Part 1—Preliminary

1.01 Name of Regulations

These Regulations are the Superannuation Industry (Supervision) Regulations 1994.

1.03 Interpretation

(1) In these regulations, unless the contrary intention appears:

1997 Tax Act means the Income Tax Assessment Act 1997.

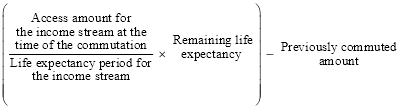

access amount, at a particular time (the access time) for a benefit supported by a superannuation interest (within the meaning of the 1997 Tax Act), means the sum of:

(a) the maximum amount payable if the benefit were commuted on the retirement phase start day for the benefit, as determined by the contract or rules for the provision of the benefit; and

(b) any instalments paid for the benefit after the retirement phase start day for the benefit and before the access time.

account‑based annuity means an annuity provided under a contract that:

(a) is described in paragraph 1.05(11A)(a); and

(b) meets the standards of subregulation 1.05(11A).

account‑based pension means a pension that is provided in accordance with the rules of a fund that:

(a) are described in paragraph 1.06(9A)(a); and

(b) meet the standards of subregulation 1.06(9A).

accumulation fund means a regulated superannuation fund that is not a defined benefit fund.

accumulation interest means a superannuation interest that is not a defined benefit interest.

Act means the Superannuation Industry (Supervision) Act 1993.

adjusted base amount, in relation to a non‑member spouse at a particular date, means the adjusted base amount applicable to the non‑member spouse at that date worked out under Division 6.1A of the Family Law (Superannuation) Regulations 2001.

advance instalment of surcharge means the advance instalment payable under section 11 of the Superannuation Contributions Tax (Assessment and Collection) Act 1997.

AFCA scheme has the same meaning as in Chapter 7 of the Corporations Act 2001.

allocated pension means a pension that is provided under rules of a superannuation fund that meet the standards of subregulation 1.06(4).

allot, for Division 6.7, means to credit an amount from a member’s account to another account in the regulated superannuation fund held by, or created for, the receiving spouse otherwise than by transfer or roll‑over.

base amount payment split, in relation to a superannuation interest, means a payment split under which a base amount is allocated to the non‑member spouse in relation to the interest under Part VIIIB of the Family Law Act 1975.

benefit certificate has the meaning given by section 10 of the SG(A) Act.

capital gains tax exempt component has the same meaning as CGT exempt component in subsection 27A(1) of the Tax Act as in force immediately before 1 July 2007.

child contributions means contributions that are made to a regulated superannuation fund in respect of a child, other than:

(a) contributions made in respect of the child by, or on behalf of, an employer of the child; and

(b) contributions made by a child in respect of himself or herself.

Co‑contribution Act means the Superannuation (Government Co‑contribution for Low Income Earners) Act 2003.

commencement day, in relation to a pension or an annuity, means the first day of the period to which the first payment of the pension or annuity relates.

contributions, in relation to a fund, includes:

(a) payments of shortfall components to the fund; and

(b) payments to the fund from the Superannuation Holding Accounts Special Account;

but does not include benefits that have been rolled over or transferred to the fund.

deferred superannuation income stream means a benefit supported by a superannuation interest (within the meaning of the 1997 Tax Act) if the contract or rules for the provision of the benefit provides for payments of the benefit:

(a) to start more than 12 months after the superannuation interest is acquired; and

(b) to be made at least annually afterwards.

defined benefit fund, subject to regulation 1.03AAA, means:

(a) a public sector superannuation scheme that:

(i) is a regulated superannuation fund; and

(ii) has at least 1 defined benefit member; or

(b) a regulated superannuation fund (other than a public sector superannuation scheme):

(i) that has at least 1 defined benefit member; and

(ii) some or all of the contributions to which (out of which, together with earnings on those contributions, the benefits are to be paid) are not paid into a fund, or accumulated in a fund, in respect of any individual member but are paid into and accumulated in a fund in the form of an aggregate amount.

defined benefit interest has the meaning given by regulation 1.03AA.

defined benefit member means a member who is entitled, on retirement or termination of employment, to be paid a benefit defined wholly or in part by reference to:

(a) the member’s salary on retirement, termination of employment or an earlier date; or

(b) the member’s salary averaged over a period before retirement; or

(c) both (a) and (b); or

(d) a specified amount.

defined benefit pension means a pension mentioned in section 10 of the Act, other than:

(a) a pension wholly determined by reference to policies of life assurance purchased or obtained by the trustee of a regulated superannuation fund, solely for the purposes of providing benefits to members of that fund; or

(b) an allocated pension; or

(c) a market linked pension; or

(d) an account‑based pension.

defined benefit sub‑fund means a sub‑fund of a defined benefit fund that:

(a) has at least one defined benefit member; and

(b) satisfies the conditions mentioned in section 69A of the Act.

eligible rollover fund has the same meaning as in Part 24 of the Act.

Note: As to what is an eligible rollover fund for Part 24 of the Act, see section 242 of the Act and regulation 10.01.

eligible spouse contribution means a contribution made by an individual to a superannuation fund:

(a) to provide superannuation benefits for the individual’s spouse, whether or not the benefits would be payable to the dependants of the individual’s spouse if the spouse dies before or after becoming entitled to receive the benefits; and

(b) in circumstances in which the individual:

(i) could not have deducted the contribution under section 82AAC of the Tax Act in the 2006–07 income year or a previous year; and

(ii) cannot deduct the contribution under Subdivision 290‑B of the 1997 Tax Act in the 2007–08 income year or a later year.

eligible termination payment has the same meaning as in Subdivision AA of Division 2 of Part III of the Tax Act.

employer contribution, in relation to a regulated superannuation fund, means a contribution by, or on behalf of, an employer‑sponsor of the fund.

EPSSS means an exempt public sector superannuation scheme.

first half of the life expectancy period, for a benefit supported by a superannuation interest (within the meaning of the 1997 Tax Act), means the number of days in the period:

(a) starting on the retirement phase start day for the benefit; and

(b) ending when the number of days equal to the life expectancy period for the benefit divided by 2, and rounded down to the nearest whole number, have passed.

flag lifting agreement means a flag lifting agreement under Part VIIIB of the Family Law Act 1975.

FSR commencement has the same meaning as in section 1410 of the Corporations Act 2001.

Note: The FSR commencement is the commencement of item 1 of Schedule 1 to the Financial Services Reform Act 2001.

full‑time, in relation to being gainfully employed, means gainfully employed for at least 30 hours each week.

gainfully employed means employed or self‑employed for gain or reward in any business, trade, profession, vocation, calling, occupation or employment.

growth phase has the meaning given by regulation 1.03AB.

Immigration Department means the Department administered by the Minister administering the Migration Act 1958.

industrial authority means:

(a) a court, or a tribunal or other body or person, constituted under a law of the Commonwealth, a State or a Territory with power of conciliation or arbitration in relation to industrial disputes; or

(b) a special board constituted under the law of a State relating to factories.

life expectancy has the same meaning as life expectation factor in section 27H of the Tax Act.

life expectancy period, for a benefit supported by a superannuation interest (within the meaning of the 1997 Tax Act), means the number of days worked out by:

(a) calculating the number of years in the complete expectation of life of:

(i) if the primary beneficiary of the benefit is alive on the retirement phase start day for the benefit—the primary beneficiary; or

(ii) otherwise—the person (if any) to whom the benefit was transferred because of the primary beneficiary’s death, if at the time of that death the person was eligible under paragraph 6.21(2)(b) to be paid a benefit;

on the retirement phase start day for the benefit as worked out using the prescribed Life Tables; and

(b) rounding the result down to the nearest whole number of years; and

(c) converting those years to a number of days, assuming 365 days in a year.

lost member has the meaning given by regulation 1.03A.

lost RSA holder has the meaning given by regulation 1.06 of the RSA Regulations.

market linked annuity means an annuity provided under a contract that meets the standards of subregulation 1.05(10).

market linked income stream means an annuity provided under a contract that meets the standards of subregulation 1.05(10), or a pension paid under rules that meet the standards of subregulation 1.06(8).

market linked pension means a pension paid under rules that meet the standards of subregulation 1.06(8).

member, except in Part 2, means:

(a) in relation to an approved deposit fund—a depositor in the fund; and

(b) in relation to a regulated superannuation fund—a member of the fund; and

(c) in relation to a PST—a unit‑holder in the PST.

