Treasury Laws Amendment (A Tax Plan for the COVID‑19 Economic Recovery) Act 2020

No. 92, 2020

An Act to amend the law in relation to taxation, and for related purposes

Treasury Laws Amendment (A Tax Plan for the COVID‑19 Economic Recovery) Act 2020

No. 92, 2020

An Act to amend the law in relation to taxation, and for related purposes

Contents

2 Commencement

3 Schedules

Schedule 1—Accelerating the Personal Income Tax Plan

Part 1—Personal income tax reform: main amendments

Income Tax Rates Act 1986

Part 2—Personal income tax reform: repeals on 1 July 2024

Income Tax Rates Act 1986

Part 3—Low Income tax offset

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Part 4—Low and Middle Income tax offset

Income Tax Assessment Act 1997

Part 5—Amendments to amending legislation

Treasury Laws Amendment (Personal Income Tax Plan) Act 2018

Schedule 2—Temporary loss carry back

Part 1—Main amendments

Income Tax Assessment Act 1997

Part 2—Anti‑avoidance

Income Tax Assessment Act 1936

Part 3—Consequential amendments

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Schedule 3—Increasing small business entity turnover threshold for certain concessions

Part 1—Amendments

A New Tax System (Goods and Services Tax) Act 1999

Customs Act 1901

Excise Act 1901

Fringe Benefits Tax Assessment Act 1986

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Part 2—Application of amendments

Schedule 4—Enhancing the R&D Tax Incentive

Income Tax Assessment Act 1997

Tax Laws Amendment (Research and Development) Act 2015

Schedule 5—Enhancing the integrity of the R&D Tax Incentive

Part 1—Schemes to reduce income tax

Income Tax Assessment Act 1936

Part 2—R&D clawback and catch up amounts

Income Tax Assessment Act 1997

Income Tax Rates Act 1986

Income Tax (Transitional Provisions) Act 1997

Part 3—Application of amendments

Schedule 6—Improving the administration of the R&D Tax Incentive

Part 1—Reporting of information about research and development tax offset

Taxation Administration Act 1953

Part 2—Determinations about performance of Board’s functions

Industry Research and Development Act 1986

Part 3—Delegation by Board and committees

Industry Research and Development Act 1986

Part 4—Extensions of time

Industry Research and Development Decision‑making Principles 2011

Schedule 7—Temporary full expensing of depreciating assets

Part 1—Temporary full expensing of depreciating assets

Income Tax (Transitional Provisions) Act 1997

Part 2—Adjusting existing measures

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Part 3—Consequential amendments

Income Tax Assessment Act 1997

Income Tax (Transitional Provisions) Act 1997

Treasury Laws Amendment (A Tax Plan for the COVID-19 Economic Recovery) Act 2020

No. 92, 2020

An Act to amend the law in relation to taxation, and for related purposes

[Assented to 14 October 2020]

The Parliament of Australia enacts:

This Act is the Treasury Laws Amendment (A Tax Plan for the COVID‑19 Economic Recovery) Act 2020.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provisions | Commencement | Date/Details |

1. Sections 1 to 3 and anything in this Act not elsewhere covered by this table | The day this Act receives the Royal Assent. | 14 October 2020 |

2. Schedule 1, Part 1 | The day after this Act receives the Royal Assent. | 15 October 2020 |

3. Schedule 1, Part 2 | 1 July 2024. | 1 July 2024 |

4. Schedule 1, Part 3 | The day after this Act receives the Royal Assent. | 15 October 2020 |

5. Schedule 1, Part 4 | 1 July 2021. | 1 July 2021 |

6. Schedule 1, Part 5 | The day after this Act receives the Royal Assent. | 15 October 2020 |

7. Schedules 2 to 7 | The first 1 January, 1 April, 1 July or 1 October to occur after the day this Act receives the Royal Assent. | 1 January 2021 |

Note: This table relates only to the provisions of this Act as originally enacted. It will not be amended to deal with any later amendments of this Act.

(2) Any information in column 3 of the table is not part of this Act. Information may be inserted in this column, or information in it may be edited, in any published version of this Act.

Legislation that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Note: The provisions of the Industry Research and Development Decision‑making Principles 2011 amended or inserted by this Act, and any other provisions of that instrument, may be amended or repealed by an instrument made under section 32A of the Industry Research and Development Act 1986 (see subsection 13(5) of the Legislation Act 2003).

Schedule 1—Accelerating the Personal Income Tax Plan

Part 1—Personal income tax reform: main amendments

1 Clause 1 of Part I of Schedule 7 (table dealing with tax rates for resident taxpayers for the 2018‑19, 2019‑20, 2020‑21 or 2021‑22 year of income)

Repeal the table (including the note).

2 Repealed law continues for relevant years of income

Despite the repeal by item 1 of the table mentioned in that item, that table continues to apply, in relation to assessments for the 2018‑19 or 2019‑20 year of income, as if that repeal had not happened.

3 Clause 1 of Part I of Schedule 7 (heading to table dealing with tax rates for resident taxpayers for the 2022‑23 or 2023‑24 year of income)

Omit “Tax rates for resident taxpayers for the 2022‑23 or 2023‑24 year of income”, substitute “Tax rates for resident taxpayers for the 2020‑21, 2021‑22, 2022‑23 or 2023‑24 year of income”.

4 Clause 1 of Part I of Schedule 7 (table dealing with tax rates for resident taxpayers for the 2022‑23 or 2023‑24 year of income) (note)

Repeal the note, substitute:

Note: The above table will be repealed on 1 July 2024 by the Treasury Laws Amendment (A Tax Plan for the COVID‑19 Economic Recovery) Act 2020.

5 Clause 1 of Part II of Schedule 7 (table dealing with tax rates for non‑resident taxpayers for the 2018‑19, 2019‑20, 2020‑21 or 2021‑22 year of income)

Repeal the table (including the note).

6 Repealed law continues for relevant years of income

Despite the repeal by item 5 of the table mentioned in that item, that table continues to apply, in relation to assessments for the 2018‑19 or 2019‑20 year of income, as if that repeal had not happened.

7 Clause 1 of Part II of Schedule 7 (heading to table dealing with tax rates for non‑resident taxpayers for the 2022‑23 or 2023‑24 year of income)

Omit “Tax rates for non‑resident taxpayers for the 2022‑23 or 2023‑24 year of income”, substitute “Tax rates for non‑resident taxpayers for the 2020‑21, 2021‑22, 2022‑23 or 2023‑24 year of income”.

8 Clause 1 of Part II of Schedule 7 (table dealing with tax rates for non‑resident taxpayers for the 2022‑23 or 2023‑24 year of income) (note)

Repeal the note, substitute:

Note: The above table will be repealed on 1 July 2024 by the Treasury Laws Amendment (A Tax Plan for the COVID‑19 Economic Recovery) Act 2020.

9 Clause 1 of Part III of Schedule 7 (table dealing with tax rates for working holiday makers for the 2018‑19, 2019‑20, 2020‑21 or 2021‑22 year of income)

Repeal the table (including the note).

10 Repealed law continues for relevant years of income

Despite the repeal by item 9 of the table mentioned in that item, that table continues to apply, in relation to assessments for the 2018‑19 or 2019‑20 year of income, as if that repeal had not happened.

11 Clause 1 of Part III of Schedule 7 (heading to table dealing with tax rates for working holiday makers for the 2022‑23 or 2023‑24 year of income)

Omit “Tax rates for working holiday makers for the 2022‑23 or 2023‑24 year of income”, substitute “Tax rates for working holiday makers for the 2020‑21, 2021‑22, 2022‑23 or 2023‑24 year of income”.

12 Clause 1 of Part III of Schedule 7 (table dealing with tax rates for working holiday makers for the 2022‑23 or 2023‑24 year of income) (note)

Repeal the note, substitute:

Note: The above table will be repealed on 1 July 2024 by the Treasury Laws Amendment (A Tax Plan for the COVID‑19 Economic Recovery) Act 2020.

Part 2—Personal income tax reform: repeals on 1 July 2024

13 Clause 1 of Part I of Schedule 7 (table dealing with tax rates for resident taxpayers for the 2020‑21, 2021‑22, 2022‑23 or 2023‑24 year of income)

Repeal the table (including the note).

14 Clause 1 of Part II of Schedule 7 (table dealing with tax rates for non‑resident taxpayers for the 2020‑21, 2021‑22, 2022‑23 or 2023‑24 year of income)

Repeal the table (including the note).

15 Clause 1 of Part III of Schedule 7 (table dealing with tax rates for working holiday makers for the 2020‑21, 2021‑22, 2022‑23 or 2023‑24 year of income)

Repeal the table (including the note).

