Minerals Resource Rent Tax Act 2012

No. 13, 2012

An Act about a minerals resource rent tax, and for related purposes

Minerals Resource Rent Tax Act 2012

No. 13, 2012

An Act about a minerals resource rent tax, and for related purposes

Contents

Part 1‑1—Preliminary

Division 1—Preliminary

1‑1.................................Short title

1‑5.............................Commencement

1‑10............................Object of this Act

1‑15.......................Administration of this Act

1‑20...................Extension to external Territories

1‑25......................Extraterritorial application

Part 1‑2—A guide to this Act

Division 2—Overview of this Act

2‑1..........................What this Act is about

2‑5........................How this Act is arranged

Division 3—Defined terms

3‑1...................When defined terms are identified

3‑5.....................When terms are not identified

3‑10.............Identifying the defined term in a definition

Division 4—Status of guides and other non‑operative material

4‑1....................................Non‑operative material

4‑5...................................Guides

4‑10..............................Other material

Chapter 2—General liability rules

Part 2‑1—Core rules

Division 10—Core rules

10‑1....................A miner’s liability for MRRT

10‑5.........The MRRT liability for a mining project interest

10‑10..........................MRRT allowances

10‑15...The effect of low profits on a miner’s liability for MRRT

10‑20..........................Payment of MRRT

10‑25..............................MRRT years

Part 2‑2—Mining project interests

Division 15—Mining project interests

Guide to Division 15

15‑1......................What this Division is about

Operative provisions

15‑5.........................When an entity has a mining project interest

15‑10.......Iron ore mining project interests to be kept separate

15‑15..............................Meaning of production right

15‑20..............................Meaning of project area

Division 20—Taxable resources

Guide to Division 20

20‑1......................What this Division is about

Operative provisions

20‑5................................What are taxable resources

Part 2‑3—Mining profits

Division 25—Mining profits

Guide to Division 25

25‑1......................What this Division is about

Operative provisions

25‑5..........................How to work out the mining profit for a mining project interest

Division 30—Mining revenue

Guide to Division 30

30‑1......................What this Division is about

Subdivision 30‑A—A miner’s mining revenue

30‑5................................A miner’s mining revenue

Subdivision 30‑B—Revenue from supply, export or use of taxable resources

30‑10When amounts from taxable resources etc. are included in mining revenue

30‑15.................Meaning of mining revenue event

30‑20..............................Meaning of initial supply

30‑25................Working out amounts to be included

30‑30..............................Meaning of arm’s length consideration

30‑35.......................When supplies are made

Subdivision 30‑C—Other revenue

30‑40.........Recoupment or offsetting of mining expenditure

30‑45....Recoupment of payments that give rise to royalty credits

30‑50............Compensation for loss of taxable resources

30‑55 Amounts that do not relate to a particular mining revenue event

Subdivision 30‑D—Miscellaneous

30‑60..........................No double counting

30‑65..Expenditure incurred in causing amounts to be received etc.

30‑70....................Amounts taken to be received

30‑75..................GST and increasing adjustments

Division 35—Mining expenditure

Guide to Division 35

35‑1......................What this Division is about

Subdivision 35‑A—A miner’s mining expenditure

35‑5................................A miner’s mining expenditure

35‑10.........................General expenditure

35‑15..............................Meaning of upstream mining operations

35‑20..............................Meaning of mining operations

35‑25..........................No double counting

Subdivision 35‑B—Excluded expenditure

35‑35.........Cost of acquiring rights and interests in projects

35‑40................................Royalties

35‑45..............................Meanings of mining royalty and private mining royalty

35‑50............................Financing costs

35‑55......................Hire purchase agreements

35‑60...................................Non‑adjacent land and buildings used in administrative or accounting activities

35‑65............Hedging or foreign exchange arrangements

35‑70..............Rehabilitation bond and trust payments

35‑75..................Payments of income tax or GST

Division 40—Valuation point

Guide to Division 40

40‑1......................What this Division is about

Operative provisions

40‑5...............................Meaning of valuation point

Part 2‑4—Low profit offsets

Division 45—Low profit offsets

Guide to Division 45

45‑1......................What this Division is about

Operative provisions

45‑5......Low profit offset—profits not greater than $75 million

45‑10Low profit offset—profits greater than $75 million and less than $125 million

Part 2‑5—Payment of MRRT

Division 50—How to work out when to pay MRRT

Guide to Division 50

50‑1......................What this Division is about

Operative provisions

50‑5..................When assessed MRRT is payable

50‑10.............When shortfall interest charge is payable

50‑15General interest charge payable on unpaid assessed MRRT or shortfall interest charge

Chapter 3—MRRT allowances

Part 3‑1—Royalty allowances

Division 60—Royalty allowances

Guide to Division 60

60‑1......................What this Division is about

Operative provisions

60‑5........................Objects of this Division

60‑10...............When a miner has a royalty allowance

60‑15.................The amount of a royalty allowance

60‑20.....................When a royalty credit arises

60‑25......................Amount of a royalty credit

60‑30.............Royalty credits reduced by recoupments

Part 3‑2—Transferred royalty allowances

Division 65—Transferred royalty allowances

Guide to Division 65

65‑1......................What this Division is about

Operative provisions

65‑5.........................Object of this Division

65‑10........When a miner has a transferred royalty allowance

65‑15..........The amount of a transferred royalty allowance

65‑20.......................Available royalty credits

Part 3‑3—Pre‑mining loss allowances

Division 70—Pre‑mining loss allowances

Guide to Division 70

70‑1......................What this Division is about

Subdivision 70‑A—Object of this Division

70‑5........................Objects of this Division

Subdivision 70‑B—When a miner has a pre‑mining loss allowance

70‑10.......................When a miner has a pre‑mining loss allowance

70‑15.........................The amount of a pre‑mining loss allowance

70‑20.............................Available pre‑mining losses for a pre‑mining loss allowance

70‑25..............................Meaning of pre‑mining project interest etc.

Subdivision 70‑C—Pre‑mining losses

70‑30....................................Pre‑mining losses

70‑35..............................Meaning of pre‑mining expenditure etc.

