Treasury Laws Amendment (Major Bank Levy) Act 2017

No. 64, 2017

An Act to amend the law relating to taxation, and for related purposes

Treasury Laws Amendment (Major Bank Levy) Act 2017

No. 64, 2017

An Act to amend the law relating to taxation, and for related purposes

Contents

2 Commencement

3 Schedules

Schedule 1—Amendments

Australian Prudential Regulation Authority Act 1998

Financial Sector (Collection of Data) Act 2001

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Treasury Laws Amendment (Major Bank Levy) Act 2017

No. 64, 2017

An Act to amend the law relating to taxation, and for related purposes

[Assented to 23 June 2017]

The Parliament of Australia enacts:

This Act is the Treasury Laws Amendment (Major Bank Levy) Act 2017.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, in accordance with column 2 of the table. Any other statement in column 2 has effect according to its terms.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provisions | Commencement | Date/Details |

1. Sections 1 to 3 and anything in this Act not elsewhere covered by this table | The day this Act receives the Royal Assent. | 23 June 2017 |

2. Schedule 1 | At the same time as the Major Bank Levy Act 2017 commences. However, the provisions do not commence at all if that Act does not commence. | 24 June 2017 |

Note: This table relates only to the provisions of this Act as originally enacted. It will not be amended to deal with any later amendments of this Act.

(2) Any information in column 3 of the table is not part of this Act. Information may be inserted in this column, or information in it may be edited, in any published version of this Act.

Legislation that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

1 After subsection 56(5C)

Insert:

(5D) It is not an offence if the production by a person of a document that was given to APRA under section 13 of the Financial Sector (Collection of Data) Act 2001 is to the Commissioner of Taxation for the purposes of the Major Bank Levy Act 2017 (including the administration of that Act).

Note: A defendant bears an evidential burden in relation to matters in subsection (5D) (see subsection 13.3(3) of the Criminal Code).

2 At the end of subsection 3(1)

Add:

; and (d) reporting amounts for the purposes of the Major Bank Levy Act 2017.

3 After subsection 13(2A)

Insert:

(2B) Without limiting the matters that may be included in the reporting standards, the matters may relate to reporting of amounts for the purposes of the Major Bank Levy Act 2017.

(2C) A reporting standard made under this section may make provision in relation to a matter mentioned in subsection (2B) by applying, adopting or incorporating any matter contained in any other instrument or writing as in force or existing from time to time.

(2D) Subsection (2C) has effect despite anything in subsection 14(2) of the Legislation Act 2003.

4 After paragraph 25‑5(1)(ca)

Insert:

(cb) levy under the Major Bank Levy Act 2017; or

5 Section 960‑265 (at the end of the table)

Add:

14 | Levy threshold for the major bank levy | subsection 4(3) of the Major Bank Levy Act 2017 |

6 Subsection 960‑270(3) (including the note)

Repeal the subsection, substitute:

(3) This section does not apply in relation to amounts mentioned in the provisions listed at items 8 to 12, or at item 14, in section 960‑265.

Note: For the indexation of those amounts, see sections 960‑285 and 960‑290.

7 Subsection 960‑275(6) (including the note)

Repeal the subsection, substitute:

(6) This section does not apply in relation to amounts mentioned in the provisions listed at items 8 to 12, or at item 14, in section 960‑265.

Note: For the indexation of those amounts, see sections 960‑285 and 960‑290.

8 Subsection 960‑280(6) (including the note)

Repeal the subsection, substitute:

Exceptions

(6) This section does not apply in relation to amounts mentioned in the provisions listed at items 8 to 12, or at item 14, in section 960‑265.

Note: For the indexation of those amounts, see sections 960‑285 and 960‑290.

9 At the end of Subdivision 960‑M

Add:

(1) You index, on a *quarterly basis, the amount mentioned in the provision listed at item 14 in section 960‑265 by:

(a) first, multiplying the amount by its *indexation factor mentioned in subsection (3); and

(b) next, rounding the result in paragraph (a) down to the nearest multiple of $1,000,000.

(2) You do not index the amount if the *indexation factor is 1 or less.

(3) For indexation of the amount, the indexation factor is:

where:

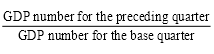

GDP number for the base quarter is the estimate that is, at the end of the *quarter to which the indexation is to be applied, the estimate of the Gross Domestic Product: Current Prices‑Seasonally Adjusted most recently published by the Australian Statistician for the *quarter ending on 30 June 2017.

GDP number for the preceding quarter is the estimate of the Gross Domestic Product: Current Prices‑Seasonally Adjusted first published by the Australian Statistician for the *quarter preceding the quarter to which the indexation is to be applied.

(4) You work out the *indexation factor mentioned in subsection (3) to 3 decimal places (rounding up if the fourth decimal place is 5 or more).