16 Repealed law continues for relevant years of income

Despite the repeal of a table by this Part, that table continues to apply, in relation to assessments for a year of income mentioned in the table’s heading, as if that repeal had not happened.

Income Tax Assessment Act 1936

17 Section 159N

Repeal the section.

Income Tax Assessment Act 1997

18 Section 13‑1 (table item headed “low income earner”)

Omit:

tax offset for 2021‑22 income year and earlier income years |

|

19 Subsections 61‑110(1) and (2)

Omit “the 2022‑23 income year or a later income year”, substitute “the 2020‑21 income year or a later income year”.

20 Subsection 63‑10(1) (table item 17)

Repeal the item.

21 Subsection 63‑10(1) (notes 6 and 7)

Repeal the notes.

Taxation Administration Act 1953

22 Section 45‑340 in Schedule 1 (method statement, step 1, paragraph (f))

Repeal the paragraph.

23 Section 45‑375 in Schedule 1 (method statement, step 1, paragraph (e))

Repeal the paragraph.

24 Application of amendments

The amendments made by this Part apply in relation to assessments for the 2020‑21 income year or a later income year.

Part 4—Low and Middle Income tax offset

Income Tax Assessment Act 1997

25 Subdivision 61‑D (heading)

Repeal the heading, substitute:

Subdivision 61‑D—Low Income tax offset

26 Sections 61‑105 and 61‑107

Repeal the sections.

27 Application of amendments

The amendments made by this Part apply in relation to assessments for the 2021‑22 income year or a later income year.

Part 5—Amendments to amending legislation

Treasury Laws Amendment (Personal Income Tax Plan) Act 2018

28 Subsection 2(1) (table item 3)

Repeal the item.

29 Subsection 2(1) (table items 5 and 6)

Repeal the items.

30 Part 3 of Schedule 1

Repeal the Part.

31 Part 3 of Schedule 2

Repeal the Part.

Schedule 2—Temporary loss carry back

Income Tax Assessment Act 1997

1 Section 67‑23 (after table item 13)

Insert:

14 | corporate losses | *loss carry back tax offset under Division 160 |

2 Before Division 164

Insert:

Table of Subdivisions

Guide to Division 160

160‑A Entitlement to and amount of loss carry back tax offset

160‑1 What this Division is about

A corporate tax entity can choose to “carry back” a tax loss it had for 2019‑20, 2020‑21 or 2021‑22 against the income tax liability it had for 2018‑19, 2019‑20 or 2020‑21.

The entity gets a refundable tax offset for 2020‑21 or 2021‑22 that is a proxy for the tax the entity would save if it deducted the loss in the income year to which the loss is “carried back”.

The refundable tax offset:

(a) is capped at the entity’s franking account balance; and

(b) is only available for losses for years for which the entity’s turnover was less than $5 billion.

Subdivision 160‑A—Entitlement to and amount of loss carry back tax offset

Table of sections

160‑5 Entitlement to loss carry back tax offset

160‑10 Amount of loss carry back tax offset

160‑5 Entitlement to loss carry back tax offset

An entity is entitled to a *tax offset (the loss carry back tax offset) for the *current year if the following conditions are satisfied:

(a) the current year is:

(i) the 2020‑21 income year; or

(ii) the 2021‑22 income year;

(b) the entity is a *corporate tax entity throughout the current year;

Note: See also section 160‑25.

(c) any or all of the following income years were *loss years:

(i) the 2019‑20 income year;

(ii) the 2020‑21 income year;

(iii) if the current year is the 2021‑22 income year—the 2021‑22 income year;

(d) the entity had an *income tax liability for any or all of the following income years:

(i) the 2018‑19 income year;

(ii) the 2019‑20 income year;

(iii) if the current year is the 2021‑22 income year and the 2021‑22 income year was a loss year—the 2020‑21 income year;

(e) any of the following requirements are satisfied for the current year and each of the 5 income years before the current year:

(i) the entity has lodged its *income tax return for the year;

(ii) the entity was not required to lodge an income tax return for the year;

(iii) the Commissioner has made an assessment of the entity’s income tax for the year;

(f) the entity makes a *loss carry back choice for the current year in accordance with Subdivision 160‑B.

Note 1: The entity can be entitled to only one loss carry back tax offset for 2020‑21. However, that offset has 2 components: one relating to 2018‑19 and one relating to 2019‑20: see section 160‑10.

Note 2: The entity can be entitled to only one loss carry back tax offset for 2021‑22. However, that offset has 3 components: one relating to 2018‑19, one relating to 2019‑20 and one relating to 2020‑21: see section 160‑10.

Note 3: The loss carry back tax offset is a refundable tax offset: see section 67‑23.

160‑10 Amount of loss carry back tax offset

(1) The amount of the entity’s *loss carry back tax offset for the *current year is the lesser of the following amounts:

(a) the sum of the *loss carry back tax offset components for:

(i) the 2018‑19 income year; and

(ii) the 2019‑20 income year; and

(iii) if the current year is the 2021‑22 income year—the 2020‑21 income year;

(b) the entity’s *franking account balance at the end of the current year.

Meaning of loss carry back tax offset component

(2) For the purposes of working out the amount of the entity’s *loss carry back tax offset for the *current year, the entity’s loss carry back tax offset component for an income year is:

(a) if the entity does not, in its *loss carry back choice for the current year, *carry back any *tax losses to the income year—nil; or

(b) otherwise—so much of the entity’s *income tax liability for the income year as does not exceed:

(i) if, in its loss carry back choice for the current year, the entity carries back only one tax loss to the income year—the amount worked out at step 3 of the following method statement in relation to the tax loss; or

(ii) if, in its loss carry back choice for the current year, the entity carries back tax losses for 2 or 3 *loss years to the income year—the sum of the amounts worked out at step 3 of the following method statement in relation to each of those tax losses.

Method statement

Step 1. Start with the amount of the *tax loss the entity *carries back to the income year.

Step 2. Reduce the step 1 amount by the entity’s *net exempt income for the income year.

Note: Do not reduce the step 1 amount by the entity’s net exempt income to the extent the net exempt income has already been utilised: see section 960‑20.

Step 3. Multiply the step 2 amount by the *corporate tax rate for the *loss year.

Example: Company A (which is not a base rate entity) has at the end of the 2020‑21 income year:

(a) a tax loss of $900,000 for that year and a franking account balance of $280,000; and

(b) for the 2018‑19 income year—an income tax liability of $120,000 and net exempt income of $5,000; and

(c) for the 2019‑20 income year—an income tax liability of $210,000.

Company A chooses to carry back $405,000 of its tax loss for the 2020‑21 year to the 2018‑19 year and $495,000 of that loss to the 2019‑20 year.

Company A’s loss carry back tax offset for the 2020‑21 year is $268,500, worked out as follows:

(a) an offset component for the 2018‑19 income year of $120,000, calculated by starting with the $405,000 carried back, reducing that at step 2 by $5,000, and multiplying the result by 30%;

(b) an offset component for the 2019‑20 income year of $148,500, calculated by starting with the $495,000 carried back and multiplying the result by 30%.

The sum of the 2 components is $268,500 (which is less than Company A’s $280,000 franking account balance at the end of the 2020‑21 year). If that sum had exceeded that balance, the amount of the offset would have been limited under paragraph (1)(b) of this section to that balance.

Income tax liability for the 2018‑19 or 2019‑20 income year already utilised

(3) Subsection (4) applies in relation to applying paragraph (2)(b) to work out the entity’s *loss carry back tax offset component for the 2018‑19 or 2019‑20 income year (the gain year) as part of working out the entity’s entitlement to a *loss carry back tax offset for the 2021‑22 income year.

(4) Disregard so much of the entity’s *income tax liability for the gain year as has previously been included (as part of working out the entity’s entitlement to a *loss carry back tax offset for the 2020‑21 income year) in a *loss carry back tax offset component.

Foreign residents

(5) Paragraph (1)(b) does not apply if the entity was a foreign resident (other than an *NZ franking company) for:

(a) if the entity *carries back an amount to the 2018‑19 income year—more than half of the 2018‑19 income year; and

(b) if the entity carries back an amount to the 2019‑20 income year—more than half of the 2019‑20 income year; and

(c) if the *current year is the 2021‑22 income year and the entity carries back an amount to the 2020‑21 income year—more than half of the 2020‑21 income year.