70‑40..............................Meaning of pre‑mining revenue

Subdivision 70‑D—Amounts of pre‑mining losses

70‑45....................................Pre‑mining losses for the MRRT years in which they arise

70‑50....................................Pre‑mining losses for later MRRT years

Part 3‑4—Mining loss allowances

Division 75—Mining loss allowances

Guide to Division 75

75‑1......................What this Division is about

Operative provisions

75‑5........................Objects of this Division

75‑10............When a miner has a mining loss allowance

75‑15..............The amount of a mining loss allowance

75‑20.............................Mining losses

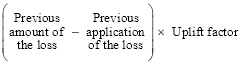

Part 3‑5—Starting base allowances

Division 80—Starting base allowances

Guide to Division 80

80‑1......................What this Division is about

Subdivision 80‑A—Objects of this Division

80‑5........................Objects of this Division

Subdivision 80‑B—When a miner has a starting base allowance

80‑10...........When a miner has a starting base allowance

80‑15.............The amount of a starting base allowance

80‑20...............When a miner has a starting base loss

Subdivision 80‑C—Starting base assets

80‑25..............................Meaning of starting base asset

80‑30...Treating starting base assets as a single starting base asset

80‑35..Mine development expenditure may be a starting base asset

Subdivision 80‑D—Amounts of starting base losses

80‑40..Starting base losses for the MRRT years in which they arise

80‑45.............Starting base losses for later MRRT years

80‑50...........Mining project interests originating from pre‑mining project interests with different valuation approaches

Division 85—Valuation approaches

Guide to Division 85

85‑1......................What this Division is about

Operative provisions

85‑5....................Choosing a valuation approach

85‑10.......Restriction on specifying the book value approach

85‑15......The valuation approach for a mining project interest

Division 90—Declines in value of starting base assets

Guide to Division 90

90‑1......................What this Division is about

Subdivision 90‑A—How to work out the decline in value of a starting base asset

90‑5..How to work out the decline in value of a starting base asset

90‑10..........Write off rates under the book value approach

90‑15.........Write off rates under the market value approach

Subdivision 90‑B—Base values under the book value approach

90‑20...................Application of this Subdivision

90‑25...........................Initial base value

90‑30...........................Later base values

Subdivision 90‑C—Base values under the market value approach

90‑35...................Application of this Subdivision

90‑40...........................Initial base value

90‑45...........Mining project interest originating from pre‑mining project interests etc.

90‑50...........................Later base values

Subdivision 90‑D—Miscellaneous

90‑55..............................Meaning of interim expenditure

90‑60..Partial disposal of a starting base asset before the start time

90‑65.........Recoupment of the value of a starting base asset

Part 3‑6—Transferred pre‑mining loss allowances

Division 95—Transferred pre‑mining loss allowances

Guide to Division 95

95‑1......................What this Division is about

Operative provisions

95‑5.........................Object of this Division

95‑10.................When a miner has a transferred pre‑mining loss allowance

95‑15...................The amount of a transferred pre‑mining loss allowance

95‑20.............................Available pre‑mining losses for a transferred pre‑mining loss allowance

95‑25.........................Cap on available pre‑mining losses

95‑30...................................The pre‑mining loss cap

Part 3‑7—Transferred mining loss allowances

Division 100—Transferred mining loss allowances

Guide to Division 100

100‑1.....................What this Division is about

Operative provisions

100‑5........................Object of this Division

100‑10....When a miner has a transferred mining loss allowance

100‑15......The amount of a transferred mining loss allowance

100‑20......................Available mining losses

100‑25......................Common ownership test

Chapter 4—Specialist liability rules

Part 4‑1—Mining project interests

Division 115—Combining mining project interests

Guide to Division 115

115‑1.....................What this Division is about

Subdivision 115‑A—Object of this Division

115‑5........................Object of this Division

Subdivision 115‑B—When mining project interests are combined

115‑10Mining project interests may be treated as the same mining project interest

115‑15......................Choosing to override non‑compliance

115‑20.................Transferability of royalty credits

115‑25........................Transferability of pre‑mining losses

115‑30..................Transferability of mining losses

115‑35...........Starting base losses and starting base assets

Subdivision 115‑C—The effect of combining mining project interests

115‑40........The effect of combining mining project interests

115‑45..Allowance components arising in preceding MRRT years

115‑50..Different valuation approaches for mining project interests

115‑55............................Transferred pre‑mining loss allowances

115‑60...............Transferred mining loss allowances

115‑65...........Choice of the alternative valuation method

Division 120—Transferring mining project interests

Guide to Division 120

120‑1.....................What this Division is about

Operative provisions

120‑5........................Object of this Division

120‑10.................Effect of mining project transfer

120‑15...................Effect of transferred property

120‑20.........Events happening after mining project transfer

120‑25..Start of mining venture taken to be mining project transfer

Division 125—Splitting mining project interests

Guide to Division 125

125‑1.....................What this Division is about

Operative provisions

125‑5........................Object of this Division

125‑10...................Effect of mining project split

125‑15.............................Meaning of split percentage

125‑20...................Effect of transferred property

125‑25Effect of MRRT liability from earlier years on rehabilitation tax offset amounts

125‑30...........Events happening after mining project split

125‑35....Start of mining venture taken to be mining project split

Division 130—Winding down mining project interests

Guide to Division 130

130‑1.....................What this Division is about

Operative provisions

130‑5........................Object of this Division

130‑10..........Suspension days for mining project interests

130‑15..............Extinguishing allowance components

130‑20................Restarting commercial production

Division 135—Ending mining project interests

Guide to Division 135

135‑1.....................What this Division is about

Operative provisions

135‑5........The termination day for a mining project interest

135‑10.....The effect of renewing or changing production rights

135‑15......The effect of renewing or changing mining ventures

135‑20The effect of mining project transfers and mining project splits

135‑25...Continuation of obligations etc. after the termination day

Part 4‑2—Pre‑mining project interests

Division 140—Pre‑mining profits and royalty credits

Guide to Division 140

140‑1.....................What this Division is about

Subdivision 140‑A—Pre‑mining profits

140‑5....................................Pre‑mining profits

140‑10...........................Treatment of pre‑mining profits—general rule

140‑15Effect on allowance components for other mining project interests

140‑20...........................Treatment of pre‑mining profits—mining project interest originating from the pre‑mining project interest

Subdivision 140‑B—Pre‑mining royalty credits

140‑25...................................Pre‑mining royalty credits

Division 145—Transferring pre‑mining project interests

Guide to Division 145

145‑1.....................What this Division is about

Operative provisions

145‑5........................Object of this Division

145‑10.........................Continuation of pre‑mining project interest

145‑15.............................Effects of pre‑mining project transfer

145‑20...................Effect of transferred property

145‑25.....................Events happening after pre‑mining project transfer

145‑30...................................Pre‑mining project transfer when mining project interest originates

Division 150—Splitting pre‑mining project interests

150‑1...........................Guide to Division 150

Operative provisions

150‑5........................Object of this Division

150‑10.........................Continuation of pre‑mining project interest

150‑15.............................Effects of pre‑mining project split

150‑20...................Effect of transferred property

150‑25Effect of MRRT liability from earlier years on rehabilitation tax offset amounts

150‑30.....................Events happening after pre‑mining project split

150‑35...................................Pre‑mining project split when mining project interest originates

Division 155—Ending pre‑mining project interests

Guide to Division 155

155‑1.....................What this Division is about

Operative provisions

155‑5....................The termination day for a pre‑mining project interest

155‑10.....The effect of renewing or changing exploration rights

155‑15...........................The effect of pre‑mining project transfers and pre‑mining project splits

155‑20...Continuation of obligations etc. after the termination day

155‑25..............Extinguishing allowance components

Part 4‑3—Adjusting MRRT liabilities

Division 160—Adjustments to revenue and expenditure of project interests

Guide to Division 160

160‑1.....................What this Division is about

Operative provisions

160‑5........................Object of this Division

160‑10.........................Mining adjustments

160‑15Effect of mining adjustments on mining revenue, mining expenditure etc.