10 Subsection 995‑1(1) (at the end of the definition of BAS provisions) (before the note)

Add:

; and (e) the Major Bank Levy Act 2017.

11 Subsection 995‑1(1) (after paragraph (a) of the definition of indexation factor)

Insert:

(aa) for the amount mentioned in the provision listed at item 14 in section 960‑265—indexation factor has the meaning given by section 960‑290; or

12 Subsection 995‑1(1) (paragraph (b) of the definition of index number)

After “amount”, insert “(other than the amount mentioned in the provision listed at item 14 in section 960‑265)”.

13 Subsection 995‑1(1)

Insert:

MBL benefit has the meaning given by section 117‑15 in Schedule 1 to the Taxation Administration Act 1953.

MBL reporting day, for a *quarter, has the meaning given by subsection 115‑5(3) in Schedule 1 to the Taxation Administration Act 1953.

14 Subsection 8AAB(4) (after table item 45)

Insert:

45A | 115‑10 in Schedule 1 | Taxation Administration Act 1953 | payment of major bank levy |

15 After Part 3‑10 in Schedule 1

Insert:

An ADI that is liable to pay levy under the Major Bank Levy Act 2017 must give quarterly returns to the Commissioner.

An amount of levy is due and payable when an ADI’s last PAYG instalment within an instalment quarter is due.

Table of sections

115‑5 Returns

115‑10 When major bank levy is due and payable

(1) An *ADI that is liable to pay levy for a *quarter under the Major Bank Levy Act 2017 must give to the Commissioner a return relating to the levy, in the *approved form.

(2) The return must be given on or before the *MBL reporting day for the *quarter.

(3) The MBL reporting day for the *quarter is the day by which the *ADI is required to give to *APRA a report, in accordance with a standard determined by APRA under section 13 of the Financial Sector (Collection of Data) Act 2001, that:

(a) relates to the *quarter; and

(b) states the total liabilities amount (within the meaning of the Major Bank Levy Act 2017) for the quarter in relation to the ADI.

(1) An amount of levy under the Major Bank Levy Act 2017 that an *ADI is liable to pay for a *quarter is due and payable on the first day:

(a) that occurs on or after the *MBL reporting day for the quarter; and

(b) on which the last instalment that the ADI is liable to pay within an *instalment quarter is due under Subdivision 45‑B.

(2) If that amount remains unpaid after it is due and payable, the *ADI is liable to pay *general interest charge on the unpaid amount for each day in the period that:

(a) started at the beginning of the day by which the amount was due to be paid; and

(b) finishes at the end of the last day at the end of which either of the following remains unpaid:

(i) the amount;

(ii) general interest charge on any of the amount.

Table of Subdivisions

Guide to Division 117

117‑A Application of this Division

117‑B Commissioner may negate effects of schemes for MBL benefits

This Division applies to deter schemes that give entities MBL benefits.

If the sole or dominant purpose of entering into a scheme is to give an entity such a benefit, the Commissioner may negate the MBL benefit an entity gets from the scheme by making a determination.

Table of sections

117‑5 Object of this Division

117‑10 Application of this Division

117‑15 Meaning of MBL benefit

117‑20 Matters to be considered in determining purpose

The object of this Division is to deter *schemes to give entities benefits that reduce or defer liabilities to levy under the Major Bank Levy Act 2017.

(1) This Division applies if:

(a) an entity gets or got an *MBL benefit from a *scheme; and

(b) taking account of the matters described in section 117‑20, it is reasonable to conclude that an entity that (whether alone or with others) entered into or carried out the scheme, or part of the scheme, did so for the sole or dominant purpose of that entity or another entity getting an MBL benefit from the scheme; and

(c) the scheme:

(i) has been or is entered into at or after 7.30 pm, by legal time in the Australian Capital Territory, on 9 May 2017; or

(ii) has been or is carried out or commenced at or after that time (other than a scheme that was entered into before that time).

(2) It does not matter whether the *scheme, or any part of the scheme, was entered into or carried out inside or outside Australia.

(1) An entity gets an MBL benefit from a *scheme, if:

(a) an amount of levy under the Major Bank Levy Act 2017 that is payable by the entity under this Act apart from this Division is, or could reasonably be expected to be, smaller than it would be apart from the scheme or a part of the scheme; or

(b) all or part of an amount of levy under the Major Bank Levy Act 2017 that is payable by the entity under this Act apart from this Division is, or could reasonably be expected to be, payable later than it would have been apart from the scheme or a part of the scheme.

(2) To avoid doubt, a smaller liability mentioned in paragraph (1)(a) includes a case where the liability is zero, or there is no such liability for a particular *quarter.

