of the days worked out under paragraph (a) for each of those financial benchmarks.

Subdivision 5.3—Sub‑sectors to which graduated levy component applies

62B Credit rating agencies

(1) A leviable entity forms part of the credit rating agencies sub‑sector in a financial year if, at any time in the financial year, the entity holds an Australian financial services licence that authorises the holder to provide general advice by issuing a credit rating.

Levy component

(2) The amount of a leviable entity’s levy component in respect of the sub‑sector for the financial year is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) the graduated levy component for the entity for the sub‑sector.

Note: For the graduated levy component, see section 10.

Entity metric

(3) The leviable entity’s entity metric for the sub‑sector for the financial year is the number of days in the financial year on which:

(a) the entity holds a licence of the kind mentioned in subsection (1); and

(b) there is a supervisory college for the entity.

(4) The minimum levy component for the sub‑sector is $2,000.

63 Corporate advisors

(1) A leviable entity forms part of the corporate advisors sub‑sector in a financial year if, at any time in the financial year:

(a) the entity:

(i) holds an Australian financial services licence; or

(ii) is exempt from the requirement to hold such a licence under paragraph 911A(2)(l) or subsection 926A(2) of the Corporations Act 2001 (other than because of an exemption under the ASIC Corporations (Foreign Financial Services Providers—Limited Connection) Instrument 2017/182); and

(b) the entity, or an authorised representative of the entity, provides or holds out that it provides, one or more of the financial services mentioned in subsection (2).

(2) For the purposes of paragraph (1)(b), the financial services are:

(a) financial product advice provided in Australia to a wholesale client in the course of advising on any of the following:

(i) takeover bids or merger proposals;

(ii) the structure, pricing, acquisition or disposal of assets or enterprises;

(iii) raising or reducing capital through the issue or acquisition of equities or debt; and

(b) dealing in a financial product in Australia by underwriting the issue, acquisition or sale of the product.

Levy component

(3) The amount of a leviable entity’s levy component in respect of the sub‑sector for the financial year is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) if the entity’s entity metric for the sub‑sector for the financial year exceeds the minimum levy threshold—the graduated levy component for the entity for the sub‑sector.

Note: For the graduated levy component, see section 10.

Entity metric

(4) The leviable entity’s entity metric for the sub‑sector for the financial year is the total gross revenue made in the financial year by the entity, and the authorised representative of the entity, from providing the financial services mentioned in subsection (2).

(5) The minimum levy component for the sub‑sector is $1,000.

(6) The minimum levy threshold for the sub‑sector is $100,000.

64 Large futures exchange participants

(1) A leviable entity forms part of the large futures exchange participants sub‑sector in a financial year if, at any time in the financial year, the entity is a participant in a large futures exchange.

Levy component

(2) The amount of a leviable entity’s levy component in respect of the sub‑sector for the financial year is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) 10% of the graduated levy component for the entity for the sub‑sector; and

(c) 90% of the graduated levy component for the entity for the sub‑sector.

Entity metric (messages)

(3) The leviable entity’s entity metric for the sub‑sector for the financial year is the number of messages that:

(a) are sent by the entity in the financial year to a large futures exchange; and

(b) are reported by the operator of the large futures exchange to ASIC’s Market Surveillance System; and

(c) are recognised by ASIC’s Market Surveillance System as orders or executed transactions.

(3A) For the purposes of subsection (3), 2 or more reports that relate to the same message, and contain the same information, are counted as one message.

Entity metric (lots)

(4) However, in working out the graduated levy component for the purposes of paragraph (2)(c), the leviable entity’s entity metric for the sub‑sector for the financial year is instead the number of lots that:

(a) are executed on, or reported to, a large futures exchange by the entity in the financial year; and

(b) are reported by the operator of the large futures exchange to ASIC’s Market Surveillance System; and

(c) are recognised by ASIC’s Market Surveillance System as executed lots.

(5) For the purposes of subsection (4), 2 or more reports that relate to the same lot, and contain the same information, are counted as one lot.

(6) The minimum levy component for the sub‑sector is $9,000.

65 Large securities exchange participants

(1) A leviable entity forms part of the large securities exchange participants sub‑sector in a financial year if, at any time in the financial year, the entity is a participant in a large securities exchange.

Levy component

(2) The amount of a leviable entity’s levy component in respect of the sub‑sector for the financial year is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) 10% of the graduated levy component for the entity for the sub‑sector; and

(c) 90% of the graduated levy component for the entity for the sub‑sector.

Entity metric (messages)

(3) The leviable entity’s entity metric for the sub‑sector for the financial year is the number of messages that:

(a) are sent by the entity in the financial year to a large securities exchange; and

(b) are reported by the operator of the large securities exchange to ASIC’s Market Surveillance System; and

(c) are recognised by ASIC’s Market Surveillance System as orders or executed transactions.

(3A) For the purposes of subsection (3), 2 or more reports that relate to the same message, and contain the same information, are counted as one message.

Entity metric (transactions)

(4) However, in working out the graduated levy component for the purposes of paragraph (2)(c), the leviable entity’s entity metric for the sub‑sector for the financial year is instead the number of transactions that:

(a) are executed on, or reported to, a large securities exchange by the entity in the financial year; and

(b) are reported by the operator of the large securities exchange to ASIC’s Market Surveillance System; and

(c) are recognised by ASIC’s Market Surveillance System as executed transactions.

(5) For the purposes of subsection (4), 2 or more reports that relate to the same transaction, and contain the same information, are counted as one transaction.

(6) The minimum levy component for the sub‑sector is $9,000.

66 Over‑the‑counter traders

(1) A leviable entity forms part of the over‑the‑counter traders sub‑sector in a financial year if, at any time in the financial year, the entity:

(a) holds an Australian financial services licence or is exempt from the requirement to hold such a licence under paragraph 911A(2)(l) or subsection 926A(2) of the Corporations Act 2001 (other than because of an exemption under the ASIC Corporations (Foreign Financial Services Providers—Limited Connection) Instrument 2017/182); and

(b) deals in, or holds out that it deals in, over‑the‑counter financial products by:

(i) acquiring over‑the‑counter financial products from professional investors; or

(ii) disposing of over‑the‑counter financial products to professional investors; or

(iii) issuing over‑the‑counter financial products to professional investors; and

(c) either:

(i) forms part of the corporate advisors sub‑sector (see section 63); or

(ii) is a related body corporate of an entity that forms part of the corporate advisors sub‑sector.

(1A) However, a leviable entity does not form part of the over‑the‑counter traders sub‑sector in a financial year if, at all times in the financial year that the entity deals in (or holds out that it deals in) over‑the‑counter financial products, the entity so deals (or so holds out) only in its capacity as an entity that forms part of one or more of the following sub‑sectors:

(a) the responsible entities sub‑sector (see section 35);

(b) the superannuation trustees sub‑sector (see section 36);

(c) the wholesale trustees sub‑sector (see section 37).

Levy component

(2) The amount of a leviable entity’s levy component in respect of the sub‑sector for the financial year is the sum of:

(a) the minimum levy component for the sub‑sector; and

(b) the graduated levy component for the entity for the sub‑sector.

Note: For the graduated levy component, see section 10.

Entity metric

(3) The leviable entity’s entity metric for the sub‑sector for the financial year is the number of persons who:

(a) ordinarily act on behalf of the entity or an authorised representative of the entity in the financial year; and

(b) in so acting have, at any time in the financial year, carried out one or more of the following activities in relation to dealing in an over‑the‑counter financial product with a professional investor:

(i) determining the terms on which the entity is willing to deal;