Subdivision 160‑B—Loss carry back choice

Table of sections

160‑15 Loss carry back choice

160‑20 Entity must have had turnover less than $5 billion for loss year

160‑25 Entity must have been a corporate tax entity during relevant years

160‑30 Transferred tax losses, income tax liabilities etc. not included

160‑35 Integrity rule—no loss carry back tax offset if scheme entered into

(1) If the *current year is the 2020‑21 or 2021‑22 income year, the entity may make a loss carry back choice for the current year that specifies the following:

(a) if the current year is the 2021‑22 income year:

(i) how much of the entity’s *tax loss (if any) for the 2021‑22 income year is to be *carried back to the 2020‑21 income year; and

(ii) how much of the entity’s tax loss (if any) for the 2021‑22 income year is to be carried back to the 2019‑20 income year; and

(iii) how much of the entity’s tax loss (if any) for the 2021‑22 income year is to be carried back to the 2018‑19 income year;

(b) in any case:

(i) how much of the entity’s tax loss (if any) for the 2020‑21 income year is to be carried back to the 2019‑20 income year; and

(i) how much of the entity’s tax loss (if any) for the 2020‑21 income year is to be carried back to the 2018‑19 income year;

(c) in any case—how much of the entity’s tax loss (if any) for the 2019‑20 income year is to be carried back to the 2018‑19 income year.

(2) The choice under subsection (1) must be made in the *approved form by:

(a) the day the entity lodges its *income tax return for the *current year; or

(b) such later day as the Commissioner allows.

160‑20 Entity must have had turnover less than $5 billion for loss year

The entity cannot *carry back an amount of a *tax loss for an income year unless the entity:

(a) was a *small business entity for the income year; or

(b) would have been a small business entity for the income year if:

(i) each reference in Subdivision 328‑C (about what is a small business entity) to $10 million were instead a reference to $5 billion; and

(ii) the reference in paragraph 328‑110(5)(b) to a small business entity were instead a reference to an entity covered by this section.

160‑25 Entity must have been a corporate tax entity during relevant years

(1) If the *current year is the 2020‑21 income year:

(a) the entity cannot *carry back an amount of a *tax loss to the 2018‑19 income year unless the entity was a *corporate tax entity throughout:

(i) the 2018‑19 income year (disregarding any period when the entity was not in existence); and

(ii) the 2019‑20 income year; and

(b) the entity cannot carry back an amount of a tax loss to the 2019‑20 income year unless the entity was a corporate tax entity throughout the 2019‑20 income year (disregarding any period when the entity was not in existence).

Note: The entity must be a corporate tax entity throughout 2020‑21: see paragraph 160‑5(b).

(2) If the *current year is the 2021‑22 income year:

(a) the entity cannot *carry back an amount of a *tax loss to the 2018‑19 income year unless the entity was a *corporate tax entity throughout:

(i) the 2018‑19 income year (disregarding any period when the entity was not in existence); and

(ii) the 2019‑20 income year; and

(iii) the 2020‑21 income year; and

(b) the entity cannot carry back an amount of a tax loss to the 2019‑20 income year unless the entity was a corporate tax entity throughout:

(i) the 2019‑20 income year (disregarding any period when the entity was not in existence); and

(ii) the 2020‑21 income year; and

(c) the entity cannot carry back an amount of a tax loss to the 2020‑21 income year unless the entity was a corporate tax entity throughout the 2020‑21 income year (disregarding any period when the entity was not in existence).

Note: The entity must be a corporate tax entity throughout 2021‑22: see paragraph 160‑5(b).

160‑30 Transferred tax losses, income tax liabilities etc. not included

(1) The entity cannot *carry back an amount of a *tax loss for an income year, to the extent that the loss:

(a) was transferred to or from the entity under Division 170 or Subdivision 707‑A (about certain company groups); or

(b) exceeds the amount that would be the entity’s tax loss for the year if section 36‑55 (about excess franking offsets) were disregarded.

(2) For the purposes of this Division, disregard the *income tax liability of the entity for an income year to the extent that it consists of an income tax liability of a *subsidiary member of a *consolidated group or *MEC group that is taken to be an income tax liability of the entity because of section 701‑5 (the entry history rule).

160‑35 Integrity rule—no loss carry back tax offset if scheme entered into

No loss carry back tax offset if scheme entered into

(1) The *corporate tax entity cannot *carry back an amount of a *tax loss to an income year (the gain year) if:

(a) there is a *scheme for a disposition of *membership interests, or an *interest in membership interests, in:

(i) the corporate tax entity; or

(ii) an entity that has a direct or indirect interest in the corporate tax entity; and

(b) the scheme is entered into or carried out during the period:

(i) starting at the start of the gain year; and

(ii) ending at the end of the *current year; and

(c) the disposition results in a change in who controls, or is able to control, (whether directly, or indirectly through one or more interposed entities) the voting power in the corporate tax entity; and

(d) another entity receives, in connection with the scheme, a *financial benefit calculated by reference to one or more *loss carry back tax offsets to which it was reasonable, at the time the scheme was entered into or carried out, to expect the corporate tax entity would be entitled; and

(e) having regard to the relevant circumstances of the scheme, it would be concluded that a person, or one of the persons, who entered into or carried out the scheme or any part of the scheme did so for a purpose (whether or not the dominant purpose but not including an incidental purpose) of enabling the corporate tax entity to get a loss carry back tax offset.

Relevant circumstances

(2) For the purposes of paragraph (1)(e), the relevant circumstances of the *scheme for a disposition include the following:

(a) the extent to which the *corporate tax entity continued to conduct the same activities after the scheme as it did before the scheme;

(b) if the corporate tax entity continued to use the same assets after the scheme as it did before the scheme—the extent to which those assets were assets for which equivalents were not readily available at the time of the scheme;

(c) the matters referred to in subsection 177D(2) of the Income Tax Assessment Act 1936 (applying paragraph 177D(2)(d) as if the reference in that paragraph to Part IVA of that Act were instead a reference to this section).

Application of this section to non‑share equity interests

(3) This section:

(a) applies to a *non‑share equity interest in the same way as it applies to a *membership interest; and

(b) applies to an *equity holder in the same way as it applies to a *member.

3 Subsection 995‑1(1)

Insert:

income tax liability, of an entity for an income year, is the amount assessed as being the amount of income tax that the entity owes (as mentioned in step 4 of the method statement in subsection 4‑10(3)) for the financial year applicable to the entity under subsection 4‑10(2).

interest in membership interests has the same meaning as in section 177EA of the Income Tax Assessment Act 1936.

scheme for a disposition, in relation to *membership interests or an *interest in membership interests, has the same meaning as in section 177EA of the Income Tax Assessment Act 1936.

Income Tax Assessment Act 1936

4 Subsection 6(1)

Insert:

loss carry back tax offset has the same meaning as in the Income Tax Assessment Act 1997.

5 After paragraph 177C(1)(ba)

Insert:

(baa) a loss carry back tax offset being allowable to the taxpayer where the whole or a part of that loss carry back tax offset would not have been allowable, or might reasonably be expected not to have been allowable, to the taxpayer if the scheme had not been entered into or carried out; or

6 After paragraph 177C(1)(e)

Insert:

(ea) in a case where paragraph (baa) applies—the amount of the whole of the loss carry back tax offset or of the part of the loss carry back tax offset, as the case may be, referred to in that paragraph; and

7 After paragraph 177C(2)(c)

Insert:

(ca) a loss carry back tax offset being allowable to the taxpayer the whole or a part of which would not have been, or might reasonably be expected not to have been, allowable to the taxpayer if the scheme had not been entered into or carried out, where:

(i) the allowance of the loss carry back tax offset to the taxpayer is attributable to the making of a declaration, agreement, election, selection or choice, the giving of a notice or the exercise of an option by any person, being a declaration, agreement, election, selection, choice, notice or option expressly provided for by this Act; and

(ii) the scheme was not entered into or carried out by any person for the purpose of creating any circumstance or state of affairs the existence of which is necessary to enable the declaration, agreement, election, selection, choice, notice or option to be made, given or exercised, as the case may be; or

8 Subsection 177C(3)

After “subparagraph (2)(a)(i), (b)(i), (c)(i),”, insert “(ca)(i),”.