The following matters are to be taken into account under section 117‑10 in considering an entity’s purpose in entering into or carrying out the *scheme, or part of the scheme:

(a) the manner in which the scheme was entered into or carried out;

(b) the form and substance of the scheme;

(c) the time at which the scheme was entered into and the length of the period during which the scheme was carried out;

(d) the effect that the Major Bank Levy Act 2017, and any other *taxation law to the extent that it applies in relation to that Act, would have in relation to the scheme apart from this Division;

(e) any change in the financial position of the entity that has resulted, or may reasonably be expected to result, from the scheme;

(f) any change that has resulted, or may reasonably be expected to result, from the scheme in the financial position of an entity (a connected entity) that has or had a connection or dealing with the entity, whether the connection or dealing is or was of a business or other nature;

(g) any other consequence for the entity or a connected entity of the scheme having been entered into or carried out;

(h) the nature of the connection (whether of a business or other nature) between the entity and a connected entity.

Table of sections

117‑25 Commissioner may negate entity’s MBL benefits

117‑30 Determination has effect according to its terms

117‑35 Commissioner may disregard scheme in making determinations

117‑40 One determination may cover several quarters etc.

117‑45 Commissioner must give copy of determination to entity affected

117‑50 Objections

(1) For the purpose of negating an *MBL benefit the entity mentioned in paragraph 117‑10(1)(a) gets or got from the *scheme, the Commissioner may:

(a) make a determination stating the amount that is (and has been at all times) the entity’s liability for levy under the Major Bank Levy Act 2017, for a specified *quarter that has ended; or

(b) make a determination stating the amount that is (and has been at all times) a particular amount mentioned in paragraph 5(2)(a) or (b) of that Act, for a specified quarter that has ended.

(2) A determination under this section is not a legislative instrument.

(3) The Commissioner may take such action as the Commissioner considers necessary to give effect to the determination.

For the purpose of making an *assessment, a statement in a determination under this Subdivision has effect according to its terms, despite the provisions of a *taxation law outside of this Division.

For the purposes of making a determination under this Subdivision, the Commissioner may:

(a) treat a particular event that actually happened as not having happened; and

(b) treat a particular event that did not actually happen as having happened and, if appropriate, treat the event as:

(i) having happened at a particular time; and

(ii) having involved particular action by a particular entity; and

(c) treat a particular event that actually happened as:

(i) having happened at a time different from the time it actually happened; or

(ii) having involved particular action by a particular entity (whether or not the event actually involved any action by that entity).

To avoid doubt, statements relating to different *quarters and different *MBL benefits may be included in a single determination under this Subdivision.

(1) The Commissioner must give a copy of a determination under this Subdivision to the entity whose liability for levy under the Major Bank Levy Act 2017 is stated in the determination.

(2) A failure to comply with subsection (1) does not affect the validity of the determination.

If the entity whose liability for levy under the Major Bank Levy Act 2017 is stated in a determination under this Subdivision is dissatisfied with the determination, the entity may object against it in the manner set out in Part IVC of the Taxation Administration Act 1953.

16 At the end of subsection 155‑5(2) in Schedule 1

Add:

; (i) an amount of levy under the Major Bank Levy Act 2017 for a *quarter.

17 Subsection 155‑15(1) in Schedule 1 (at the end of the table)

Add:

5 | an amount of levy under the Major Bank Levy Act 2017 for a *quarter | the Commissioner | return given under section 115‑5 for the quarter |

18 Subsection 250‑10(2) in Schedule 1 (after table item 135R)

Insert:

136 | amount of major bank levy | 115‑10 in Schedule 1 | Taxation Administration Act 1953 |

19 Subsection 355‑65(3) in Schedule 1 (after table item 5)

Insert:

6 | APRA | is for the purpose of administering a reporting standard made under section 13 of the Financial Sector (Collection of Data) Act 2001, to the extent that the standard relates to amounts reported to *APRA for the purposes of the Major Bank Levy Act 2017. |

20 At the end of section 356‑1 in Schedule 1

Add “and the Major Bank Levy Act 2017”.

21 At the end of Division 356 in Schedule 1

Add:

Table of sections

356‑10 Commissioner has general administration of major bank levy

The Commissioner has the general administration of the Major Bank Levy Act 2017.

22 After paragraph 357‑55(fc) in Schedule 1

Insert:

(fd) levy under the Major Bank Levy Act 2017;

23 Application of amendments

(1) The amendments made to the Income Tax Assessment Act 1997 and the Taxation Administration Act 1953 by this Schedule apply in relation to quarters starting on or after 1 July 2017.

(2) However, section 115‑10 in Schedule 1 to the Taxation Administration Act 1953 as inserted by this Act applies in relation to the quarter starting on 1 July 2017 as if the MBL reporting day for the quarter were the same day as the MBL reporting day for the quarter starting on 1 October 2017.

[Minister’s second reading speech made in—

House of Representatives on 30 May 2017

Senate on 19 June 2017]

(114/17)