ASA 2012-1 |

Auditing Standard ASA 2012-1

Amending Standard to

ASA 570 Going Concern

Issued by the Auditing and Assurance Standards Board

ASA 2012-1 |

Auditing Standard ASA 2012-1

Amending Standard to

ASA 570 Going Concern

Issued by the Auditing and Assurance Standards Board

This Auditing Standard is available on the Auditing and Assurance Standards Board (AUASB) website: www.auasb.gov.au

Auditing and Assurance Standards Board Level 7, 600 Bourke Street Melbourne Victoria 3000 AUSTRALIA | Phone: (03) 8080 7400 Fax: (03) 8080 7450 E-mail: enquiries@auasb.gov.au

Postal Address: PO Box 204 Collins Street West Melbourne Victoria 8007 AUSTRALIA |

© 2012 Commonwealth of Australia. The text, graphics and layout of this Auditing Standard are protected by Australian copyright law and the comparable law of other countries. Reproduction within Australia in unaltered form (retaining this notice) is permitted for personal and non‑commercial use subject to the inclusion of an acknowledgment of the source. Requests and enquiries concerning reproduction and rights for commercial purposes within Australia should be addressed to the Executive Director, Auditing and Assurance Standards Board, PO Box 204, Collins Street West, Melbourne Victoria 8007. Otherwise, no part of the Auditing Standard may be reproduced, stored or transmitted in any form or by any means without the prior written permission of the AUASB except as permitted by law.

ISSN 1833-4393

PREFACE

AUTHORITY STATEMENT

Paragraphs

Application......................................................Aus 0.1-Aus 0.2

Operative Date.........................................................Aus 0.3

Introduction

Scope of this Auditing Standard..................................................1

Objective..................................................................2

Definition..................................................................3

Amendments to Auditing Standard

Amendments to ASA 570.......................................................4

The Auditing and Assurance Standards Board (AUASB) issues Auditing Standard ASA 2012-1 Amending Standard to ASA 570 Going Concern, pursuant to the requirements of the legislative provisions and the Strategic Direction explained below.

The AUASB is an independent statutory committee of the Australian Government established under section 227A of the Australian Securities and Investments Commission Act 2001, as amended (ASIC Act). Under section 336 of the Corporations Act 2001, the AUASB may make Auditing Standards for the purposes of the corporations legislation. These Auditing Standards are legislative instruments under the Legislative Instruments Act 2003.

Under the Strategic Direction given to the AUASB by the Financial Reporting Council (FRC), the AUASB is required, inter alia, to develop auditing standards that have a clear public interest focus and are of the highest quality.

This Auditing Standard makes amendments to Auditing Standard ASA 570 Going Concern.

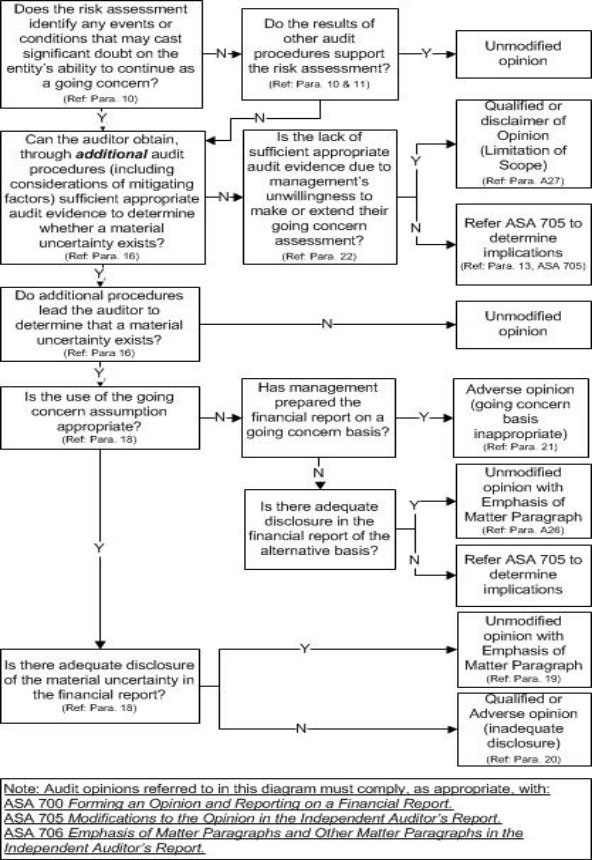

This Auditing Standard makes amendments to ASA 570 Going Concern comprising [Aus] Appendix 1 Linking Going Concern Considerations and Types of Audit Opinions.

The amendments are editorial improvements in nature and do not have an impact on the requirements of the Auditing Standard.

The Auditing and Assurance Standards Board (AUASB) makes this Auditing Standard ASA 2012-1 Amending Standard to ASA 570 Going Concern, pursuant to section 227B of the Australian Securities and Investments Commission Act 2001 and section 336 of the Corporations Act 2001.

Dated: 31 July 2012 M H Kelsall

Chairman - AUASB

Aus 0.1 This Auditing Standard applies to:

(a) an audit of a financial report for a financial year, or an audit of a financial report for a half-year, in accordance with the Corporations Act 2001; and

(b) an audit of a financial report, or a complete set of financial statements, for any other purpose.

Aus 0.2 This Auditing Standard also applies, as appropriate, to an audit of other historical financial information.

Aus 0.3 This Auditing Standard is operative for financial reporting periods commencing on or after 1 July 2012.

This Auditing Standard has been made for Australian legislative purposes and there is no equivalent International Standards on Auditing issued by the International Auditing and Assurance Standards Board (IAASB), an independent standard-setting board of the International Federation of Accountants (IFAC).