9 After paragraph 177C(3)(caa)

Insert:

(cab) the allowance of a loss carry back tax offset to a taxpayer; or

10 After paragraph 177C(3)(f)

Insert:

(fa) the loss carry back tax offset would not have been allowable; or

11 After paragraph 177CB(1)(c)

Insert:

(ca) the whole or a part of a loss carry back tax offset not being allowable to the taxpayer;

12 After paragraph 177F(1)(c)

Insert:

(ca) in the case of a tax benefit that is referable to a loss carry back tax offset, or a part of a loss carry back tax offset, being allowable to the taxpayer—determine that the whole or a part of the loss carry back tax offset, or the part of the loss carry back tax offset, as the case may be, is not to be allowable to the taxpayer; or

13 After paragraph 177F(3)(c)

Insert:

(ca) if, in the opinion of the Commissioner:

(i) an amount would have been allowed, or would be allowable, to the relevant taxpayer as a loss carry back tax offset if the scheme had not been entered into or carried out, being an amount that was not allowed or would not, apart from this subsection, be allowable, as the case may be, as a loss carry back tax offset to the relevant taxpayer; and

(ii) it is fair and reasonable that the amount, or a part of the amount, should be allowable as a loss carry back tax offset to the relevant taxpayer;

determine that that amount or that part, as the case may be, should have been allowed or is allowable, as the case may be, as a loss carry back tax offset to the relevant taxpayer; or

Part 3—Consequential amendments

Income Tax Assessment Act 1936

14 Subsection 92A(3)

After “Division 36”, insert “or 160”.

15 Paragraph 175A(2)(b)

Omit “payable..”, substitute “payable.”.

Income Tax Assessment Act 1997

16 Section 13‑1 (after table item headed “long service leave”)

Insert:

losses |

|

loss carry back ............................ | Division 160 |

17 Subsection 36‑17(1) (note)

After “Note”, insert “1”.

18 At the end of subsection 36‑17(1)

Add:

Note 2: A corporate tax entity may also, in the 2020‑21 or 2021‑22 income year, be able to carry a loss back to the 2018‑19, 2019‑20 or 2020‑21 income year: see Division 160.

19 Section 36‑25 (at the end of the table dealing with tax losses of corporate tax entities)

Add:

| See also Division 160 (loss carry back tax offset for 2020‑21 or 2021‑22 for businesses with turnover under $5 billion) |

|

20 Section 36‑25 (table dealing with tax losses of pooled development funds (PDFs), item 1)

Repeal the item, substitute:

1. | A company is a pooled development fund (PDF) at the end of an income year for which it has a tax loss: it can only: (a) deduct the loss while it is a PDF; or (b) carry back the loss to an income year in which it was a PDF. | Sections 195‑5 and 195‑37 |

21 Section 36‑25 (table dealing with tax losses of VCLPs, ESVCLPs, AFOFs and VCMPs, item 1)

Repeal the item, substitute:

1. | A limited partnership that has a tax loss becomes a VCLP, an ESVCLP, an AFOF or a VCMP: it cannot: (a) deduct the loss while it is a VCLP, an ESVCLP, an AFOF or a VCMP; or (b) carry back the loss to an income year in which it was not a VCLP, an ESVCLP, an AFOF or a VCMP. | Subdivision 195‑B |

22 At the end of paragraph 195‑15(5)(b)

Add “and”.

23 After paragraph 195‑15(5)(b)

Insert:

(c) section 195‑37 does not prevent the company from *carrying back its tax loss for the purpose of working out the amount of the company’s *loss carry back tax offset for the 2020‑21 or 2021‑22 income year;

24 At the end of Subdivision 195‑A

Add:

Working out a PDF’s loss carry back tax offset

195‑37 PDF cannot carry back tax loss

A company that:

(a) has a *tax loss for an income year; and

(b) is a *PDF at the end of the income year;

cannot *carry back the loss to an earlier income year for the purposes of working out the amount of the company’s *loss carry back tax offset for the 2020‑21 or 2021‑22 income year (the offset year) unless the company is a PDF throughout the earlier income year and the offset year.

25 After section 195‑70

Insert:

A *limited partnership’s *tax loss for a *loss year cannot be *carried back to an income year during which the partnership was a *VCLP, an *ESVCLP, an *AFOF or a *VCMP.

26 Subparagraph 205‑35(1)(b)(ii)

After “applying”, insert “a *loss carry back tax offset, or”.

27 Subparagraph 205‑35(1)(b)(ii)

After “(about R&D)”, insert “,”.

28 Subsection 219‑50(2) (step 1 of the method statement)

Omit “income tax liability” (first occurring), substitute “*income tax liability”.

29 Subsection 219‑50(2) (steps 2 and 3 of the method statement)

Omit “income tax liability”, substitute “*income tax liability”.

30 After paragraph 320‑149(2)(a)

Insert:

(aa) Division 160 (Corporate loss carry back tax offset for 2020‑21 or 2021‑22 for businesses with turnover under $5 billion);

31 At the end of subsection 830‑65(3)

Add “or 160”.

32 At the end of subsection 960‑20(2)

Add:

; or (c) it is *carried back.

33 At the end of subsection 960‑20(4)

Add:

; or (f) because of it, an amount is reduced under step 2 of the method statement in subsection 160‑10(2) (which is a step in calculating a loss carry back tax offset component).

34 Subsection 995‑1(1)

Insert:

carry back: you carry back to an income year so much of a *tax loss for a later income year as you specify, in a *loss carry back choice, to be carried back to the earlier income year.

Note: You can make a loss carry back choice only for the 2020‑21 or 2021‑22 income year.

loss carry back choice has the meaning given by section 160‑15.

loss carry back tax offset has the meaning given by section 160‑5.

loss carry back tax offset component has the meaning given by subsection 160‑10(2).

35 Amendments of listed provisions—income tax liability

Omit “income tax liability” (first occurring) and substitute “*income tax liability” in the following provisions:

(a) paragraph 205‑70(4)(b);

(b) paragraph 205‑70(5)(b);

(c) subsection 219‑15(2) (table items 1, 2, 3, 4 and 9);

(d) subsection 219‑30(2) (table items 2, 3 and 4);

(e) subsection 219‑50(2);

(f) subsection 219‑50(3);

(g) subsection 219‑50(4);

(h) paragraph 219‑55(1)(a);

(i) subsection 219‑75(1);

(j) subsection 219‑75(2) (step 2 of the method statement);

(k) paragraph 219‑75(3)(a);

(l) subsection 295‑490(3);

(m) subsection 392‑95(1);

(n) subsection 961‑5(3);

(o) subsection 961‑55(3);

(p) subsection 995‑1(1) (definition of shareholders’ share).

Taxation Administration Act 1953

36 Section 45‑340 in Schedule 1 (after paragraph (da) of step 1 of the method statement)

Insert:

(db) Division 160 of the Income Tax Assessment Act 1997 (the corporate loss carry back tax offset for 2020‑21 or 2021‑22 for businesses with turnover under $5 billion); or

Schedule 3—Increasing small business entity turnover threshold for certain concessions

A New Tax System (Goods and Services Tax) Act 1999

1 After paragraph 123‑7(1)(a)

Insert:

(aa) the entity is an entity covered by subsection (1A) for the income year in which the time occurs; or

2 After subsection 123‑7(1)

Insert:

(1A) An entity is covered by this subsection for an *income year if:

(a) the entity is not a *small business entity (other than because of subsection 328‑110(4) of the *ITAA 1997) for the income year; and

(b) the entity would be such a small business entity for the income year if:

(i) each reference in Subdivision 328‑C (about what is a small business entity) of that Act to $10 million were instead a reference to $50 million; and

(ii) the reference in paragraph 328‑110(5)(b) of that Act to a small business entity were instead a reference to an entity covered by this subsection.

3 Subsection 4(1)

Insert:

eligible business entity has the meaning given by subparagraph 69(1)(d)(ia).

4 Before subparagraph 69(1)(d)(i)

Insert:

(ia) the person is a small business entity, or is a person covered by subsection (1AA), (an eligible business entity); or

5 Subparagraph 69(1)(d)(i)

Omit “a small business entity or”.

6 After subsection 69(1)

Insert:

(1AA) A person is covered by this subsection if:

(a) the person is not a small business entity; and

(b) the person would be a small business entity if:

(i) each reference in Subdivision 328‑C (about what is a small business entity) of the Income Tax Assessment Act 1997 to $10 million were instead a reference to $50 million; and

(ii) the reference in paragraph 328‑110(5)(b) of that Act to a small business entity were instead a reference to a person covered by this subsection.

7 Paragraphs 69(8)(c) and (e) and (13)(a) and (c)

Omit “a small business entity” (wherever occurring), substitute “an eligible business entity”.

8 Subsection 4(1)

Insert:

eligible business entity has the meaning given by subparagraph 61C(1)(b)(ia).

9 Before subparagraph 61C(1)(b)(i)

Insert:

(ia) the person is a small business entity, or is a person covered by subsection (1AA), (an eligible business entity); or

10 Subparagraph 61C(1)(b)(i)

Omit “a small business entity or”.