Division 165—Starting base adjustments

Guide to Division 165

165‑1.....................What this Division is about

Subdivision 165‑A—Starting base adjustment events and starting base adjustment amounts

165‑5...................Starting base adjustment events

165‑10.................Starting base adjustment amounts

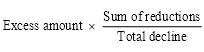

165‑15.....Reductions in declines in value of starting base assets

Subdivision 165‑B—General rules for starting base adjustments

165‑20.....................Starting base adjustments

165‑25 The effect of starting base adjustments on starting base losses

165‑30The effect of negative starting base adjustments on mining revenue

Subdivision 165‑C—Partial disposal of starting base assets

165‑35Starting base adjustments for partial disposal of starting base assets

165‑40...Declines in value of retained parts of starting base assets

165‑45.................Reductions in starting base losses

165‑50...............Base value for the next MRRT year

Subdivision 165‑D—Miscellaneous

165‑55Use etc. of starting base assets for other mining project interests etc.

165‑60Effect on base value of use etc. of starting base assets after starting base adjustment events

Part 4‑4—Valuation

Division 170—Valuation principles

Guide to Division 170

170‑1.....................What this Division is about

Operative provisions

170‑5.........Valuations to comply with valuation principles

170‑10......................The valuation principles

Division 175—Alternative valuation method

Guide to Division 175

175‑1.....................What this Division is about

Subdivision 175‑A—Object of this Division

175‑5........................Object of this Division

Subdivision 175‑B—Choosing to use the alternative valuation method

175‑10.......Choosing to use the alternative valuation method

175‑15..............Group production of taxable resources

Subdivision 175‑C—Amounts included in mining revenue under the alternative valuation method

175‑20When amounts are included in mining revenue under the alternative valuation method

175‑25................How to work out the single amount

175‑30...................Unadjusted revenue amounts

175‑35....................Downstream operating costs

175‑40........................Depreciation of assets

175‑45.......................Return on capital costs

Division 180—Valuation of starting base assets using the look‑back approach

Guide to Division 180

180‑1.....................What this Division is about

Operative provisions

180‑5.....................Choosing to apply the look‑back approach

180‑10........................The effect of the look‑back approach on valuation of mining project interests

Part 4‑5—Accounting for MRRT

Division 185—Currency translation

Guide to Division 185

185‑1.....................What this Division is about

Operative provisions

185‑5.......................Objects of this Division

185‑10........Translation of amounts into Australian currency

185‑15.....................Functional currency rules

185‑20Functional currency rules—Australian permanent establishments

185‑25......................Special translation rules

Division 190—Substituted accounting periods

Guide to Division 190

190‑1.....................What this Division is about

Operative provisions

190‑5........................Object of this Division

190‑10...Accounting periods recognised for income tax purposes

190‑15..................Changes in accounting periods

190‑20The effect of transitional accounting periods on threshold amounts

190‑25 The effect of transitional accounting periods on uplift factors

Division 195—Non‑cash benefits

Guide to Division 195

195‑1.....................What this Division is about

Operative provisions

195‑5........................Object of this Division

195‑10..........................Barter transactions

195‑15...........................Gift transactions

Division 200—Simplified MRRT method

Guide to Division 200

200‑1.....................What this Division is about

Operative provisions

200‑5..............Effect of the simplified MRRT method

200‑10.........Choosing to use the simplified MRRT method

200‑15Working out an entity’s profit for simplified MRRT method purposes

Part 4‑6—Integrity measures

Division 205—Anti‑profit shifting

Guide to Division 205

205‑1.....................What this Division is about

Operative provisions

205‑5..........................Object of Division

205‑10.............Amounts to reflect independent dealings

205‑15Method to be used when determining amounts for the purposes of this Division

205‑20....Commissioner may compensate entity or another entity

205‑25...................Commissioner determinations

Division 210—Anti‑avoidance

Guide to Division 210

210‑1.....................What this Division is about

Subdivision 210‑A—Application of this Division

210‑5........................Object of this Division

210‑10..................When does this Division apply?

210‑15..When does an entity get an MRRT benefit from a scheme?

210‑20........Matters to be considered in determining purpose

Subdivision 210‑B—Commissioner may negate effects of schemes for MRRT benefits

210‑25......Commissioner may negate entity’s MRRT benefits

210‑30....Commissioner may compensate entity or another entity

210‑35....One determination may cover several MRRT years etc.

210‑40Commissioner must give copy of determination to entity affected

Part 4‑7—Entities

Division 215—Consolidated groups

Guide to Division 215

215‑1.....................What this Division is about

Operative provisions

215‑5.......................Objects of this Division

215‑10...........Choice to consolidate for MRRT purposes

215‑15..........................Single entity rule

215‑20.Project interests transferred to head company etc. on joining

215‑25....Project interests transferred to leaving entity on leaving

215‑30 Mining project interests etc. split to leaving entity on leaving

215‑35Acquisition of consolidated group by another consolidated group etc.

215‑40...Instalment rates for leaving entity or new head company

215‑45Effect of choice to continue group after shelf company becomes new head company

215‑50Effect of change of head company or provisional head company of a MEC group

215‑55......Effect of group conversions involving MEC groups

Division 220—Partnerships and unincorporated associations and bodies

Guide to Division 220

220‑1.....................What this Division is about

Operative provisions

220‑5..............................Partnerships

220‑10.............Unincorporated associations and bodies

Part 4‑8—Miscellaneous

Division 225—Rehabilitation tax offsets

Guide to Division 225

225‑1.....................What this Division is about

Operative provisions

225‑5........................Object of this Division

225‑10.............Entitlement to rehabilitation tax offsets

225‑15Rehabilitation tax offset amounts relating to mining project interests

225‑20........Rehabilitation tax offset amounts relating to pre‑mining project interests

225‑25.............Application of rehabilitation tax offsets

Chapter 5—Miscellaneous

Division 235—Miscellaneous

235‑1..............................Regulations

Chapter 6—Interpreting this Act

Part 6‑1—Rules for interpreting this Act

Division 245—Rules for interpreting this Act

245‑1.....................What forms part of this Act

245‑5................What does not form part of this Act

245‑10........................Guides and other non‑operative provisions, and their role in interpreting this Act

Part 6‑2—Meaning of some important concepts

Division 250—Meaning of hold

Guide to Division 250

250‑1.....................What this Division is about

Operative provisions

250‑5..............................Meaning of hold

250‑10............When certain starting base assets are held

250‑15.....................Things that are jointly held

Division 255—Integrated mining project interests

Guide to Division 255

255‑1.....................What this Division is about

Operative provisions

255‑5.........Upstream integration of mining project interests

255‑10......Downstream integration of mining project interests

255‑15.............................Meaning of downstream mining operations

255‑20.........................Choice to integrate

Part 6‑3—Dictionary

Division 300—Dictionary

300‑1...............................Dictionary

Minerals Resource Rent Tax Act 2012

No. 13, 2012

An Act about a minerals resource rent tax, and for related purposes

[Assented to 29 March 2012]

The Parliament of Australia enacts:

This Act may be cited as the Minerals Resource Rent Tax Act 2012.