Note: The meaning of the term ‘member’ in Part 2 is defined in subregulation 2.01(2).

member spouse, in relation to a superannuation interest that is subject to a payment split, means the person who is the member spouse in relation to the interest under Part VIIIB of the Family Law Act 1975.

minimum requisite benefit, in relation to a member, means the benefit certified by an actuary in a relevant benefit certificate as the minimum benefit in respect of the member.

non‑member spouse, in relation to a superannuation interest that is subject to a payment split, means the person who is the non‑member spouse in relation to the interest under Part VIIIB of the Family Law Act 1975.

old Regulations means these Regulations as in force immediately before the FSR commencement.

operative time, for a payment split, means the operative time under Part VIIIB of the Family Law Act 1975 for the payment split.

part‑time, in relation to being gainfully employed, means gainfully employed for at least 10 hours, and less than 30 hours, each week

payment split means a payment split under Part VIIIB of the Family Law Act 1975.

payment split notice means a notice given by a trustee under regulation 7A.03.

pension age:

(a) in relation to a person other than a person mentioned in paragraph (b)—has the meaning given by subsections 23(5A), (5B), (5C) or (5D) of the Social Security Act 1991; and

(b) in relation to a person who is a veteran within the meaning of the Veterans’ Entitlement Act 1986—has the meaning that it has in section 5QA of that Act.

percentage‑only interest has the meaning given by Part VIIIB of the Family Law Act 1975.

percentage payment split, in relation to a superannuation interest, means a payment split under a superannuation agreement, flag lifting agreement or splitting order that specifies a percentage that is to apply to all splittable payments in respect of the interest.

prescribed Life Tables means the Life Tables prescribed by section 7 of the Income Tax Assessment (1936 Act) Regulation 2015, as if references in that section to:

(a) an annuity included a reference to a benefit supported by a superannuation interest (within the meaning of the 1997 Tax Act); and

(b) the year in which the annuity first commences to be payable were a reference to the year that includes the retirement phase start day for the benefit.

protected member has the meaning given by regulation 1.03B.

PST means a pooled superannuation trust.

receiving spouse has the meaning given by regulation 6.46.

registered company auditor has the same meaning as in section 9 of the Corporations Act 2001.

relevant benefit certificate, in relation to a regulated superannuation fund, means a benefit certificate that relates to a defined benefit superannuation scheme (within the meaning of the SG(A) Act) of which the fund forms part.

relevant entity means:

(a) a public offer entity; or

(b) an approved deposit fund.

Note: The expression relevant entity is defined in the same terms as in section 22 of the Act.

reserves, in relation to a superannuation entity, means reserves maintained under section 115 of the Act.

retirement phase has the same meaning as in the 1997 Tax Act.

retirement phase start day, for a benefit supported by a superannuation interest (within the meaning of the 1997 Tax Act), means:

(a) if the benefit is a deferred superannuation income stream—the later of:

(i) the day the primary beneficiary satisfies a condition of release mentioned in item 101, 102, 102A, 103 or 106 of Schedule 1; and

(ii) the day the superannuation interest is acquired; or

(b) otherwise—the day that payments of the benefit start to be payable.

reviewable decision means:

(a) a decision of APRA under paragraph 1.05(2)(c) refusing to approve a sum payable as benefit; or

(b) a decision of the Regulator under paragraph 1.06(2)(c) refusing to approve a sum payable as benefit; or

(c) a decision of the Regulator refusing to approve the use of a factor under subregulation 1.08(2); or

(d) a decision of APRA under paragraph 4.08A(2)(e) refusing to approve an arrangement for management and control of a fund; or

(e) a decision of the Regulator under paragraph 4.12(2)(b), 6.27B(b) or 7A.16(8)(b) to not determine the form of consent; or

(f) a decision of APRA to refuse to suspend or vary an obligation of a trustee under subregulation 6.37(6); or

(g) a decision of the Regulator under subparagraph 7A.03J(2)(a)(ii) refusing to allow a longer period for a rollover or transfer of a non‑member spouse’s interest; or

(h) a decision of the Regulator under paragraph 7A.03K(2)(b) or 7A.13(7)(b) refusing to allow a longer period to pay a lump sum; or

(i) a decision of the Regulator under subparagraph 7A.12(4)(a)(ii) refusing to allow a longer period for rolling over or transferring transferable benefits; or

(j) a decision of the Regulator under paragraph 7A.16(3)(b) refusing to allow a longer period to allocate, rollover or transfer non‑member spouse entitlements; or

(k) a decision of the Regulator to give a direction to a trustee to obtain a new or a replacement funding and solvency certificate under subregulation 9.09(1A); or

(l) a decision of the Regulator under subregulation 9.24(2) refusing to approve an actuary’s recommendation for a defined benefit fund; or

(m) a decision of the Regulator under subregulation 9.44(2) refusing to approve an actuary’s recommendation for an accumulation fund; or

(n) a decision of APRA refusing to approve a proposed element of an actuarial basis for calculation of value A under subregulation 12.05(5) or (6); or

(o) a decision of APRA refusing to approve a proposed assumption or element of an actuarial basis for calculation of value B under subregulation 12.06(5); or

(p) a decision of APRA under regulation 12.08 to specify a day on or before which an application is to be made; or

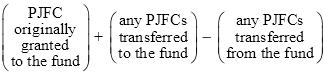

(q) a decision of APRA refusing to approve an application to transfer a PJFC under subregulation 12.12(2) or 12.13(2); or

(r) a decision of APRA under regulation 12.14 to revoke an approval of an application to transfer a PJFC; or

(s) a decision of the Regulator refusing to consent to an alteration of accrued benefits under subparagraph 13.16(2)(a)(ii) or (d)(ii); or

(t) a decision of the Regulator to confirm or vary a reviewable decision under regulation 13.25.

RSA Act means the Retirement Savings Accounts Act 1997.

RSA holder has the same meaning given to the term holder in section 9 of the RSA Act.

RSA institution has the meaning given by section 11 of the RSA Act.

RSA Regulations means the Retirement Savings Accounts Regulations.

SG(A) Act means the Superannuation Guarantee (Administration) Act 1992.

shortfall component has the same meaning as in the SG(A) Act.

splittable payment means a splittable payment under Part VIIIB of the Family Law Act 1975.

splitting order means a splitting order under Part VIIIB of the Family Law Act 1975.

successor fund, in relation to a transfer of benefits of a member from a fund (called the original fund), means a fund which satisfies the following conditions:

(a) the fund confers on the member equivalent rights to the rights that the member had under the original fund in respect of the benefits;

(b) before the transfer, the trustee of the fund has agreed with the trustee of the original fund that the fund will confer on the member equivalent rights to the rights that the member had under the original fund in respect of the benefits.

superannuation agreement means a superannuation agreement under Part VIIIB of the Family Law Act 1975.

superannuation contributions surcharge means the superannuation contributions surcharge imposed by the Superannuation Contributions Tax Imposition Act 1997.

Superannuation Holding Accounts Special Account means the Special Account established by section 8 of the Small Superannuation Accounts Act 1995.

superannuation income stream has the same meaning as in the 1997 Tax Act.

superannuation lump sum has the meaning given by subsection 995‑1(1) of the 1997 Tax Act.