11 After subsection 61C(1)

Insert:

(1AA) A person is covered by this subsection if:

(a) the person is not a small business entity; and

(b) the person would be a small business entity if:

(i) each reference in Subdivision 328‑C (about what is a small business entity) of the Income Tax Assessment Act 1997 to $10 million were instead a reference to $50 million; and

(ii) the reference in paragraph 328‑110(5)(b) of that Act to a small business entity were instead a reference to a person covered by this subsection.

12 Paragraphs 61C(3)(c) and (e) and (8)(a) and (c)

Omit “a small business entity” (wherever occurring), substitute “an eligible business entity”.

Fringe Benefits Tax Assessment Act 1986

13 Subparagraph 58GA(1)(d)(ii)

After “small business entity”, insert “, or is an employer covered by subsection (1A),”.

14 After subsection 58GA(1)

Insert:

(1A) An employer is covered by this subsection for a year of income if:

(a) the employer is not a small business entity for the year of income; and

(b) the employer would be a small business entity for the year of income if:

(i) each reference in Subdivision 328‑C (about what is a small business entity) of the Income Tax Assessment Act 1997 to $10 million were instead a reference to $50 million; and

(ii) the reference in paragraph 328‑110(5)(b) of that Act to a small business entity were instead a reference to an employer covered by this subsection.

15 Paragraph 58X(4)(b)

After “small business entity”, insert “, or is an employer covered by subsection (5),”.

16 At the end of section 58X

Add:

(5) An employer is covered by this subsection for a year of income if:

(a) the employer is not a small business entity for the year of income; and

(b) the employer would be a small business entity for the year of income if:

(i) each reference in Subdivision 328‑C (about what is a small business entity) of the Income Tax Assessment Act 1997 to $10 million were instead a reference to $50 million; and

(ii) the reference in paragraph 328‑110(5)(b) of that Act to a small business entity were instead a reference to an employer covered by this subsection.

Income Tax Assessment Act 1936

17 Section 82KZM (heading)

After “small”, insert “and medium”.

18 Subparagraph 82KZM(1)(aa)(i)

After “small business entity”, insert “, or is covered by subsection (1A),”.

19 After subsection 82KZM(1)

Insert:

(1A) A taxpayer is covered by this subsection for a year of income if:

(a) the taxpayer is not a small business entity for the year of income; and

(b) the taxpayer would be a small business entity for the year of income if:

(i) each reference in Subdivision 328‑C (about what is a small business entity) of the Income Tax Assessment Act 1997 to $10 million were instead a reference to $50 million; and

(ii) the reference in paragraph 328‑110(5)(b) of that Act to a small business entity were instead a reference to a taxpayer covered by this subsection.

20 Paragraph 82KZMA(2)(b)

After “small business entity”, insert “, or is covered by subsection (2A),”.

21 After subsection 82KZMA(2)

Insert:

(2A) A taxpayer is covered by this subsection for the expenditure year if:

(a) the taxpayer is not a small business entity for the expenditure year; and

(b) the taxpayer would be a small business entity for the expenditure year if:

(i) each reference in Subdivision 328‑C (about what is a small business entity) of the Income Tax Assessment Act 1997 to $10 million were instead a reference to $50 million; and

(ii) the reference in paragraph 328‑110(5)(b) of that Act to a small business entity were instead a reference to a taxpayer covered by this subsection.

22 Section 82KZMD (note)

Omit “small business entity unless the small business entity”, substitute “small or medium business entity unless the entity”.

23 Subsection 170(1) (table items 1, 2 and 3)

After “small business entity” (wherever occurring), insert “or medium business entity”.

24 Subsection 170(14)

Insert:

medium business entity, for a year of income, means an entity (within the meaning of the Income Tax Assessment Act 1997) who:

(a) is not a small business entity for the year of income; and

(b) would be a small business entity for the year of income if:

(i) each reference in Subdivision 328‑C (about what is a small business entity) of that Act to $10 million were instead a reference to $50 million; and

(ii) the reference in paragraph 328‑110(5)(b) of that Act to a small business entity were instead a reference to an entity (within the meaning of that Act) covered by this definition.

Income Tax Assessment Act 1997

25 Paragraph 40‑880(2A)(c)

After “you are a *small business entity”, insert “, or an entity covered by subsection (2B),”.

26 Subparagraph 40‑880(2A)(c)(ii)

Omit “not a small business entity”, substitute “neither a small business entity, nor an entity covered by subsection (2B),”.

27 After subsection 40‑880(2A)

Insert:

(2B) An entity is covered by this subsection for an income year if:

(a) the entity is not a *small business entity for the income year; and

(b) the entity would be a small business entity for the income year if:

(i) each reference in Subdivision 328‑C (about what is a small business entity) to $10 million were instead a reference to $50 million; and

(ii) the reference in paragraph 328‑110(5)(b) to a small business entity were instead a reference to an entity covered by this subsection.

28 At the end of subsection 328‑10(1)

Add:

Note 3: Some of these concessions are also available to medium businesses (for example, see subsection 328‑285(2)).

29 At the end of subsection 328‑110(1)

Add:

Note 3: The $10 million thresholds in this subsection and in subsections (3) and (4) have been increased to $50 million for certain concessions (for example, see subsection 328‑285(2)).

30 Subdivision 328‑E (heading)

Omit “small business entities”, substitute “small and medium business entities”.

31 Section 328‑280

Omit “Small business entities”, substitute “Small and medium business entities”.

32 Section 328‑280

Omit “small business entities”, substitute “those entities”.

33 Section 328‑285 (heading)

Omit “small business entities”, substitute “small and medium business entities”.

34 Section 328‑285

Before “You can”, insert “(1)”.

35 Paragraph 328‑285(a)

After “*small business entity”, insert “, or an entity covered by subsection (2),”.

36 At the end of section 328‑285

Add:

(2) An entity is covered by this subsection for an income year if:

(a) the entity is not a *small business entity for the income year; and

(b) the entity would be a small business entity for the income year if:

(i) each reference in Subdivision 328‑C (about what is a small business entity) to $10 million were instead a reference to $50 million; and

(ii) the reference in paragraph 328‑110(5)(b) to a small business entity were instead a reference to an entity covered by this subsection.

Taxation Administration Act 1953

37 Paragraph 45‑130(1)(d) in Schedule 1

Repeal the paragraph, substitute:

(d) for the 2009‑10 income year or a later income year—you are one of the following kinds of entity (an eligible business entity):

(i) a *small business entity (other than because of subsection 328‑110(4) of the Income Tax Assessment Act 1997);

(ii) an entity covered by subsection (1A) of this section.

38 After subsection 45‑130(1) in Schedule 1

Insert:

(1A) An entity is covered by this subsection for an income year if:

(a) the entity is not a *small business entity (other than because of subsection 328‑110(4) of the Income Tax Assessment Act 1997) for the income year; and

(b) the entity would be such a small business entity for the income year if:

(i) each reference in Subdivision 328‑C (about what is a small business entity) of that Act to $10 million were instead a reference to $50 million; and

(ii) the reference in paragraph 328‑110(5)(b) of that Act to a small business entity were instead a reference to an entity covered by this subsection.

39 Subsections 45‑130(2A) and (3A) in Schedule 1

Omit “a *small business entity (other than because of subsection 328‑110(4) of the Income Tax Assessment Act 1997)”, substitute “an eligible business entity”.

Part 2—Application of amendments

40 Application of amendments

Simplified accounting methods for small enterprise entities

(1) The amendments made by this Schedule of the A New Tax System (Goods and Services Tax) Act 1999 apply in relation to working out whether an entity is a small enterprise entity at or after the start of 1 July 2021.

Customs concession

(2) The amendments made by this Schedule of the Customs Act 1901 apply in relation to applications made under subsection 69(1) of that Act on or after 1 July 2021.

Excise concession

(3) The amendments made by this Schedule of the Excise Act 1901 apply in relation to applications made under subsection 61C(1) of that Act on or after 1 July 2021.

Exempt fringe benefits

(4) The amendments made by this Schedule of the Fringe Benefits Tax Assessment Act 1986 apply in relation to benefits provided on or after 1 April 2021.

Immediate deduction for certain prepaid expenditure

(5) The amendments made by this Schedule of sections 82KZM to 82KZMD of the Income Tax Assessment Act 1936 apply in relation to expenditure incurred on or after 1 July 2020.

Amendments of assessments

(6) The amendments made by this Schedule of section 170 of the Income Tax Assessment Act 1936 apply in relation to assessments for income years starting on or after 1 July 2021.