This Act commences on 1 July 2012.

The object of this Act is to ensure that the Australian community receives an adequate return for its *taxable resources, having regard to:

(a) the inherent value of the resources; and

(b) the non‑renewable nature of the resources; and

(c) the extent to which the resources are subject to Commonwealth, State and Territory royalties.

This Act does this by taxing above normal profits made by miners (also known as economic rents) that are reasonably attributable to the resources in the form and place they were in when extracted.

1‑15 Administration of this Act

The Commissioner has the general administration of this Act.

Note: An effect of this provision is that people who acquire information under this Act are subject to the confidentiality obligations in Division 355 in Schedule 1 to the Taxation Administration Act 1953.

1‑20 Extension to external Territories

The *MRRT law extends to every external Territory other than the Australian Antarctic Territory.

1‑25 Extraterritorial application

The *MRRT law extends to acts, omissions, matters and things outside *Australia (except where a contrary intention appears).

Division 2—Overview of this Act

This Act works out a miner’s MRRT liability on mining profits made from extracting taxable resources (mainly coal and iron ore) for a mining project interest for a year.

A mining project interest is principally a share of the output of an undertaking to extract taxable resources. Mining profit consists of mining revenue less mining expenditure. The sum of the miner’s mining profits for its interests are taxed at the MRRT rate.

Mining revenue is mainly that part of the revenue the miner makes from supplying, exporting or using extracted taxable resources (or things produced from them) that reasonably relates to the form and place the resources were in at their valuation point (usually when leaving the run‑of‑mine stockpile).

Mining expenditure is mainly the costs of finding and extracting the taxable resources and getting them to their valuation point.

Mining profit may be reduced by allowances for past losses, for the miner’s existing investments at 2 May 2010 (called a starting base allowance), and for the miner’s Commonwealth, State and Territory mining royalty amounts. Some allowances can be transferred to other mining project interests to reduce their mining profits.

If the total mining profits of the miner and certain connected entities is $75 million or less, a low‑profit offset will ensure that the miner has no liability for MRRT. The offset is phased‑out for profits between $75 million and $125 million.

(1) This Act is arranged in a way that reflects the principle of moving from the general case to the particular.

(2) In this respect, the conceptual structure of the Act is something like a pyramid. The pyramid shape illustrates the way the MRRT law is organised, moving down from the central or core provisions at the top of the pyramid, to general rules of wide application and then to the more specialised topics.

Note: Provisions relating to the administration of the MRRT and to collection and recovery of amounts of MRRT or instalments of MRRT are contained in Schedule 1 to the Taxation Administration Act 1953.

3‑1 When defined terms are identified

(1) Many of the terms used in the MRRT law are defined.

(2) Most defined terms in this Act are identified by an asterisk appearing at the start of the term: as in “*MRRT year”.

3‑5 When terms are not identified

(1) Once a defined term has been identified by an asterisk, later occurrences of the term in the same subsection are not usually asterisked.

(2) Terms are not asterisked in the non‑operative material contained in this Act.

Note: The non‑operative material is described in Division 4.

(3) The following basic terms used throughout the Act are not identified with an asterisk:

Common definitions that are not asterisked | |

Item | Term |

1 | Commissioner |

2 | extract |

3 | miner |

4 | mining project interest |

5 | MRRT |

3‑10 Identifying the defined term in a definition

Within a definition, the defined term is identified by bold italics.

Division 4—Status of guides and other non‑operative material

(1) In addition to the operative provisions themselves, this Act contains other material to help readers identify accurately and quickly the provisions that are relevant to them and to help them understand those provisions.

(2) This other material falls into 2 main categories, see sections 4‑5 and 4‑10.

(1) One category is the guide in many Divisions. Under the heading “What this Division is about’, a short explanation of the Division appears in boxed text.

(2) Guides form part of this Act but are not operative provisions. In interpreting an operative provision, guides may only be considered for limited purposes. These are set out in subsection 245‑10(2).

The other category consists of material such as notes and examples. These also form part of the Act. They are usually distinguished by font size from the operative provisions, but are not kept separate from them.

Chapter 2—General liability rules

Table of sections

10‑1 A miner’s liability for MRRT

10‑5 The MRRT liability for a mining project interest

10‑10 MRRT allowances

10‑15 The effect of low profits on a miner’s liability for MRRT

10‑20 Payment of MRRT

10‑25 MRRT years

10‑1 A miner’s liability for MRRT

A miner is liable to pay MRRT, for an *MRRT year, equal to the sum of its *MRRT liabilities for each of its mining project interests for that year.

Note: For mining project interests, see Part 2‑2.

10‑5 The MRRT liability for a mining project interest

Work out the miner’s MRRT liability for a mining project interest for an *MRRT year as follows:

Method statement

Step 1. Work out the miner’s *mining profit for the mining project interest for the *MRRT year.

Note: For the mining profit, see Part 2‑3.

Step 2. Work out the miner’s *MRRT allowances for the mining project interest for the *MRRT year.

Note: For MRRT allowances, see section 10‑10.

Step 3. Subtract the *MRRT allowances from the *mining profit.

Step 4. Multiply the result by the *MRRT rate. This is the miner’s MRRT liability for the mining project interest for the *MRRT year.

Note 1: For the MRRT rate, see section 300‑1.

Note 2: If the result from step 3 is zero, the miner’s MRRT liability will also be zero.

The MRRT allowances, and the order in which they are applied in working out *MRRT liabilities, are as follows:

MRRT allowances | ||

Item | Order of applying the MRRT allowances | See: |

1 | *Royalty allowance | Part 3‑1 |

2 | *Transferred royalty allowance | Part 3‑2 |

3 | *Pre‑mining loss allowance | Part 3‑3 |

4 | *Mining loss allowance | Part 3‑4 |

5 | *Starting base allowance | Part 3‑5 |

6 | *Transferred pre‑mining loss allowance | Part 3‑6 |

7 | *Transferred mining loss allowance | Part 3‑7 |

Note: MRRT allowances are made up of allowance components, up to the amount of the relevant mining profit.