Tax Act means the Income Tax Assessment Act 1936.

traditional life insurance policy means a life policy within the meaning of section 9 of the Life Insurance Act 1995 if:

(a) the policy includes an investment component; and

(b) the premium is not dissected (whether by reference to the investment component or otherwise); and

(c) the sum insured, together with bonuses (if any), is payable only on:

(i) the death of the life insured; or

(ii) the occurrence of the earlier of the death of the life insured and the attainment by the life insured of the age specified in the policy.

transferable benefits, in relation to a superannuation interest that is subject to a payment split and in relation to the non‑member spouse in relation to that interest, means benefits that are equal to:

(a) if the payment split is a base amount payment split and an adjusted base amount applies to the non‑member spouse when the benefits are transferred—the adjusted base amount less the amount of any fees payable by the non‑member spouse in respect of the payment split; or

(b) if the payment split is a base amount payment split and an adjusted base amount does not apply to the non‑member spouse when the benefits are transferred—the base amount allocated to the non‑member spouse, within the meaning of regulation 45 of the Family Law (Superannuation) Regulations 2001, less the amount of any fees payable by the non‑member spouse in respect of the payment split; or

(c) if the payment split is a percentage payment split:

(i) for an entitlement, in respect of an accumulation interest in the growth phase that is not a partially vested accumulation interest, to which subparagraph (ii) does not apply—the amount in relation to the interest at the time when the benefits are transferred, determined in the way in which a court would determine an amount in accordance with regulation 28 and subregulation 31(2A) of the Family Law (Superannuation) Regulations 2001, multiplied by the specified percentage, less the amount of any fees payable by the non‑member spouse in respect of the payment split; or

(ii) for an entitlement in respect of an interest in a self‑managed superannuation fund—the amount in relation to the interest at the time when the benefits are transferred, determined by a method that a court might use if the court were acting under paragraph 90MT(2)(b) of the Family Law Act 1975, multiplied by the specified percentage, less the amount of any fees payable by the non‑member spouse in respect of the payment split; or

(iii) for an entitlement in respect of any other interest—the amount in relation to the interest at the time when the benefits are transferred, determined in the way in which a court would determine an amount in accordance with the relevant method in Part 5 of the Family Law (Superannuation) Regulations 2001, multiplied by the specified percentage, less the amount of any fees payable by the non‑member spouse in respect of the payment split.

unfunded public sector superannuation scheme means a regulated superannuation fund that is declared to be an unfunded defined benefits superannuation scheme under regulation 2A of the Superannuation Contributions Tax (Assessment and Collection) Regulations 1997.

withdrawal benefit, in relation to a member of a superannuation entity, means the total amount of the benefits that would be payable to:

(a) the member; and

(b) the trustee of another superannuation entity or an EPSSS in respect of the member; and

(c) an RSA in respect of the member; and

(d) another person or entity because of a payment split in respect of the member’s interest in the superannuation entity;

if the member voluntarily ceased to be a member.

(2) In these Regulations, other than Part 2:

fund means:

(a) an approved deposit fund; or

(b) a regulated superannuation fund.

Note: For the meaning of fund in Part 2, see subregulation 2.01(3).

1.03A Lost member

(1) A member of a fund is taken to be a lost member at a particular time if:

(a) the member is uncontactable, that is, if and only if:

(i) either:

(A) the fund has never had an address (whether non‑electronic or electronic) for the member; or

(B) the trustee of the fund has made one or more attempts to send written communications to the member at the member’s last known address (or addresses), and the trustee believes, on reasonable grounds, that the member can no longer be contacted at any address known to the fund; and

(ia) the member has not contacted the fund (whether by written communication or otherwise) within the last 12 months of the member’s membership of the fund; and

(ib) the member has not accessed details about the member’s superannuation interest in the fund from any electronic facility provided by the fund within the last 12 months of the member’s membership of the fund; and

(ii) the fund has not received a contribution or rollover in respect of the member within the last 12 months of the member’s membership of the fund; or

(b) the member is an inactive member, that is, if and only if:

(i) he or she has been a member of the fund for longer than 2 years; and

(ia) he or she was, at the time he or she joined the fund, a person in respect of whom there was in effect a contribution arrangement of the kind referred to in subsection 16(5) of the Act (which deals with the definition of standard employer‑sponsored member); and

(ii) the fund has not received a contribution or rollover in respect of him or her within the last 5 years of his or her membership of the fund; or

(c) the member joined the fund from another fund or an EPSSS as a lost member; or

(ca) the member joined the fund from an RSA provider as a lost RSA holder;

unless:

(d) within the last 2 years of the member’s membership, the trustee of the fund has verified that the member’s address is correct and has no reason to believe that that address is now incorrect; or

(e) the member is permanently excluded from being a lost member.

(1A) To avoid doubt, for the purposes of this regulation, a written communication includes a written communication by non‑electronic means or by electronic means.

(2) For the purposes of subregulation (1), and subject to subregulation (3), a member of a fund is permanently excluded from being a lost member if:

(a) the member is an inactive member who has indicated by a positive act (for example, deferring a benefit in the fund) that he or she wishes to continue to be a member of the fund; or

(b) the member has contacted the fund at any time after the time at which he or she joined the fund and indicated that he or she wishes to continue being a member of the fund; or

(c) the member is a member of a self managed superannuation fund.

(3) The trustee of a fund may decide that:

(a) a member, a class of members, or all members of the fund cannot be permanently excluded from becoming lost members; or

(b) a member who is, a class of members who are, or all members of the fund who are permanently excluded from being lost is or are not to continue being permanently excluded from being lost.

Note: The consequences of a member becoming a lost member are:

(a) that the trustee of the fund must report certain details to the Commissioner (see regulation 5 of the Superannuation (Unclaimed Money and Lost Members) Regulations 1999); and

(b) that, if the member is transferred to another fund or an EPSSS (the transferee fund), the trustee of the transferring fund must supply certain information about the member to the trustee of the transferee fund (see regulation 7.9.81 of the Corporations Regulations 2001).

There may also be consequences regarding the information to be supplied to the member (see regulation 7.9.61 of, and Part 14 of Schedule 10A to, the Corporations Regulations 2001).

1.03AA Defined benefit interest

(1) A superannuation interest is a defined benefit interest if it is:

(a) an interest in an unfunded public sector superannuation scheme that has at least 1 defined benefit member; or

(b) an interest that entitles the member who holds the interest, when benefits in respect of the interest become payable, to be paid a benefit defined, wholly or in part, by reference to one or more of the following:

(i) the amount of:

(A) the member’s salary at the date of the termination of the member’s employment, the date of the member’s retirement, or another date; or

(B) the member’s salary averaged over a period; or

(C) salary, or allowance in the nature of salary, payable to another person (for example, a judicial officer, a member of the Commonwealth or a State Parliament, a member of the Legislative Assembly of a Territory);

(ii) a specified amount;

(iii) specified conversion factors.

(2) However, a superannuation interest is not a defined benefit interest if the only benefits defined by reference to any of the amounts or factors mentioned in subparagraphs (1)(b)(i) to (iii) are benefits payable on death or invalidity.

1.03AAA Defined benefit fund

For the following provisions, a fund is taken to be a defined benefit fund if at least one member of the fund receives a defined benefit pension:

(a) paragraph (c) of the definition of investment return in subregulation 5.01(1);

(b) subregulation 5.04(3);

(c) regulation 7.05;

(d) Divisions 9.3 to 9.5.

1.03AB Meaning of growth phase

(1) A superannuation interest is taken to be in the growth phase at a particular date if the member satisfies 1 of the following requirements at that date:

(a) the member has not satisfied a relevant condition of release;

(b) the member has satisfied a relevant condition of release but no benefit has been paid in respect of the superannuation interest, and no action has been taken by or for the member under the governing rules of the fund to cash any benefit that the member is entitled to be paid as a result of satisfying the condition of release;

(c) the member has satisfied a relevant condition of release and a benefit (other than a benefit that is paid as a pension) has been paid to or for the benefit of the member or, if the member has died, to his or her legal personal representative, but no action has been taken by or for the member, or his or her legal personal representative, under the governing rules of the fund to receive any other benefit that the member, or his or her estate, is entitled to be paid as a result of satisfying the condition of release.

(2) In this regulation:

relevant condition of release means a condition of release mentioned in item 101, 102, 103, 106, 108, 201, 202, 203 or 206 of Schedule 1.