Immediate deduction for certain start‑up expenses

(7) The amendments made by this Schedule of section 40‑880 of the Income Tax Assessment Act 1997 apply in relation to capital expenditure incurred on or after 1 July 2020.

Simplified trading stock rules

(8) The amendments made by this Schedule of Subdivision 328‑E of the Income Tax Assessment Act 1997 apply in relation to income years starting on or after 1 July 2021.

PAYG instalments based on GDP‑adjusted notional tax

(9) The amendments made by this Schedule of section 45‑130 in Schedule 1 to the Taxation Administration Act 1953 apply in relation to income years starting on or after 1 July 2021.

Schedule 4—Enhancing the R&D Tax Incentive

Income Tax Assessment Act 1997

1 Subsection 67‑30(1)

Omit “if all or part of the amount of the tax offset is worked out using the percentage in item 1 of the table in subsection 355‑100(1)”, substitute “if the amount of the tax offset is worked out in accordance with item 1 of the table in subsection 355‑100(1) (disregarding subsection 355‑100(3))”.

2 Subsection 67‑30(1) (notes)

Repeal the notes, substitute:

Note: Otherwise, the tax offset will be a non‑refundable tax offset (see item 35 of the table in subsection 63‑10(1)).

3 Subsection 355‑100(1) (heading)

Repeal the heading, substitute:

If notional deductions are between $20,000 and $150 million

4 Subsection 355‑100(1) (cell at table item 1, column headed “The percentage is:”)

Repeal the cell, substitute:

the R&D entity’s *corporate tax rate for the income year, plus 18.5 percentage points |

5 Subsection 355‑100(1) (table items 2 and 3, column headed “The percentage is:”)

Omit “38.5%”, substitute “the R&D entity’s *corporate tax rate for the income year”.

6 Subsection 355‑100(1) (note)

Repeal the note, substitute:

Note 1: The tax offset will be a refundable tax offset if item 1 of the table applies (see section 67‑30).

Note 2: The tax offset is increased under subsection (1A) of this section if item 2 or 3 of the table applies.

7 After subsection 355‑100(1)

Insert:

(1A) If item 2 or 3 of the table in subsection (1) applies to the *R&D entity, the amount of the *tax offset for the income year is increased by the sum of the amounts (if any) worked out for each item of the following table for that entity:

8 Subsection 355‑100(2)

Omit “However, if the total of those amounts is less than $20,000, the *R&D entity is instead entitled to a *tax offset for the income year equal to that percentage of”, substitute “However, if the total amount mentioned in subsection (1) is less than $20,000, the *R&D entity is instead entitled to a *tax offset for the income year, worked out in accordance with subsections (1) and (1A), as if that amount were instead”.

9 Subsection 355‑100(3)

Repeal the subsection (including the note), substitute:

If notional deductions exceed $150 million

(3) Despite subsections (1) and (1A), if the total amount mentioned in subsection (1) exceeds $150 million, the *R&D entity is instead entitled to a *tax offset for the income year equal to the sum of:

(a) the amount worked out in accordance with those subsections as if that amount were $150 million; and

(b) the product of the excess and the R&D entity’s *corporate tax rate for the income year.

10 At the end of Subdivision 355‑C

Add:

355‑115 Working out an R&D entity’s total expenses

(1) For the purposes of subsection 355‑100(1A), an *R&D entity’s total expenses for an income year is the sum of the amounts covered by subsection (2).

(2) The following amounts are covered by this subsection:

(a) the *R&D entity’s total expenses for the income year worked out in accordance with:

(i) the *accounting principles; or

(ii) if accounting principles do not apply in relation to the R&D entity—commercially accepted principles relating to accounting;

(b) any amount the R&D entity can deduct for the income year as mentioned in subsection 355‑100(1), to the extent the amount is not covered by paragraph (a) for the income year.

Amounts counted once only

(3) For the purposes of subsection (2):

(a) disregard an amount to which paragraph (2)(a) otherwise applies if paragraph (2)(b) has previously applied in relation to the amount; and

(b) disregard an amount to which paragraph (2)(b) otherwise applies if paragraph (2)(a) has previously applied in relation to the amount.

11 Section 355‑750

Repeal the section.

Tax Laws Amendment (Research and Development) Act 2015

12 Subsection 2(1) (table item 3)

Repeal the item.

13 Part 2 of Schedule 1

Repeal the Part.

14 Application of amendments

The amendments made by this Schedule apply in relation to assessments for income years commencing on or after 1 July 2021.

Schedule 5—Enhancing the integrity of the R&D Tax Incentive

Part 1—Schemes to reduce income tax

Income Tax Assessment Act 1936

1 Subsection 177A(1)

Insert:

non‑refundable R&D tax offset means a tax offset allowed under Division 355 of the Income Tax Assessment Act 1997, other than a refundable R&D tax offset.

refundable R&D tax offset means a tax offset allowed under Division 355 of the Income Tax Assessment Act 1997 that is subject to the refundable tax offset rules under section 67‑30 of that Act.

2 After paragraph 177C(1)(bc)

Insert:

or (bd) a refundable R&D tax offset, or a non‑refundable R&D tax offset, being allowable to the taxpayer in relation to a year of income where the whole or a part of the offset would not have been allowable, or might reasonably be expected not to have been allowable, to the taxpayer in relation to that year of income if the scheme had not been entered into or carried out;

3 At the end of subsection 177C(1)

Add:

; and (h) in a case to which paragraph (bd) applies—the amount of the whole of the offset or of the part of the offset, as the case may be, referred to in that paragraph.

4 At the end of subsection 177C(2)

Add:

; or (f) a refundable R&D tax offset, or a non‑refundable R&D tax offset, being allowable to the taxpayer in relation to a year of income the whole or a part of which offset would not have been, or might reasonably be expected not to have been, allowable to the taxpayer in relation to that year of income if the scheme had not been entered into or carried out, where:

(i) the allowance of the offset to the taxpayer is attributable to the making of a declaration, agreement, election, selection or choice, the giving of a notice or the exercise of an option by any person, being a declaration, agreement, election, selection, choice, notice or option expressly provided for by this Act; and

(ii) the scheme was not entered into or carried out by any person for the purpose of creating any circumstance or state of affairs the existence of which is necessary to enable the declaration, agreement, election, selection, choice, notice or option to be made, given or exercised, as the case may be.

5 Subsection 177C(3)

Omit “or (e)(i)”, substitute “, (e)(i) or (f)(i)”.

6 After paragraph 177C(3)(cb)

Insert:

or (cc) the allowance of a refundable R&D tax offset, or a non‑refundable R&D tax offset, to a taxpayer;

7 At the end of subsection 177C(3)

Add:

; or (i) the refundable R&D tax offset, or non‑refundable R&D tax offset, would not have been allowable.

8 At the end of subsection 177CB(1)

Add:

; (f) the whole or a part of a refundable R&D tax offset, or of a non‑refundable tax offset, not being allowable to the taxpayer.

9 After paragraph 177F(1)(e)

Insert:

or (f) in the case of a tax benefit that is referable to:

(i) a refundable R&D tax offset; or

(ii) a non‑refundable R&D tax offset; or

(iii) a part of a refundable R&D tax offset; or

(iv) a part of a non‑refundable R&D tax offset;

being allowable to the taxpayer in relation to a year of income—determine that the whole or a part of the offset, or the part of the offset, as the case may be, is not to be allowable to the taxpayer in relation to that year of income;

10 After paragraph 177F(3)(f)

Insert:

or (g) if, in the opinion of the Commissioner:

(i) an amount would have been allowed, or would be allowable, to the relevant taxpayer as a refundable R&D tax offset, or a non‑refundable R&D tax offset, in relation to a year of income if the scheme had not been entered into or carried out, being an amount that was not allowed or would not, apart from this subsection, be allowable, as the case may be, as a refundable R&D tax offset, or a non‑refundable R&D tax offset, as the case may be, to the relevant taxpayer in relation to that year of income; and

(ii) it is fair and reasonable that the amount, or a part of the amount, should be allowable as a refundable R&D tax offset, or a non‑refundable R&D tax offset, as the case may be, to the relevant taxpayer;

determine that that amount or that part, as the case may be, should have been allowed or is allowable, as the case may be, as a refundable R&D tax offset, or a non‑refundable R&D tax offset, as the case may be, to the relevant taxpayer in relation to that year of income;

Part 2—R&D clawback and catch up amounts

Income Tax Assessment Act 1997

11 Section 4‑25

Repeal the section, substitute:

4‑25 Special provisions for working out your basic income tax liability

Subsection 392‑35(3) may increase your basic income tax liability beyond the liability worked out simply by applying the income tax rates to your taxable income.