10‑15 The effect of low profits on a miner’s liability for MRRT

If the miner has an offset under section 45‑5 or 45‑10 for the *MRRT year, the amount of MRRT that the miner must pay for the MRRT year is reduced by the amount of the offset.

Note 1: For low profit offsets, see Part 2‑4.

Note 2: A miner is not liable to pay MRRT for the MRRT year if the miner has chosen to use the simplified MRRT method under Division 200.

The miner must pay to the Commonwealth its *assessed MRRT for the *MRRT year on or before the day on which the assessed MRRT becomes due and payable.

Note 1: For payment of MRRT, see Part 2‑5.

Note 2: Division 115 in Schedule 1 to the Taxation Administration Act 1953 provides for payment of MRRT by instalments.

Note 3: Rehabilitation tax offsets reduce the amount of MRRT that the miner must pay: see section 225‑25.

An MRRT year is a *financial year starting on or after 1 July 2012.

Note: Other accounting periods may be MRRT years if a miner uses, for income tax purposes, an accounting period other than a financial year: see Division 190 (Substituted accounting periods).

Part 2‑2—Mining project interests

Division 15—Mining project interests

15‑1 What this Division is about

The concept of a mining project interest is central to the MRRT. A miner’s liability is based on its MRRT liabilities for each of its mining project interests.

Note: Chapter 4 contains special rules about mining project interests, including combining, transferring and splitting of mining project interests, and their suspension and termination.

Table of sections

Operative provisions

15‑5 When an entity has a mining project interest

15‑10 Iron ore mining project interests to be kept separate

15‑15 Meaning of production right

15‑20 Meaning of project area

15‑5 When an entity has a mining project interest

Mining project interest arising from a mining venture

(1) An *entity has a mining project interest to the extent that the entity is entitled to share in the output of a *mining venture in which the entity participates (whether actively or otherwise, and whether alone or with one or more other entities).

Note 1: There may be more than one mining venture to extract taxable resources from an area covered by a production right.

Note 2: Changing or renewing a mining venture does not cause the termination day of a mining project interest: see section 135‑15.

(2) If the *mining venture relates to one or more *production rights, the *entity has a separate mining project interest in relation to each production right.

Example: Scouting Resources participates in a mining venture relating to the extraction of taxable resources from an area covered by 3 production rights. Scouting Resources has 3 mining project interests, one in relation to each production right.

Meaning of mining venture

(3) An undertaking is a mining venture if the purpose, or a purpose, of the undertaking is:

(a) to extract some or all of the *taxable resources from the area covered by one or more *production rights; and

(b) to produce an output that is a taxable resource extracted under the authority of the production right or rights, or something produced using such a taxable resource.

Example: CheckCo and BelCo enter into a contractual arrangement under which they agree to jointly extract and process iron ore from the whole area covered by a mining lease, and each take an equal share of the ore once it has been pelletised.

Participation in this undertaking gives rise to a mining project interest for each of CheckCo and BelCo, comprising their respective entitlements to share in the pellets produced from the mining venture.

Residual mining project interest

(4) An *entity has a mining project interest to the extent that:

(a) the entity is entitled to extract *taxable resources from the area covered by a *production right; and

(b) there is no *mining venture, relating to the extraction of those taxable resources, that gives rise to a mining project interest for one or more entities under subsection (1).

Note 1: The start of a mining venture relating to the extraction of those taxable resources is treated as a mining project transfer (if the venture relates to all of the resources), or otherwise, a mining project split: see section 120‑25 (for transfers) or 125‑35 (for splits).

Note 2: Changing or renewing a production right does not cause the termination day of a mining project interest: see section 135‑10.

Example: LesseeCo holds a mining lease, with a term of 21 years, to extract coal from an area. LesseeCo enters into a sublease with DiggerCo, giving DiggerCo the exclusive right to extract coal from the whole area for a period of 3 years.

LesseeCo has a mining project interest under this subsection comprising its entitlement to extract coal from the area after the expiration of the 3 year sublease.

If there is no mining venture relating to the coal that may be extracted under the sublease, DiggerCo has a mining project interest under this subsection comprising its entitlement to extract the coal under the sublease.

Further entitlements constitute new mining project interest

(5) If, after the *entity becomes entitled as mentioned in subsection (1) or (4), the entity becomes so entitled to a further extent, the entity is taken to have a separate mining project interest corresponding to that further extent.

Note: The separate mining project interests are combined into a single mining project interest under Division 115 if the requirements of that Division are met.

Example: CheckCo and BelCo each have a mining project interest comprising an entitlement to share in the output of a mining venture in which they both participate.

CheckCo transfers its interest in the mining venture to BelCo (Division 120, about transferring mining project interests, applies). BelCo then has a mining project interest comprising the entitlement it acquired from CheckCo to share in the output of the venture. That mining project interest is separate from CheckCo’s original mining project interest.

Royalties not to give rise to mining project interest

(6) To avoid doubt, a *mining royalty or a *private mining royalty is not an output mentioned in subsection (1), unless it is a private mining royalty that is payable in kind.

Example: CheckCo and BelCo each participate in a mining venture that produces pelletised iron ore from the area covered by a production right. Under the contractual arrangement between the parties, CheckCo is entitled to take all the pelletised iron ore, and is required to pay BelCo an amount of money calculated by reference to the quantity of iron ore extracted under the mining venture.

CheckCo has a mining project interest under subsection (1), BelCo does not.

However, if CheckCo was required to pay BelCo in pelletised iron ore, BelCo would also have a mining project interest under subsection (1).

15‑10 Iron ore mining project interests to be kept separate

If, apart from this section, a mining project interest would relate to both iron ore and *taxable resources other than iron ore, treat the interest as:

(a) a mining project interest relating to iron ore; and

(b) another mining project interest relating to taxable resources other than iron ore.

15‑15 Meaning of production right

(1) A production right is:

(a) an authority or right (however described) under an *Australian law to extract a *taxable resource from a particular area in *Australia; or

(b) if an authority or right (however described) under an Australian law is not required to extract a taxable resource from a particular area—an interest in an area in *Australia that allows a person to extract a taxable resource from the area.

Examples: The following are some examples of production rights:

(a) a mining lease;

(b) a mining lease subject to environmental approval;

(c) a mining licence.

(2) However, an *exploration right is not a production right.

Note: An exploration right may give rise to a pre‑mining project interest: see section 70‑25.

The project area for a mining project interest is so much of the area covered by a *production right as is:

(a) for a mining project interest arising under subsection 15‑5(1)—the area to which the *mining venture mentioned in that subsection relates; or

(b) for a mining project interest arising under subsection 15‑5(4)—the area to which the entitlement giving rise to the mining project interest relates.