1.03C Meaning of permanent incapacity

For subsection 10(1) of the Act, a member of a superannuation fund or an approved deposit fund is taken to be suffering permanent incapacity if a trustee of the fund is reasonably satisfied that the member’s ill‑health (whether physical or mental) makes it unlikely that the member will engage in gainful employment for which the member is reasonably qualified by education, training or experience.

1.04 Prescribed matters (Act, s 10)

(1) The purpose of this regulation is to prescribe matters for the purposes of various definitions in section 10 of the Act.

Defined benefit member

(2) For paragraph 10(1A)(b) of the Act, subregulations (3) and (3A) set out circumstances in which a member of a superannuation fund is to be taken to be a defined benefit member for section 20B or Part 2C of the Act.

(3) A circumstance is that the member:

(a) is a member of the scheme established under the Military Superannuation and Benefits Act 1991 (the military superannuation scheme); or

(b) holds an interest, as a non‑member spouse within the meaning of section 90MD of the Family Law Act 1975, in the military superannuation scheme; or

(c) has a preserved benefit in the military superannuation scheme; or

(d) has an ancillary account in the military superannuation scheme; or

(e) both:

(i) is a member of the scheme established under the Defence Force Retirement and Death Benefits Act 1973; and

(ii) has an ancillary account in the military superannuation scheme.

(3A) A circumstance is that the member:

(a) holds an interest, as a non‑member spouse within the meaning of section 90MD of the Family Law Act 1975, in a superannuation scheme established under the Superannuation Act 1976 or the Superannuation Act 1990; or

(b) has made an election under section 137 of the Superannuation Act 1976; or

(c) is a preserved benefit member within the meaning of the Public Sector Superannuation Scheme Trust Deed, as in force from time to time; or

(d) has either of the following in the scheme established under the Superannuation (State Public Sector) Act 1990 (Qld):

(i) a capital guaranteed interest in a voluntary preservation plan;

(ii) a deferred retirement benefit amount; or

(e) both:

(i) is covered by the Crown Employees (Fire and Rescue NSW Firefighting Staff Death and Disability) Award 2012 (the 2012 award) or by an award that replaces the 2012 award (a successor award); and

(ii) would be entitled, on the occurrence of an event mentioned in any of the following clauses, to a pension or lump sum mentioned in that clause:

(A) clause 7 of the 2012 award, or an equivalent clause of a successor award;

(B) clause 8 of the 2012 award, or an equivalent clause of a successor award;

(C) clause 10 of the 2012 award, or an equivalent clause of a successor award;

(D) clause 11 of the 2012 award, or an equivalent clause of a successor award.

Excluded approved deposit fund

(4) For the purposes of paragraph (b) of the definition of excluded approved deposit fund in section 10 of the Act, the following condition is specified, namely, that the fund must be:

(a) a fund established before 1 July 1994; or

(b) a fund that was established on or after 1 July 1994 using eligible termination payments (within the meaning of the Tax Act as in force when the fund was established) of the fund’s beneficiary that had an initial value of at least $400 000; or

(c) a fund that is established after 1 July 2007 using a superannuation lump sum or an employment termination payment (within the meaning of the 1997 Tax Act) of the fund’s beneficiary that had an initial value of at least $400 000.

Exempt public sector superannuation scheme

(4A) For the purposes of the definition of exempt public sector superannuation scheme in section 10 of the Act the schemes listed in Schedule 1AA are specified.

(4AA) A scheme that is listed, or established by or operated under legislation that is listed, in Schedule 1AA ceases to be an exempt public sector superannuation scheme at the time it is registered as a registrable superannuation entity under Division 2 of Part 2B of the Act.

(4B) If a scheme listed in Schedule 1AA is re‑named, the reference to that scheme includes the scheme as so re‑named.

(4C) Subregulation (4A) has effect in relation to a scheme specified in Part 1 of Schedule 1AA in respect of the 1994–95 and 1995–96 years of income of that scheme.

(4D) Subregulation (4A) applies in relation to a scheme specified in Part 2 of Schedule 1AA during the 1996‑97 year of income of that scheme.

(4E) Subregulation (4A) applies in relation to a scheme specified in Part 3 of Schedule 1AA during the 1997‑1998 year of income, and subsequent years of income, of that scheme.

Pooled superannuation trust

(5) For the purposes of paragraph (b) of the definition of pooled superannuation trust in section 10 of the Act, the definition applies to a unit trust that is:

(a) used only for investing the following kinds of assets:

(i) assets of a regulated superannuation fund;

(ii) assets of an approved deposit fund;

(iii) assets of a PST;

(iv) complying superannuation assets of a life insurance company within the meaning of the 1997 Tax Act;

(v) segregated exempt assets of a life insurance company within the meaning of the 1997 Tax Act; and

Note 1: PST is defined in regulation 1.03 to mean a pooled superannuation trust.

Note 2: Complying superannuation asset, life insurance company and segregated exempt assets are defined in subsection 995‑1(1) of the 1997 Tax Act.

(b) a resident unit trust within the meaning of section 102Q of the Tax Act; and

(c) a trust in relation to which each of the following circumstances applies:

(i) the trustee has confirmed in writing an intention to have the trust treated as a PST;

(ii) the confirmation was given to APRA, in the approved form, and signed and dated by the trustee;

(iii) the confirmation was given not later than:

(A) the time of lodgment, in accordance with subsection 36(1) of the Act, of the first return in relation to the trust after 12 July 2000 (the time of lodgment); or

(B) such later time as allowed, in writing, by APRA, either generally or in a particular case and whether allowed before or after the time of lodgment;

(iv) the confirmation has not been withdrawn.

(6) The trustee of a unit trust may confirm an intention under paragraph (5)(c) despite anything in the governing rules of the unit trust.

(7) The trustee of a unit trust mentioned in subregulation (6) must inform APRA in writing as soon as practicable after the unit trust ceases to be a PST because paragraph (5)(a) or (b) ceases to apply to the trust.

(8) The trustee may withdraw the confirmation of an intention under paragraph (5)(c) by giving to APRA a notice of the withdrawal that is signed and dated by the trustee.

1.04AAAA Interdependency relationships (Act s 10A)

(1) For paragraph 10A(3)(a) of the Act, the following matters are to be taken into account in determining whether 2 persons have an interdependency relationship, or had an interdependency relationship immediately before the death of 1 of the persons:

(a) all of the circumstances of the relationship between the persons, including (where relevant):

(i) the duration of the relationship; and

(ii) whether or not a sexual relationship exists; and

(iii) the ownership, use and acquisition of property; and

(iv) the degree of mutual commitment to a shared life; and

(v) the care and support of children; and

(vi) the reputation and public aspects of the relationship; and

(vii) the degree of emotional support; and

(viii) the extent to which the relationship is one of mere convenience; and

(ix) any evidence suggesting that the parties intend the relationship to be permanent;

(b) the existence of a statutory declaration signed by one of the persons to the effect that the person is, or (in the case of a statutory declaration made after the end of the relationship) was, in an interdependency relationship with the other person.

(2) For paragraph 10A(3)(b) of the Act, 2 persons have an interdependency relationship if:

(a) they satisfy the requirements of paragraphs 10A(1)(a) to (c) of the Act; and

(b) one or each of them provides the other with support and care of a type and quality normally provided in a close personal relationship, rather than by a mere friend or flatmate.

Examples of care normally provided in a close personal relationship rather than by a friend or flatmate:

1. Significant care provided for the other person when he or she is unwell.

2. Significant care provided for the other person when he or she is suffering emotionally.

(3) For paragraph 10A(3)(b) of the Act, 2 persons have an interdependency relationship if:

(a) they have a close personal relationship; and

(b) they do not satisfy the other requirements set out in subsection 10A(1) of the Act; and

(c) the reason they do not satisfy the other requirements is that they are temporarily living apart.

Example for paragraph (3)(c): One of the persons is temporarily working overseas or is in gaol.

(4) For paragraph 10A(3)(b) of the Act, 2 persons have an interdependency relationship if:

(a) they have a close personal relationship; and

(b) they do not satisfy the other requirements set out in subsection 10A(1) of the Act; and

(c) the reason they do not satisfy the other requirements is that either or both of them suffer from a disability.