Note: Subsection 392‑35(3) increases some primary producers’ tax liability by requiring them to pay extra income tax on their averaging components worked out under Subdivision 392‑C.

12 Subsection 9‑5(1) (table item 4A)

Repeal the item.

13 Section 10‑5 (table item headed “R&D”)

Omit:

feedstock adjustment ........................ | 355‑465 |

substitute:

recoupments and feedstock adjustments ........... | 355‑450 |

14 Section 20‑5 (table item 10)

Repeal the item, substitute:

15 Subsection 40‑292(1)

Omit “Note”, substitute “Note 1”.

16 At the end of subsection 40‑292(1)

Add:

Note 2: To the extent that any amount is included in your assessable income under section 40‑285 in relation to R&D activities, you may have an additional amount included in your assessable income (see section 355‑447).

Note 3: To the extent any amount that you are entitled to as a deduction under section 40‑285 relates to R&D activities, you may have an additional amount you can deduct (see section 355‑466).

17 Subsections 40‑292(3) to (5)

Repeal the subsections.

18 Subsection 40‑293(1)

Omit “Note”, substitute “Note 1”.

19 At the end of subsection 40‑293(1)

Add:

Note 2: To the extent any amount that is included in the R&D partnership’s assessable income under section 40‑285 relates to R&D activities, a partner may have an additional amount included in the partner’s assessable income (see section 355‑449).

Note 3: To the extent any amount that the R&D partnership is entitled to as a deduction under section 40‑285 relates to R&D activities, a partner may have an additional amount the partner can deduct (see section 355‑468).

20 Subsection 40‑293(3)

Repeal the subsection.

21 Paragraphs 355‑100(1)(c) and (f)

Repeal the paragraphs.

22 Section 355‑105

Before “An amount”, insert “(1)”.

23 At the end of section 355‑105

Add:

(2) Subsection (1) does not apply to amounts that the *R&D entity can deduct under the following:

(a) subsection 355‑315(2);

(b) subsection 355‑475(1);

(c) subsection 355‑525(2).

24 Subdivision 355‑E (heading)

After “Notional deductions”, insert “etc.”.

25 Section 355‑300

Omit “notionally deduct” (second occurring), substitute “actually deduct”.

26 Subsection 355‑315(2) (heading)

Repeal the heading.

27 At the end of subsection 355‑315(2)

Add:

Note 1: A deduction under this subsection is not a notional deduction (see subsection 355‑105(2)).

Note 2: A deduction under this subsection results in a catch up amount for the R&D entity (see section 355‑465).

28 Subsection 355‑315(3)

Repeal the subsection, substitute:

(3) If an amount would be included in the *R&D entity’s assessable income for the event year under subsection 40‑285(1) for the asset and the event if Division 40 applied as described in paragraph (1)(e), that amount is included in the R&D entity’s assessable income for the event year.

Note: Some or all of the amount included in the R&D entity’s assessable income may result in a clawback amount for the R&D entity (see section 355‑446).

29 Subdivisions 355‑G and 355‑H

Repeal the Subdivisions, substitute:

Subdivision 355‑G—Clawback of R&D recoupments, feedstock adjustments and balancing adjustments

355‑430 What this Subdivision is about

An amount is included in an R&D entity’s assessable income if:

(a) the R&D entity receives a recoupment from government of expenditure on R&D activities for which it has obtained tax offsets under this Division; or

(b) the R&D entity can deduct under this Division expenditure on goods, materials or energy used during R&D activities to produce marketable products or products applied to the R&D entity’s own use; or

(c) a balancing adjustment event happens for an asset held by the R&D entity (or an R&D partnership in which the R&D entity is a partner) for which tax offsets have been obtained under this Division and for which an amount is otherwise included in the R&D entity’s (or R&D partnership’s) assessable income.

Table of sections

Operative provisions

355‑435 When this Subdivision applies

355‑445 Feedstock adjustments

355‑446 Balancing adjustments for assets only used for R&D activities

355‑447 Balancing adjustments for assets partially used for R&D activities

355‑448 Balancing adjustments for R&D partnership assets only used for R&D activities

355‑449 Balancing adjustments for R&D partnership assets partially used for R&D activities

355‑450 Amount to be included in assessable income

355‑435 When this Subdivision applies

This Subdivision applies to an *R&D entity for an income year (the present year) if:

(a) the R&D entity has an amount (a clawback amount) under section 355‑440, 355‑445, 355‑446, 355‑447, 355‑448 or 355‑449 for the present year; and

(b) the R&D entity has received, or is entitled to receive, a *tax offset under section 355‑100 for one or more income years (each an offset year) in relation to that clawback amount.

355‑440 R&D recoupments

(1) The *R&D entity has an amount under this section if:

(a) the entity, or another entity mentioned in subsection (5), receives or becomes entitled to receive a *recoupment from either of the following (otherwise than under the *CRC program):

(i) an *Australian government agency;

(ii) an STB (within the meaning of Division 1AB of Part III of the Income Tax Assessment Act 1936); and

(b) the recoupment is received, or the entitlement to receive the recoupment arises, during the present year; and

(c) either:

(i) the recoupment is of expenditure incurred on or in relation to certain activities; or

(ii) the recoupment requires expenditure (the project expenditure) to have been incurred, or to be incurred, on certain activities.

Note: Paragraph (c) includes expenditure incurred in purchasing a tangible depreciating asset to be used when conducting R&D activities.

(2) The amount is equal to the sum of:

(a) so much of the expenditure referred to in subsection (1) that is deducted under this Division; and

(b) for each asset (if any) for which expenditure referred to in subsection (1) is included in the asset’s *cost—each amount (if any) equal to the asset’s decline in value that is deducted under this Division;

that is taken into account in working out *tax offsets under section 355‑100 obtained by the *R&D entity for one or more income years.

Note: Paragraphs (a) and (b) of this subsection refer to amounts notionally deducted under this Division (see section 355‑105).

Amount is reduced by any repayments of the recoupment

(3) For the purposes of subsection (2), reduce the expenditure referred to in subparagraph (1)(c)(i) by any repayments of the *recoupment during an income year.

Cap on extra income tax if recoupment relates to a project

(4) Despite subsection (2), if the *recoupment is covered by subparagraph (1)(c)(ii), the amount mentioned in subsection (2) for the present year cannot exceed the amount worked out using the following formula:

where:

net amount of the recoupment means the total amount of the *recoupment, less any repayments of the recoupment during an income year.

R&D expenditure means the amount mentioned in subsection (2), disregarding subsection (3).

Related entities

(5) The other entities for the purposes of paragraph (1)(a) are as follows:

(a) an entity *connected with the *R&D entity;

(b) an *affiliate of the R&D entity or an entity of which the R&D entity is an affiliate.

(1) The *R&D entity has an amount under this section if:

(a) it incurs expenditure in one or more income years in acquiring or producing goods, or materials, (the feedstock inputs) transformed or processed during *R&D activities in producing one or more tangible products (the feedstock outputs); and

(b) it obtains under section 355‑100 *tax offsets for one or more income years (each an offset year) for deductions under this Division:

(i) for the expenditure; or

(ii) for expenditure it incurs on any energy input directly into the transformation or processing; or

(iii) for the decline in value of assets used in acquiring or producing the feedstock inputs; and

(c) during the present year, a feedstock output, or a transformed feedstock output, (the marketable product), is:

(i) *supplied by the R&D entity to another entity; or

(ii) applied by the R&D entity to the R&D entity’s own use, other than use for the purpose of transforming that product for supply.

(2) The amount is equal to the lesser of:

(a) the *feedstock revenue for the feedstock output; and

(b) so much of the total of the amounts deducted as described in paragraph (1)(b) as is reasonably attributable to the production of the feedstock output.

(3) Subsection (2) does not apply to the feedstock output if:

(a) it becomes, or is transformed into, a feedstock input; or

(b) that subsection already applies to the feedstock output because of the application of paragraph (1)(c) to:

(i) an earlier time during the present year; or

(ii) an earlier income year.

(4) The feedstock revenue, for the feedstock output, is worked out using the following formula:

where:

market value of the marketable product means the marketable product’s *market value at the time it is:

(a) *supplied by the *R&D entity to the other entity; or

(b) first applied by the R&D entity to the R&D entity’s own use, other than use for the purpose of transforming that product for supply.

(5) This section applies to a *supply or use of the marketable product by:

(a) an entity *connected with the *R&D entity; or

(b) an *affiliate of the R&D entity or an entity of which the R&D entity is an affiliate;

as if it were by the R&D entity.