Note: The project area for a mining project interest may also be, or be part of, the project area for another mining project interest.

20‑1 What this Division is about

The concept of a taxable resource is central to whether an entity has a mining project interest, and to the other concepts (such as mining profits) that govern an entity’s MRRT liabilities.

Table of sections

Operative provisions

20‑5 What are taxable resources

20‑5 What are taxable resources

(1) A taxable resource is a quantity of any of the following:

(a) iron ore;

(b) coal;

(c) anything produced from a process that results in iron ore or coal being consumed or destroyed without extraction;

(d) coal seam gas extracted as a necessary incident of mining coal.

Example: Gas extracted on an ongoing basis from a coal mine, or a proposed coal mine (if it is not extracted as part of a separate commercial operation) in order to comply with engineering requirements, mine safety laws or environmental conditions would be a taxable resource because its extraction is a necessary incident of mining the coal.

Gas extracted before coal mining begins as part of an independent commercial operation would not be a taxable resource because its extraction would not be a necessary incident of coal mining. Instead, that gas would be subject to taxation under the Petroleum Resource Rent Tax Assessment Act 1987.

(2) In deciding whether something is a taxable resource, disregard:

(a) the use to which it is or will be put; and

(b) what is or will be produced from it after extraction.

(3) A quantity of a thing may be a taxable resource even if its extent is not known (for example, before it is extracted).

25‑1 What this Division is about

A miner’s mining profit is a component of its MRRT liability for a mining project interest for an MRRT year. It is the excess of mining revenue over mining expenditure for the interest for the year.

Table of sections

Operative provisions

25‑5 How to work out the mining profit for a mining project interest

25‑5 How to work out the mining profit for a mining project interest

Work out a miner’s mining profit for a mining project interest for an *MRRT year as follows:

Method statement

Step 1. Work out the miner’s *mining revenue for the mining project interest for the *MRRT year.

Note: For the mining revenue, see Division 30.

Step 2. Work out the miner’s *mining expenditure for the mining project interest for the *MRRT year.

Note: For the mining expenditure, see Division 35.

Step 3. If the *mining revenue exceeds the *mining expenditure, the difference is the miner’s mining profit for the mining project interest for the *MRRT year.

Step 4. If the *mining revenue does not exceed the *mining expenditure, the miner’s mining profit for the mining project interest for the *MRRT year is zero.

Note: Mining expenditure that exceeds mining revenue is a mining loss that may be applied in working out a mining loss allowance (see Part 3‑4) or a transferred mining loss allowance (see Part 3‑7).

Table of Subdivisions

Guide to Division 30

30‑A A miner’s mining revenue

30‑B Revenue from supply, export or use of taxable resources

30‑C Other revenue

30‑D Miscellaneous

30‑1 What this Division is about

A miner’s mining revenue for a mining project interest may consist of revenue from:

(a) taxable resources extracted from the project area for the mining project interest, to the extent that the revenue is reasonably attributable to the taxable resources in the form and place they were in when they were at their valuation point; and

(b) recoupment of mining expenditure relating to the mining project interest; and

(c) compensation for loss of taxable resources for the mining project interest; and

(d) amounts for supply of taxable resources if the amounts are not attributable to particular taxable resources.

Subdivision 30‑A—A miner’s mining revenue

Table of sections

30‑5 A miner’s mining revenue

A miner’s mining revenue for a mining project interest that the miner has, for an *MRRT year, is the sum of all the amounts that, under this Act, are included in the miner’s mining revenue for that interest for that year.

Note: Most of the amounts are covered by this Division. However, the following amounts may also be included in a miner’s mining revenue:

(a) amounts that are in effect recoupment of the value of starting base assets (see section 90‑65);

(b) amounts arising as a result of adjustments to take account of changes in circumstances (see Division 160);

(c) amounts arising as a result of balancing adjustment events for starting base assets (see Division 165).

Subdivision 30‑B—Revenue from supply, export or use of taxable resources

Table of sections

30‑10 When amounts from taxable resources etc. are included in mining revenue

30‑15 Meaning of mining revenue event

30‑20 Meaning of initial supply

30‑25 Working out amounts to be included

30‑30 Meaning of arm’s length consideration

30‑35 When supplies are made

30‑10 When amounts from taxable resources etc. are included in mining revenue

An amount is included in a miner’s mining revenue for a mining project interest for an *MRRT year if:

(a) a *taxable resource has been extracted from the *project area for the mining project interest; and

(b) during the year, a *mining revenue event happens in relation to the taxable resource.

30‑15 Meaning of mining revenue event

(1) A mining revenue event happens in relation to a *taxable resource extracted from the *project area for a mining project interest if the miner who has the interest:

(a) makes an *initial supply of the taxable resource, but not after its exportation from *Australia; or

(b) exports the taxable resource from Australia, but not after paragraph (a) has applied to the taxable resource; or

(c) makes an initial supply of or uses, or exports from Australia, something produced using the taxable resource, but not after paragraph (a) or (b), or this paragraph, has already applied in relation to the taxable resource.

Note: There is a mining revenue event (but only one) in relation to each quantity of taxable resource.

(2) However, a mining revenue event does not happen for use of a thing produced using a *taxable resource, to the extent that:

(a) the use takes place in the course of operations or activities of a kind mentioned in paragraph 35‑20(1)(a) for the mining project interest; and

(b) those operations or activities do not involve doing anything to, or with, other taxable resources extracted from the *project area for the interest after those other taxable resources reach the form and location they are in when a mining revenue event happens in relation to them; and

(c) the use does not give rise to:

(i) an amount of *mining expenditure for the miner; or

(ii) an amount that is taken into account for the miner under step 2 of the method statement in section 30‑25; or

(iii) an amount that is taken into account for the miner under step 3 of the method statement in section 175‑25 (alternative valuation method).

30‑20 Meaning of initial supply

(1) An initial supply of a *taxable resource, or something produced using a taxable resource, is the first *supply of the taxable resource or thing a miner makes, disregarding a supply covered by subsection (2).

(2) However, a *supply of a *taxable resource, or something produced using such a taxable resource, is not an initial supply if:

(a) the supply is made between *entities in the course of a *mining venture in relation to which each of the entities has a mining project interest; or

(b) the supply does not result in a change in the ownership of the taxable resource or the thing produced using such a taxable resource.

30‑25 Working out amounts to be included

(1) Work out the amount to be included under section 30‑10, in relation to a *mining revenue event that happens in relation to a *taxable resource, as follows:

Method statement

Step 1. Work out under subsection (2) the revenue amount for the *mining revenue event.

Step 2. Using the method that satisfies subsection (3), work out how much of that revenue amount is reasonably attributable to the *taxable resource:

(a) in the form in which it existed when it was at its *valuation point; and

(b) at the place where it was located when it was at its valuation point.

The amount worked out under this step is the amount to be included under section 30‑10.