(5) For paragraph 10A(3)(b) of the Act, 2 persons do not have an interdependency relationship if 1 of them provides domestic support and personal care to the other:

(a) under an employment contract or a contract for services; or

(b) on behalf of another person or organisation such as a government agency, a body corporate or a benevolent or charitable organisation.

1.04AAA Modified meaning of member (Act s 15B)

(1) This regulation applies if:

(a) a superannuation interest in a fund is subject to a payment split, or a non‑member spouse interest has been created under regulation 7A.03B; and

(b) the non‑member spouse in relation to the interest was not a member of the fund immediately before the operative time for the payment split.

(2) For the purposes of the provisions of the Act set out in Table 1, the non‑member spouse is to be treated as being a member of the fund in which the interest is held from the later of:

(a) the operative time for the payment split; and

(b) the time that the trustee receives the agreement or order under which the payment split is effected.

Table 1

Item | Provision |

1 | subsection 17A, except subsection (5) (definition of self managed superannuation fund) |

2 | section 65 (lending to members of regulated superannuation fund prohibited) |

3 | Part 8 (in‑house asset rules applying to regulated superannuation funds) |

(3) For subsection 17A(5) of the Act, the non‑member spouse is to be treated as being a member of the fund in which the interest is held from the later of:

(a) the end of 6 months after the operative time for the payment split; and

(b) the end of 6 months after the time that the trustee receives the agreement or order under which the payment split is effected.

(4) For regulation 1.03A, the non‑member spouse is to be treated as being a member of the fund in which the interest is held from the operative time for the payment split.

(5) For subsection 17A(5) of the Act, a non‑member spouse who became a member of a fund as a result of the creation of a non‑member spouse interest under Division 7A.1A is not treated as a member of the fund until the earlier of:

(a) 6 months after the operative time for the payment split; and

(b) the time that the non‑member spouse’s interest in the fund is confirmed under regulation 7A.03H or 7A.03I.

1.04A Specified body or person (Act s 19)

For subsection 19(4) of the Act, the Commissioner of Taxation is specified.

1.04AA Self managed superannuation funds—persons not taken to be employees (Act s 17A(8))

(1) For the purposes of paragraph 17A(8)(b) of the Act, a class of persons is a specified class if it comprises persons each of whom is, in relation to a member of a superannuation fund, an exempt person mentioned in subregulation (2).

(2) A person is an exempt person in relation to a member of a superannuation fund if:

(a) the person is an employer‑sponsor of the fund; and

(b) the member is a director of the employer‑sponsor.

(3) For the purposes of paragraph 17A(8)(b) of the Act, a class of persons is a specified class if it comprises persons each of whom is a member of a superannuation fund in relation to which the following circumstances exist:

(a) the person is the employer, but not a relative, of a member of the fund (the employee);

(b) another member is the employer, and a relative, of that employee.

Part 1A—Annuities and pensions

Division 1A.1

1.05A Interpretation

In this Division, unless a contrary intention appears:

rolled over means paid as a superannuation lump sum within the superannuation system.

1.05 Meaning of annuity (Act, s 10)

(1) A benefit that is provided by a life insurance company or a registered organisation is taken to be an annuity for the purposes of the Act if:

(a) it arises under a contract that:

(i) meets the standards of subregulation (11A) or 1.06A(2); and

(ii) does not permit the capital supporting the annuity to be added to by way of contribution or rollover after the annuity has commenced; and

(b) for a benefit purchased on or after 3 August 1993 and before 1 July 2007—it is purchased with the whole or part of a rolled over amount within the meaning given to that term by section 27A of the Tax Act; and

(c) for a benefit purchased on or after 1 July 2007—it is purchased with the whole or part of:

(i) a roll‑over superannuation benefit within the meaning of the 1997 Tax Act; or

(ii) a directed termination payment within the meaning of the Income Tax (Transitional Provisions) Act 1997; and

(d) in the case of a contract to which paragraph (11A)(a) applies and that meets the standards of subregulation (11A)—the contract also meets the standards of regulation 1.07D; and

(e) in the case of a contract to which paragraph (11A)(b) applies and that meets the standards of subregulation (11A)—the contract also meets the standards of regulation 1.07B.

(1A) A benefit that is provided by a life insurance company or a registered organisation that commenced to be paid before 20 September 2007 is taken to be an annuity for the purposes of the Act if:

(a) it arises under a contract that meets the standards of subregulation (2), (4), (6), (7), (8), (9) or (10); and

(b) for a benefit purchased on or after 3 August 1993 and before 1 July 2007—it is purchased with the whole or part of a rolled over amount within the meaning given to that term by section 27A of the Tax Act; and

(c) for a benefit purchased on or after 1 July 2007 and before 20 September 2007—it is purchased with the whole or part of:

(i) a roll‑over superannuation benefit within the meaning of the 1997 Tax Act; or

(ii) a directed termination payment within the meaning of the Income Tax (Transitional Provisions) Act 1997; and

(d) for a benefit that arises under a contract that meets the standards of subregulation (9) and is purchased by the primary beneficiary on or after 20 September 1998—the commencement day under the contract is the day when the benefit was purchased; and

(e) for a benefit that arises under a contract that meets the standards of subregulation (4)—the contract also meets the standards of regulation 1.07A; and

(f) for a benefit that arises under a contract that meets the standards of subregulation (2), (6), (7) or (9)—the contract also meets the standards of regulation 1.07B; and

(g) for a benefit that arises under a contract that meets the standards of subregulation (8):

(i) the benefit can be taken to consist of two benefits:

(A) an annuity that arises from that part of the contract that provides for payments whose size is not fixed; and

(B) an annuity that arises from that part of the contract that provides for payments whose size in a year is fixed; and

(ii) the contract meets the standards of regulation 1.07A in relation to the annuity mentioned in sub‑subparagraph (i)(A); and

(iii) the contract meets the standards of regulation 1.07B in relation to the annuity mentioned in sub‑subparagraph (i)(B); and

(h) for a benefit that arises under a contract that meets the standards of subregulation (10), and has a commencement day on or after 20 September 2004—the contract also meets the standards of regulation 1.07C.

(1B) A benefit provided by a life insurance company or registered organisation that commenced to be paid on or after 20 September 2007 is taken to be an annuity for the purposes of the Act if:

(a) the benefit arises under a contract that meets the standards of:

(i) subregulation 1.05(9) or (10); and

(ii) subregulation 1.05(11A); and

(b) the benefit was purchased with a rollover superannuation benefit that resulted from the commutation of:

(i) an annuity provided under a contract that meets the standards of subregulation 1.05(2), (9) or (10); or

(ii) a pension provided under rules that meet the standards of subregulation 1.06(2), (7) or (8); or

(iii) a pension provided under terms and conditions that meet the standards of subregulation 1.07(3A) of the RSA Regulations; and

(c) for a benefit that arises under a contract that meets the standards of subregulation (9)—the contract also meets the standards of regulation 1.07B; and

(d) for a benefit that arises under a contract that meets the standards of subregulation (10)—the contract also meets the standards of regulation 1.07C.

(2) A contract for the provision of a benefit (in this subregulation called the annuity) meets the standards of this subregulation if it ensures that:

(a) the annuity is paid at least annually throughout the life of the primary beneficiary in accordance with paragraphs (b) and (c) and, if there is a reversionary beneficiary:

(i) throughout the reversionary beneficiary’s life; or

(ii) if he or she is a child of the primary beneficiary or of a former reversionary beneficiary under the annuity—at least until his or her 16th birthday; or

(iii) if the person referred to in subparagraph (ii) is a full‑time student at age 16—at least until the end of his or her full‑time studies or until his or her 25th birthday (whichever occurs sooner); and

(b) the size of payments of benefit in a year is fixed, allowing for variation only:

(i) as specified in the contract; or

(ii) to allow commutation to pay a superannuation contributions surcharge; or

(iii) to allow an amount to be paid under a payment split and reasonable fees in respect of the payment split to be charged; and

(c) unless APRA otherwise approves, the sum payable as benefit in each year to the primary beneficiary or to the reversionary beneficiary, as the case may be, is:

(i) if CPIc is not less than CPIp—not less than SPp; or

(ii) if CPIc is less than CPIp—not less than:

where:

CPIc means the quarterly CPI first published by the Australian Statistician for the second‑last quarter before the day on which payment is to be made.