355‑446 Balancing adjustments for assets only used for R&D activities

(1) The *R&D entity has an amount under this section if:

(a) a *balancing adjustment event happens in the present year for an asset *held by the R&D entity; and

(b) the R&D entity cannot deduct, for the asset for an income year, an amount under section 40‑25 as that section applies apart from:

(i) this Division; and

(ii) former section 73BC of the Income Tax Assessment Act 1936; and

(c) the R&D entity is entitled under section 355‑100 to *tax offsets for one or more income years for deductions under section 355‑305 for the asset; and

(d) the R&D entity is registered under section 27A of the Industry Research and Development Act 1986 for one or more *R&D activities for the present year; and

(e) an amount (the section 40‑285 amount) is included in the R&D entity’s assessable income for the present year under subsection 355‑315(3) for the asset and the balancing adjustment event.

Note 1: This section applies in a modified way if the entity also has deductions for the asset under former section 73BA or 73BH of the Income Tax Assessment Act 1936 (see section 355‑320 of the Income Tax (Transitional Provisions) Act 1997).

Note 2: Section 40‑292 applies if the entity can deduct an amount under section 40‑25, as that section applies apart from this Division and former section 73BC of the Income Tax Assessment Act 1936.

(2) The amount is so much of an amount equal to the section 40‑285 amount as does not exceed the difference between:

(a) the asset’s *cost; and

(b) the asset’s *adjustable value, worked out under Division 40 as if that Division applied with the changes described in section 355‑310.

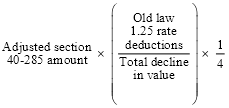

355‑447 Balancing adjustments for assets partially used for R&D activities

(1) The *R&D entity has an amount under this section if:

(a) a *balancing adjustment event happens in the present year for an asset *held by the R&D entity and for which:

(i) the R&D entity can deduct, for an income year, an amount under section 40‑25, as that section applies apart from Division 355 and former section 73BC of the Income Tax Assessment Act 1936; or

(ii) the R&D entity could have deducted, for an income year, an amount as described in subparagraph (i) if the R&D entity had used the asset; and

(b) the R&D entity is entitled under section 355‑100 to *tax offsets for one or more income years for deductions (the R&D deductions) under section 355‑305 for the asset; and

(c) an amount (the section 40‑285 amount) is included in the R&D entity’s assessable income for the asset under section 40‑285 (after applying subsection 40‑292(2)) for the present year.

Note: This section applies in a modified way if you have deductions for the asset under former section 73BA or 73BH of the Income Tax Assessment Act 1936 (see section 40‑292 of the Income Tax (Transitional Provisions) Act 1997).

(2) The amount is worked out as follows:

where:

adjusted section 40‑285 amount means so much of an amount equal to the section 40‑285 amount as does not exceed the total decline in value.

total decline in value means the *cost of the asset less its *adjustable value.

355‑448 Balancing adjustments for R&D partnership assets only used for R&D activities

(1) The *R&D entity (the partner) has an amount under this section if:

(a) the partner is a partner in an *R&D partnership; and

(b) a *balancing adjustment event happens in the present year for an asset *held by the R&D partnership; and

(c) the R&D partnership cannot deduct, for the asset for an income year, an amount under section 40‑25, as that section applies apart from:

(i) this Division; and

(ii) former section 73BC of the Income Tax Assessment Act 1936; and

(d) the partner is entitled under section 355‑100 to *tax offsets for one or more income years for deductions under section 355‑520 for the asset; and

(e) the partner is registered under section 27A of the Industry Research and Development Act 1986 for one or more *R&D activities for the present year; and

(f) an amount (the section 40‑285 amount) would, as mentioned in subsection 355‑525(3), be included in the R&D partnership’s assessable income for the present year for the asset and the balancing adjustment event.

Note 1: This section applies in a modified way if the partner has deductions for the asset under former section 73BA or 73BH of the Income Tax Assessment Act 1936 (see section 355‑325 of the Income Tax (Transitional Provisions) Act 1997).

Note 2: Section 40‑293 applies if the R&D partnership can deduct an amount under section 40‑25, as that section applies apart from this Division and former section 73BC of the Income Tax Assessment Act 1936.

(2) The amount is the partner’s proportion of the amount that is so much of an amount equal to the section 40‑285 amount as does not exceed the difference between:

(a) the asset’s *cost; and

(b) the asset’s *adjustable value, worked out under Division 40 as if that Division applied with the changes described in section 355‑310.

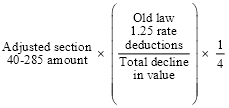

355‑449 Balancing adjustments for R&D partnership assets partially used for R&D activities

(1) The *R&D entity (the partner) has an amount under this section if:

(a) the partner is a partner in an *R&D partnership; and

(b) a *balancing adjustment event happens in the present year for a *depreciating asset *held by the R&D partnership and for which:

(i) the R&D partnership can deduct, for an income year, an amount under section 40‑25, as that section applies apart from Division 355 and former section 73BC of the Income Tax Assessment Act 1936; or

(ii) the R&D partnership could have deducted, for an income year, an amount as described in subparagraph (i) if it had used the asset; and

(c) one or more partners (including the partner) in the R&D partnership are entitled under section 355‑100 to *tax offsets for one or more income years for deductions under section 355‑520 for the asset; and

(d) an amount (the section 40‑285 amount) is included in the R&D partnership’s assessable income for the asset under section 40‑285 (after applying subsection 40‑293(2)) for the present year.

(2) The amount is the partner’s proportion of the amount worked out as follows:

where:

adjusted section 40‑285 amount means so much of an amount equal to the section 40‑285 amount as does not exceed the total decline in value.

total decline in value means the *cost of the asset less its *adjustable value.

total R&D deductions means the sum of each partner’s deductions mentioned in paragraph (1)(c) of this section.

355‑450 Amount to be included in assessable income

(1) The *R&D entity must include, in the entity’s assessable income for the present year, the sum of the following amounts for each offset year relating to the clawback amount:

where:

adjusted offset means the *tax offset the R&D entity would have received under section 355‑100 for the offset year if the total amount mentioned in subsection 355‑100(1) for that tax offset were reduced by the portion of the clawback amount that is attributable to the offset year.

deduction amount means the portion of the clawback amount that is attributable to the offset year, multiplied by the R&D entity’s *corporate tax rate for the offset year.

starting offset means the amount of the *tax offset the R&D entity has received, or is entitled to receive, under section 355‑100 for the offset year.

(2) However, if this section, or section 355‑475, has previously applied (whether in the present year or an earlier income year) in relation to another clawback amount, or catch up amount, the *R&D entity has that relates to the offset year, subsection (1) of this section applies as if:

(a) the starting offset were the *tax offset the R&D entity would have received under section 355‑100 for the offset year if the total amount mentioned in subsection 355‑100(1) were:

(i) decreased by the sum of the portions of any such other clawback amounts that are attributable to the offset year; and

(ii) increased by the sum of the portions of any such other catch up amounts that are attributable to the offset year; and

(b) the reference to the “total amount” in the definition of adjusted offset were a reference to that amount as so adjusted.

Subdivision 355‑H—Catch up deductions for balancing adjustment events for assets used for R&D activities

355‑455 What this Subdivision is about

An R&D entity can deduct an amount under this Subdivision if:

(a) a balancing adjustment event happens for an asset held by the R&D entity (or an R&D partnership in which the R&D entity is a partner); and

(b) tax offsets have been obtained under this Division for deductions for the asset; and

(c) the R&D entity (or the R&D partnership) can otherwise deduct an amount for the asset and the balancing adjustment event.

Table of sections

Operative provisions

355‑460 When this Subdivision applies

355‑465 Assets only used for R&D activities

355‑466 Assets partially used for R&D activities

355‑467 R&D partnership assets only used for R&D activities

355‑468 R&D partnership assets partially used for R&D activities

355‑475 Amount that can be deducted

355‑460 When this Subdivision applies

This Subdivision applies to an *R&D entity for an income year (the present year) if:

(a) the R&D entity has an amount (a catch up amount) under section 355‑465, 355‑466, 355‑467 or 355‑468 for an asset for the present year; and

(b) the R&D entity has received, or is entitled to receive, a *tax offset under section 355‑100 for one or more income years (each an offset year) in relation to the asset.

355‑465 Assets only used for R&D activities

(1) The *R&D entity has an amount under this section if:

(a) a *balancing adjustment event happens in the present year for an asset *held by the R&D entity; and

(b) the R&D entity cannot deduct, for the asset for an income year, an amount under section 40‑25 as that section applies apart from:

(i) this Division; and

(ii) former section 73BC of the Income Tax Assessment Act 1936; and