Revenue amount

(2) The revenue amount mentioned in step 1 of the method statement in subsection (1) is:

Working out the revenue amount | ||

Item | Column 1 | Column 2 |

1 | A *supply of the *taxable resource, or a thing produced using the taxable resource | The consideration received or receivable for the supply |

2 | An exportation from *Australia of the *taxable resource, or a thing produced using the taxable resource | What would be the *arm’s length consideration for a *supply of the taxable resource or thing at the time and place the taxable resource or thing is loaded for export |

3 | Use of a thing produced from the *taxable resource | What would be the *arm’s length consideration for a *supply of the thing at the time and place of the use. |

Note: Supplies covered by item 1 of the table that are not at arm’s length may, in appropriate cases, attract the operation of Division 205 (anti‑profit shifting).

(3) The method to use in step 2 of the method statement in subsection (1) is the one that produces the most appropriate and reliable measure of how much of the revenue amount is reasonably attributable as mentioned in that step, having regard to:

(a) the miner’s circumstances, including, but not limited to, the functions performed, assets used, and risks borne by the miner in carrying on its *mining operations, *transformative operations and *resource marketing operations for the mining project interest; and

(b) the available information.

(4) In using the method that satisfies subsection (3), make the following assumptions, to the extent that they are relevant to that method:

(a) that a distinct and separate *entity (the notional downstream entity) does all the things (including using all the assets) that the miner actually does in carrying on the *downstream mining operations, *transformative operations and *resource marketing operations for the mining project interest;

(b) that the notional downstream entity does not acquire an interest in the *taxable resource;

(c) that the miner and the notional downstream entity deal wholly independently with one another;

(d) that:

(i) there is a market for what the notional downstream entity is assumed by paragraph (a) to do; and

(ii) that market is competitive in the sense that the returns to the notional downstream entity would be no more or less than are necessary for it to commit capital, and in particular are commensurate with the non‑diversifiable risks inherent in the things it does.

(5) Without limiting subsection (3), a miner is taken for the purposes of step 2 in the method statement in subsection (1) to use the method that satisfies subsection (3) if the miner works out how much of the revenue amount is reasonably attributable as mentioned in that step by:

(a) reducing the revenue amount by an amount that, having regard to the matters mentioned in paragraphs (3)(a) and (b), is sufficient for a notional downstream entity to recover the following costs relating to what it is assumed by subsection (4) to do:

(i) any operating costs;

(ii) any depreciation of the assets that the notional downstream entity is taken to have used;

(iii) a cost of capital sufficient to justify the continued commitment of the capital; and

(b) adding back to the revenue amount so much (if any) of the costs mentioned in paragraph (a) of this subsection as relate to things done to the extent that they were not taken into account in the revenue amount.

However, the costs mentioned in paragraph (a) of this subsection only include costs to the extent that they reasonably relate to the *taxable resource in relation to which the *mining revenue event happens.

Meaning of transformative operations

(6) Operations or activities are transformative operations, for a mining project interest, to the extent that the operations or activities:

(a) are operations or activities of a kind mentioned in paragraph 35‑20(1)(a) for the mining project interest; and

(b) involve doing something to, or with, the *taxable resources after they reach the form and location they are in when they are first applied to producing something in relation to which a *mining revenue event of a kind mentioned in paragraph 30‑15(1)(c) happens; and

(c) do not involve doing anything to, or with, those taxable resources after they reach the form and location they are in when that mining revenue event happens.

Meaning of resource marketing operations

(7) Operations or activities are resource marketing operations, for a mining project interest, to the extent that the operations or activities involve marketing, selling, shipping or delivering of *taxable resources in relation to which a *mining revenue event happens.

30‑30 Meaning of arm’s length consideration

(1) The arm’s length consideration for a *supply is the amount that would reasonably be expected to be received or receivable by the miner as consideration for the supply if:

(a) the miner made the supply under an agreement between the miner and another *entity; and

(b) they were dealing wholly independently with one another in relation to the supply.

(2) The method used to determine that amount is to be the method that produces the most appropriate and reliable measure of that amount having regard to:

(a) the miner’s circumstances, including, but not limited to, the functions performed, assets used, and risks borne by the miner in carrying on its *mining operations, *transformative operations and *resource marketing operations for the mining project interest; and

(b) the available information.

(3) However, if it is not possible to work out the arm’s length consideration in accordance with subsections (1) and (2), the arm’s length consideration for a *supply is the amount that is, in the Commissioner’s opinion, fair and reasonable.

Treat the time when a miner makes a *supply for the purposes of this Act as the earliest of the following:

(a) when consideration for the supply is received or becomes receivable;

(b) when what is being supplied is delivered;

(c) when ownership of what is being supplied passes.

Subdivision 30‑C—Other revenue

Table of sections

30‑40 Recoupment or offsetting of mining expenditure

30‑45 Recoupment of payments that give rise to royalty credits

30‑50 Compensation for loss of taxable resources

30‑55 Amounts that do not relate to a particular mining revenue event

30‑40 Recoupment or offsetting of mining expenditure

(1) An amount is included in a miner’s *mining revenue for a mining project interest for an *MRRT year to the extent that:

(a) during the year, the amount is received, or becomes receivable, by any of the following *entities:

(i) the miner;

(ii) an entity *connected with the miner;

(iii) an *affiliate of the miner;

(iv) an entity of which the miner is an affiliate;

(v) an affiliate of an entity covered by subparagraph (ii);

(vi) an entity connected with an entity covered by subparagraph (ii), (iii) or (iv); and

(b) payment of the amount has, or would have, the purpose or effect of *recouping or offsetting some or all of an amount of expenditure (including future expenditure); and

(c) the amount does not give rise to an adjustment under Division 160 (adjustments for changes in circumstances).

Example: In the 2012‑13 MRRT year, a miner receives a subsidy for employing apprentices. In the 2013‑14 MRRT year, the miner incurs mining expenditure for the relevant mining project interest in the form of wages paid to the apprentices.

To the extent that the subsidy offsets those wages, it is included in the miner’s mining revenue for the mining project interest for the 2012‑13 MRRT year.

(2) However, that amount is reduced (if necessary) to reflect the proportion of the amount of expenditure mentioned in paragraph (1)(b) that is, or will be, included in *mining expenditure for the mining project interest.

30‑45 Recoupment of payments that give rise to royalty credits

An amount is included in a miner’s *mining revenue for a mining project interest for an *MRRT year if the amount is an excess royalty recoupment mentioned in subsection 60‑30(2) for the interest.

Note: Royalty recoupments are generally applied to reduce royalty credits under section 60‑30. However, if there are insufficient royalty credits the excess is mining revenue under this section.