CPIp means the quarterly CPI first published by the Australian Statistician for the same quarter in the immediately preceding year.

SPp means the sum payable in the immediately preceding year;

and

(d) the amount paid as the purchase price is wholly converted into annuity income; and

(e) the annuity does not have a residual capital value; and

(f) the annuity cannot be commuted except in any of the following circumstances:

(i) the annuity is not funded from the commutation of:

(A) an annuity that meets the standards of this subregulation or subregulation (3), (9) or (10); or

(B) a pension that meets the standards of subregulation 1.06(2), (3), (7) or (8); or

(C) a pension that meets the standards of subregulation 1.07(3A) of the RSA Regulations;

and the commutation is made within 6 months after the commencement day of the annuity;

(ii) the commutation is made to the benefit of a reversionary beneficiary on the death of the primary beneficiary and within one of the following periods after the commencement day of the annuity:

(A) if the primary beneficiary’s life expectancy on the commencement day, rounded up to the next whole number, is a period less than 20 years—that period;

(B) in any other case—20 years;

(iii) the superannuation lump sum resulting from the commutation is transferred directly for the purpose of purchasing another benefit provided under:

(A) a contract that meets the standards of this subregulation or subregulation (3), (9) or (10); or

(B) rules that meet the standards of subregulation 1.06(2), (3), (7) or (8); or

(C) terms and conditions that meet the standards of subregulation 1.07(3A) of the RSA Regulations;

(iv) to pay a superannuation contributions surcharge;

(v) to give effect to an entitlement of a non‑member spouse under a payment split;

(vi) for the purpose of paying an amount under Division 131 or 135 in Schedule 1 to the Taxation Administration Act 1953, or section 292‑80C of the Income Tax (Transitional Provisions) Act 1997, to give effect to a release authority in respect of the primary beneficiary;

(vii) the annuity was commenced in contravention of Part 6 and the commutation would result in an obligation to pay an amount to the Commissioner of Taxation under subsection 20F(1) of the Superannuation (Unclaimed Money and Lost Members) Act 1999; and

(g) if the annuity reverts or is commuted, it does not have a reversionary component greater than 100% of the benefit that was payable before the reversion or the commutation; and

(h) the annuity cannot be transferred to a person other than a reversionary beneficiary on the death of the primary beneficiary or of another reversionary beneficiary; and

(i) the capital value of the annuity, and the income from it, cannot be used as security for a borrowing.

(3) For the purpose of determining whether an annuity meets the standards in subregulation (2), it is immaterial that:

(a) if the primary beneficiary dies within the period used for subparagraph (2)(f)(ii), a surviving reversionary beneficiary may obtain a payment equal to the total payments that the primary beneficiary would have received, if the primary beneficiary had not died, from the day of the death until the end of the period; and

(b) if the primary beneficiary dies within the period used for subparagraph (2)(f)(ii) and there is no surviving reversionary beneficiary, an amount, not exceeding the difference between the sum of the amounts paid to the primary beneficiary and the sum of the amounts that would have been so payable in the period, is payable to the primary beneficiary’s estate; and

(c) if the primary beneficiary dies within the period used for subparagraph (2)(f)(ii) and there is a surviving reversionary beneficiary who also dies within that period, there is payable to the reversionary beneficiary’s estate an amount determined as described in paragraph (b) as if that paragraph applied to the reversionary beneficiary.

(4) A contract for the provision of a benefit (in this subregulation called the annuity):

(a) that does not meet the standards in subregulation (2); and

(b) that does not fix the size of payments of benefit in a year; and

(c) under which the commencement day is on or after 22 December 1992;

meets the standards of this subregulation if the contract at least ensures that:

(d) the standards in paragraphs (2)(h) and (i) are met; and

(e) payments are made at least annually; and

(f) for an annuity that has a commencement day on or after 22 December 1992 and before 1 January 2006—the payments in a year (excluding payments by way of commutation but including payments made under a payment split) are not larger or smaller in total than, respectively, the maximum and minimum limits calculated in accordance with Schedule 1A; and

(g) for an annuity that has a commencement day on or after 1 January 2006—the payments in a year (excluding payments by way of commutation but including payments made under a payment split) are not larger or smaller in total than the following:

(i) for payments made during the period starting on 1 January 2006 and ending on 30 June 2006—the respective maximum and minimum limits for the year calculated in accordance with 1 of the following Schedules:

(A) Schedule 1A;

(B) Schedule 1AAB;

(ii) for payments made on or after 1 July 2006—the respective maximum and minimum limits for the year calculated in accordance with Schedule 1AAB.

Note: 22 December 1992 was the date of Royal Assent to the Taxation Laws Amendment (Superannuation) Act 1992.

(5) For the purpose of determining whether an annuity meets the standards in subregulation (4), it is immaterial:

(a) that:

(i) the commencement day of the annuity occurs on or after 1 June in a financial year; and

(ii) the contract does not ensure that payments in that financial year meet the standard in that subregulation for the minimum amount; or

(b) that the contract does not ensure that the payments in the year in which the annuity is to end meet the standard in that subregulation for the minimum amount.

(6) A contract for the provision of a benefit (in this subregulation called the annuity):

(a) that does not meet the standards of subregulation (2); and

(b) that fixes the size of the payments of benefit in a year, allowing for variation only as specified in the contract or to allow payments to be made under a payment split; and

(c) under which the commencement day is on or after 1 July 1994;

meets the standards of this subregulation if the contract at least ensures that:

(d) the standards in paragraphs (2)(g), (h) and (i) are met; and

(e) except in relation to payments, by way of commutation, for superannuation contributions surcharge, variation in payments from year to year does not exceed, in any year, the average rate of increase of the CPI in the preceding 3 years; and

(f) payments in accordance with paragraph (b) are made at least annually; and

(g) the amount paid as the purchase price is wholly converted into annuity income.

(7) A contract for the provision of a benefit (in this subregulation called the annuity) that:

(a) does not meet the standards of subregulation (2); and

(b) provides for payments whose size in a year is fixed, allowing for variation only as specified in the contract; and

(c) provides for additional payments (in this subregulation called bonus payments);

(d) the commencement day of which is on or after 1 July 1994;

meets the standards of this subregulation if it at least ensures that:

(e) in respect of the fixed‑size payments—the standards in subregulation (6) are met; and

(f) the fixed‑size payments amount to at least 50% of:

(i) if the provider provides annuities of the kind specified in subregulation (6)—the amount that would be payable if the annuity were wholly of that kind; or

(ii) if the provider does not provide annuities of the kind specified in subregulation (6)—the fixed‑size payments are at least equal in amount to 50% of the interest payable on Commonwealth bonds that have the same value as the purchase price of the annuity and that most closely correspond in term to the term of the annuity; and

(g) the amounts of the bonus payments (if any) are reasonably proportional to the investment income from which the payments purport to be derived; and

(h) the amount of a bonus payment (if any) is notified in writing by the provider each year and is paid to the beneficiary in the year next following (except when deferral of the payment would not result, in any future year, in the rate of increase in size of the total payments for the year exceeding the average rate of increase of the CPI in the preceding 3 years).

(8) A contract for the provision of a benefit (in this subregulation called the annuity):

(a) that does not meet all the standards in any other provision of this regulation; and

(b) under which the commencement day is on or after 22 December 1992; and

(c) that provides for:

(i) payments whose size in a year is fixed, allowing for variation only as specified in the contract; and

(ii) additional payments whose size is not fixed, derived from the application of part of the purchase price to investments by allocation of the annuity provider;

meets the standards of this subregulation if it at least ensures that:

(d) in respect of fixed‑size payments—if the commencement day is on or after 1 July 1994, the standards in subregulation (6) are met; and

(e) in respect of payments whose size is not fixed—the standards in subregulation (4) are met.

Note: 22 December 1992 was the date of Royal Assent to the Taxation Laws Amendment (Superannuation) Act 1992.

(9) A contract for the provision of a benefit (in this subregulation called the annuity) meets the standards of this subregulation if the contract ensures that:

(a) for an annuity that has a commencement day before 20 September 2004:

(i) if the life expectancy of the primary beneficiary on the commencement day is less than 15 years—the annuity is paid at least annually to the primary beneficiary or to a reversionary beneficiary throughout a period equal to the primary beneficiary’s life expectancy on the commencement day, rounded up, at the primary beneficiary’s option, to the next whole number if the primary beneficiary’s life expectancy does not consist of a whole number of years; or

(ii) if the life expectancy of the primary beneficiary on the commencement day is 15 years or more—the annuity is paid at least annually to the primary beneficiary or to a reversionary beneficiary throughout a period that is not less than 15 years but not more than the primary beneficiary’s life expectancy on the commencement day, rounded up, at the primary beneficiary’s option, to the next whole number if the primary beneficiary’s life expectancy does not consist of a whole number of years; and

(b) for an annuity that has a commencement day on or after 20 September 2004:

(i) the annuity is paid at least annually to the primary beneficiary or to a reversionary beneficiary throughout a period equal to the primary beneficiary’s life expectancy on the commencement day, rounded up to the next whole number if the primary beneficiary’s life expectancy does not consist of a whole number of years; or

(ii) the annuity is paid at least annually to the primary beneficiary or to a reversionary beneficiary throughout a period equal to the primary beneficiary’s life expectancy mentioned in subparagraph (i) calculated, at the option of the primary beneficiary, as if the primary beneficiary were up to 5 years younger on the commencement day; or

(iia) if the annuity has a commencement day on or after 1 January 2006—the annuity is paid at least annually to the primary beneficiary or reversionary beneficiary throughout a period that is not less than the period available under subparagraph 1.05(9)(b)(i), and not more than the greater of the following periods:

(A) the maximum period available under subparagraph 1.05(9)(b)(ii);

(B) the period of years equal to the number that is the difference between the age attained by the primary beneficiary at his or her most recent birthday before the commencement day, and 100; or

(iii) if:

(A) the annuity is an annuity that reverts to a surviving spouse on the death of the primary beneficiary; and

(B) the life expectancy of the primary beneficiary’s spouse is greater than the life expectancy of the primary beneficiary; and

(C) the primary beneficiary has not chosen to make an arrangement mentioned in subparagraph (i), (ii) or (iia) for the annuity;

the annuity is paid at least annually to the primary beneficiary or to a reversionary beneficiary throughout a period equal to:

(D) the life expectancy of the spouse on the commencement day; or

(E) the life expectancy of the spouse calculated, at the option of the primary beneficiary, as if the spouse were up to 5 years younger on the commencement day; or

(F) if the annuity has a commencement day on or after 1 January 2006—a period that is not less than the period available under sub‑subparagraph 1.05(9)(b)(iii)(D), and not more than the greater of the following periods:

(I) the maximum period available under sub‑subparagraph 1.05(9)(b)(iii)(E);

(II) the period of years equal to the number that is the difference between the age attained by the spouse at his or her most recent birthday before the commencement day, and 100;

at the option of the primary beneficiary, and rounded up to the next whole number if the life expectancy of the spouse, or the period, does not consist of a whole number of years; and

(c) the total amount of the payment, or payments, to be made in the first year after the commencement day (not taking commuted amounts into account) is fixed and that payment, or the first of those payments, relates to the period commencing on the day the benefit was purchased; and

(d) the total amount of the payments to be made in a year other than the first year after the commencement day (not taking commuted amounts into account) does not fall below the total amount of the payments made in the immediately preceding year (the previous total), and does not exceed the previous total:

(i) if CPIc is less than or equal to 4%—by more than 5% of the previous total; or

(ii) if CPIc is more than 4%—by more than CPIc + 1%;

where:

CPIc is the change (if any), expressed as a percentage, determined by comparing the quarterly CPI first published by the Australian Statistician for the second‑last quarter before the day on which the first of those payments is to be made and the quarterly CPI first published by the Australian Statistician for the same quarter in the immediately preceding year;

and

(e) the total amount of the payments to be made in a year in accordance with paragraph (c) or (d) may be varied only:

(i) to allow commutation to pay a superannuation contributions surcharge; or

(ii) to allow an amount to be paid under a payment split and reasonable fees to be charged in respect of the payment split; and

(f) the amount paid as the purchase price is wholly converted into annuity income; and

(g) the annuity does not have a residual capital value; and

(h) the annuity cannot be commuted except in any of the following circumstances:

(i) the annuity is not funded from the commutation of:

(A) an annuity that meets the standards of this subregulation or subregulation (2), (3) or (10); or

(B) a pension that meets the standards of subregulation 1.06(2), (3), (7) or (8); or

(C) a pension that meets the standards of subregulation 1.07(3A) of the RSA Regulations;

and the commutation is made within 6 months after the commencement day of the annuity;

(ii) subject to subparagraph (iv), by payment, on the death of the primary beneficiary, to the benefit of a reversionary beneficiary or, if there is no reversionary beneficiary, to the estate of the primary beneficiary;

(iii) subject to subparagraph (iv), by payment, on the death of a reversionary beneficiary, to the benefit of another reversionary beneficiary or, if there is no other reversionary beneficiary, to the estate of the reversionary beneficiary;

(iv) for subparagraphs (ii) and (iii), if the primary beneficiary has opted, under subparagraph (b)(iii), for a period worked out in relation to the life expectancy or age of the primary beneficiary’s spouse—the annuity cannot be commuted until the death of both the primary beneficiary and the spouse;

(v) the superannuation lump sum resulting from the commutation is transferred directly to the purchase of another benefit that is:

(A) an annuity provided under a contract that meets the standards of subregulation (2), (3) or (10) or this subregulation; or

(B) a pension that is provided under rules that meet the standards of subregulation 1.06(2), (3), (7) or (8); or

(C) a pension that is provided under terms and conditions that meet the standards of subregulation 1.07(3A) of the RSA Regulations;

(vi) to pay a superannuation contributions surcharge;

(vii) to give effect to an entitlement of a non‑member spouse under a payment split;

(viii) for the purpose of paying an amount under Division 131 or 135 in Schedule 1 to the Taxation Administration Act 1953, or section 292‑80C of the Income Tax (Transitional Provisions) Act 1997, to give effect to a release authority in respect of the primary beneficiary;

(ix) the annuity was commenced in contravention of Part 6 and the commutation would result in an obligation to pay an amount to the Commissioner of Taxation under subsection 20F(1) of the Superannuation (Unclaimed Money and Lost Members) Act 1999; and

(i) if the annuity reverts, it does not have a reversionary component greater than 100% of the benefit that was payable before the reversion; and

(j) if the annuity is commuted, the commuted amount cannot exceed the benefit that was payable immediately before the commutation; and

(k) the annuity cannot be transferred to a person except:

(i) on the death of the primary beneficiary, to a reversionary beneficiary or, if there is no reversionary beneficiary, to the estate of the primary beneficiary; or

(ii) on the death of a reversionary beneficiary, to another reversionary beneficiary or, if there is no other reversionary beneficiary, to the estate of the reversionary beneficiary; and

(l) the capital value of the annuity, and the income from it, cannot be used as security for a borrowing.

(10) A contract for the provision of a benefit (market linked annuity) meets the standards of this subregulation if the contract ensures that:

(a) the market linked annuity:

(i) is paid at least annually to the primary beneficiary or to a reversionary beneficiary throughout a period equal to the primary beneficiary’s life expectancy on the commencement day of the annuity, rounded up to the next whole number if the primary beneficiary’s life expectancy does not consist of a whole number of years; or

(ii) is paid at least annually to the primary beneficiary or to a reversionary beneficiary throughout a period equal to the primary beneficiary’s life expectancy mentioned in subparagraph (i) calculated, at the option of the primary beneficiary, as if the primary beneficiary were up to 5 years younger on the commencement day; or

(iia) if the annuity has a commencement day on or after 1 January 2006—the annuity is paid at least annually to the primary beneficiary or reversionary beneficiary throughout a period that is not less than the period available under subparagraph 1.05(10)(a)(i), and not more than the greater of the following periods:

(A) the maximum period available under subparagraph 1.05(10)(a)(ii);

(B) the period of years equal to the number that is the difference between the age attained by the primary beneficiary at his or her most recent birthday before the commencement day, and 100; or

(iii) if:

(A) the annuity is an annuity that reverts to a surviving spouse on the death of the primary beneficiary; and

(B) the life expectancy of the primary beneficiary’s spouse is greater than the life expectancy of the primary beneficiary; and

(C) the primary beneficiary has not chosen to make an arrangement mentioned in subparagraph (i), (ii) or (iia) for the annuity;

the annuity is paid at least annually to the primary beneficiary or to a reversionary beneficiary throughout a period equal to:

(D) the life expectancy of the spouse on the commencement day; or

(E) the life expectancy of the spouse calculated, at the option of the primary beneficiary, as if the spouse were up to 5 years younger on the commencement day; or

(F) if the annuity has a commencement day on or after 1 January 2006—a period that is not less than the period available under sub‑subparagraph 1.05(10)(a)(iii)(D), and not more than the greater of the following periods:

(A) the maximum period available under sub‑subparagraph 1.05(10)(a)(iii)(E);

(B) the period of years equal to the number that is the difference between the age attained by the spouse at his or her most recent birthday before the commencement day, and 100;

at the option of the primary beneficiary, and rounded up to the next whole number if the life expectancy of the spouse, or the period, does not consist of a whole number of years; and

(b) the total amount of the payments to be made in a year (excluding payments by way of commutation but including payments made under a payment split) is determined in accordance with Schedule 6; and

(c) the market linked annuity does not have a residual capital value; and

(d) the market linked annuity cannot be commuted except in any of the following circumstances:

(i) the annuity is not funded from the commutation of:

(A) another annuity that is provided under a contract that meets the standards of subregulation (2), (3) or (9) or this subregulation; or

(B) a pension that is provided under rules that meet the standards of subregulation 1.06(2), (3), (7) or (8); or

(C) a pension that is provided under terms and conditions that meet the standards of subregulation 1.07(3A) of the RSA Regulations;

and the commutation is made within 6 months after the commencement day of the annuity;

(ii) subject to subparagraph (iii), on the death of the primary beneficiary or reversionary beneficiary, by payment of:

(A) a lump sum or a new annuity to one or more dependants of either the primary beneficiary or reversionary beneficiary; or

(B) a lump sum to the legal personal representative of either the primary beneficiary or reversionary beneficiary; or

(C) if, after making reasonable enquiries, the provider of the annuity is unable to find a person mentioned in sub‑subparagraph (A) or (B)—a lump sum to another individual;

(iii) for subparagraph (ii), if the primary beneficiary has opted, under subparagraph (a)(iii), for a period worked out in relation to the life expectancy or age of the primary beneficiary’s spouse—the market linked annuity cannot be commuted until the death of both the primary beneficiary and the spouse;

(iv) the superannuation lump sum resulting from the commutation is transferred directly to the purchase of another benefit that is:

(A) an annuity provided under a contract that meets the standards of subregulation 1.05(2), (3) or (9) or this subregulation; or

(B) a pension that is provided under rules that meet the standards of subregulation 1.06(2), (3), (7) or (8); or

(C) a pension that is provided under terms and conditions that meet the standards of subregulation 1.07(3A) of the RSA Regulations;

(v) to pay a superannuation contributions surcharge;

(vi) to give effect to an entitlement of a non‑member spouse under a payment split;

(vii) for the purpose of paying an amount under Division 131 or 135 in Schedule 1 to the Taxation Administration Act 1953, or section 292‑80C of the Income Tax (Transitional Provisions) Act 1997, to give effect to a release authority in respect of the primary beneficiary;

(viii) the annuity was commenced in contravention of Part 6 and the commutation would result in an obligation to pay an amount to the Commissioner of Taxation under subsection 20F(1) of the Superannuation (Unclaimed Money and Lost Members) Act 1999; and

(e) if the market linked annuity reverts, it does not have a reversionary component greater than 100% of the account balance immediately before the reversion; and

(f) if the market linked annuity is commuted, the commutation amount cannot exceed the account balance immediately before the commutation; and

(g) the market linked annuity can be transferred only:

(i) on the death of the primary beneficiary:

(A) to 1 of the dependants of the primary beneficiary; or

(B) to the legal personal representative of the primary beneficiary; or

(ii) on the death of the reversionary beneficiary:

(A) to 1 of the dependants of the reversionary beneficiary; or

(B) to the legal personal representative of the reversionary beneficiary; and

(h) the capital value of the market linked annuity, and the income from it, cannot be used as security for a borrowing.

(11) A contract mentioned in subregulation (10) is not prevented from meeting the standards of that subregulation by reason only that the contract provides that, if the commencement day of the annuity is on or after 1 June in a financial year, no payment is required to be made for that financial year.

(11A) A contract for the provision of a benefit (the annuity) meets the standards of this subregulation if the contract ensures that payment of the annuity is made at least annually, and also ensures that:

(a) for an annuity in relation to which there is an account balance attributable to the annuitant—the total of payments in any year (excluding payments by way of commutation but including payments under a payment split) is at least the amount calculated under clause 1 of Schedule 7; and

(b) for an annuity that is not described in paragraph (a):

(i) both of the following apply:

(A) the contract does not provide for a residual capital value, commutation value or withdrawal benefit greater than 100% of the purchase price of the annuity;

(B) the total of payments in any year (excluding payments by way of commutation but including payments under a payment split) is at least the amount calculated under clause 2 of Schedule 7; or

(ii) each of the following applies:

(A) the annuity is payable throughout the life of the beneficiary (primary or reversionary), or for a fixed term of years that is no greater than the difference between the primary beneficiary’s age on the commencement day and age 100;

(B) the amount paid as the purchase price is wholly converted into annuity payments;

(C) there is no arrangement for an amount (or a percentage of the purchase price) prescribed by the contract to be returned to the recipient when the annuity ends;

(D) the total of payments from the annuity in the first year (excluding payments by way of commutation but including payments under a payment split) is at least the amount calculated under clause 2 of Schedule 7;

(E) the total of payments from the annuity in a subsequent year cannot vary from the total of payments in the previous year unless the variation is as a result of an indexation arrangement or the transfer of the annuity to another person;

(F) if the annuity is commuted, the commutation amount cannot exceed the benefit that was payable immediately before the commutation; or

(iii) the standards of subregulation (2) are met; and

(c) the annuity is transferable to another person only on the death of the beneficiary (primary or reversionary, as the case may be); and

(d) the capital value of the annuity and the income from it cannot be used as a security for a borrowing.

(11B) A contract for the provision of a benefit does not meet the standards of any of subregulations (2) to (11A) if, in relation to the death of the annuity recipient on or after 1 July 2007, the annuity is transferred or paid to a person who would not be eligible to be paid a benefit in the form of an annuity under paragraph 6.21(2)(b) or subregulation 6.21(2A) or (2B).

(12) Despite section 7 of the Income Tax Assessment (1936 Act) Regulation 2015, for an annuity that has a commencement day on or after 20 September 2004 and on or before 31 December 2004, one of the following life tables are to be used in ascertaining the life expectancy of a person under this regulation:

(a) the most recently published Australian Life Tables;

(b) the 1995‑97 Australian Life Tables.

(13) In this regulation:

indexation arrangement, in relation to an annuity, means an arrangement specified in the contract for the provision of the annuity that:

(a) results in the total amount of annuity payments in each year:

(i) increasing by the same percentage factor; or

(ii) being adjusted in line with movements in the Consumer Price Index; or

(iii) being adjusted in line with movements in an index of average weekly earnings published by the Australian Statistician; or

(iv) being adjusted in accordance with subparagraph (ii) or (iii) but with an increase capped at a maximum level; and