30‑50 Compensation for loss of taxable resources

(1) An amount is included in a miner’s *mining revenue for a mining project interest for an *MRRT year to the extent that:

(a) during the year, the amount is received, or becomes receivable, by any of the following *entities:

(i) the miner;

(ii) an entity *connected with the miner;

(iii) an *affiliate of the miner;

(iv) an entity of which the miner is an affiliate;

(v) an affiliate of an entity covered by subparagraph (ii);

(vi) an entity connected with an entity covered by subparagraph (ii), (iii) or (iv); and

(b) the amount is by way of insurance, compensation or indemnity relating to loss of, destruction of or damage that:

(i) happens to a *taxable resource extracted from the *project area for the mining project interest, or to a thing produced using such a taxable resource; and

(ii) happens before a *mining revenue event happens in relation to the taxable resource; and

(c) the amount is reasonably attributable to the taxable resource, as mentioned in step 2 of the method statement in subsection 30‑25(1).

(2) Work out the extent to which the amount is reasonably attributable to the *taxable resource as so mentioned by applying section 30‑25 as if the amount were a revenue amount under subsection 30‑25(2).

30‑55 Amounts that do not relate to a particular mining revenue event

An amount is included in a miner’s *mining revenue for a mining project interest for an *MRRT year to the extent that:

(a) during the year, the amount is received, or becomes receivable, by the miner; and

(b) the amount is received, or becomes receivable, for a *supply, or a proposed supply, of *taxable resources; and

(c) the amount does not relate to a particular *mining revenue event.

Subdivision 30‑D—Miscellaneous

Table of sections

30‑60 No double counting

30‑65 Expenditure incurred in causing amounts to be received etc.

30‑70 Amounts taken to be received

30‑75 GST and increasing adjustments

If 2 or more provisions of this Act include the same amount in a miner’s *mining revenue (whether for the same *MRRT year or different MRRT years), the amount is included only under the provision that is most appropriate.

30‑65 Expenditure incurred in causing amounts to be received etc.

An amount that, under Subdivision 30‑B or 30‑C, is to be included in a miner’s *mining revenue for a mining project interest for an *MRRT year is reduced to the extent that:

(a) the miner necessarily incurred any expenditure in enforcing the miner’s entitlement to receive the amount; and

(b) the expenditure does not relate to any other amount; and

(c) the expenditure was not *mining expenditure for the mining project interest; and

(d) the expenditure was not *excluded expenditure.

Note: This section ensures that the costs associated with mining revenue, but not dealt with under Division 35, are taken into account.

Example: If a miner undertakes litigation to receive compensation for damage to the miner’s taxable resources, the amount included in the miner’s mining revenue under section 30‑50 would be reduced under this section to take account of the miner’s litigation costs.

30‑70 Amounts taken to be received

For the purposes of the *MRRT law, an amount that is not actually to be paid over to a miner is taken to be received by the miner if it is, and when it is, applied or otherwise dealt with on behalf of the miner or as the miner directs.

30‑75 GST and increasing adjustments

An amount that, under this Division, is to be included in the miner’s *mining revenue does not include:

(a) any *GST payable on a *supply for which the amount is the consideration, or part of the consideration; or

(b) any *increasing adjustments that relate to such a supply.

Division 35—Mining expenditure

Table of Subdivisions

Guide to Division 35

35‑A A miner’s mining expenditure

35‑B Excluded expenditure

35‑1 What this Division is about

A miner’s mining expenditure for a mining project interest includes expenditure necessarily incurred in carrying on mining operations upstream of the valuation point.

However, some expenditure is specifically excluded.

Note: For pre‑mining expenditure, see section 70‑35.

Subdivision 35‑A—A miner’s mining expenditure

Table of sections

35‑5 A miner’s mining expenditure

35‑10 General expenditure

35‑15 Meaning of upstream mining operations

35‑20 Meaning of mining operations

35‑25 No double counting

35‑5 A miner’s mining expenditure

(1) A miner’s mining expenditure for a mining project interest that the miner has, for an *MRRT year, is the sum of all the amounts that, under this Act, are included in the miner’s mining expenditure for that interest for that year.

Note: Most of the amounts are covered by this Division. However, amounts arising as a result of adjustments to take account of changes in circumstances may also be included in a miner’s mining expenditure (see Division 160).

(2) However, an amount is not included in the miner’s mining expenditure for the mining project interest for the *MRRT year to the extent that it is *excluded expenditure.

Note: For excluded expenditure, see Subdivision 35‑B.

(1) An amount of expenditure is included in a miner’s *mining expenditure for a mining project interest for an *MRRT year to the extent that the miner necessarily incurred the amount, in that year, in the carrying on (by the miner or another *entity) of *upstream mining operations for the mining project interest.

(2) The expenditure may be of either a capital or revenue nature.

35‑15 Meaning of upstream mining operations

*Mining operations for a mining project interest are upstream mining operations for the mining project interest to the extent the operations:

(a) are operations or activities of a kind mentioned in paragraph 35‑20(1)(a) for the mining project interest; and

(b) do not involve doing anything to, or with, the *taxable resources extracted from the *project area for the mining project interest after those taxable resources reach their *valuation point.

Examples: The following are some examples of operations or activities that might be upstream mining operations:

(a) obtaining the agreement of native title holders as part of the process of obtaining a production right over the project area;

(b) exploring for taxable resources in the project area;

(c) crushing and weighing the taxable resources before they reach their valuation point;

(d) training, engaging, employing, paying, accommodating and ensuring the safety of personnel, and other supportive head office activities, to the extent they are involved in operations or activities relating to getting the taxable resource to the valuation point;

(e) developing plans and engineering specifications for, and constructing, facilities (whether in the project area or not) to be used in recovering, transporting and storing the taxable resources before they reach their valuation point;

(f) acquiring and maintaining plant or equipment for use in recovering, transporting or storing the taxable resources before they reach their valuation point;

(g) upgrading computer software used to control inventory (like consumables and spare parts) used for recovering, transporting or storing the taxable resources before they reach their valuation point;

(h) rehabilitation of a project area from damage caused by activities relating to the exploration, extraction and movement of taxable resources to the valuation point.

Note: For downstream mining operations, see section 255‑15.

35‑20 Meaning of mining operations

(1) Operations or activities are mining operations, for a mining project interest, to the extent that the operations or activities:

(a) are preliminary or integral to, or consequential upon:

(i) extracting or producing *taxable resources from the *project area for the mining project interest; or

(ii) producing something using those taxable resources; but

(b) do not involve doing anything to, or with, those taxable resources after they reach the form and location they are in when:

(i) a *mining revenue event of a kind mentioned in paragraph 30‑15(1)(a) or (b) happens in relation to them; or

(ii) they are first applied to producing something in relation to which a mining revenue event of a kind mentioned in paragraph 30‑15(1)(c) happens.

(2) Without limiting subsection (1), the following activities are mining operations for a mining project interest:

(a) *exploration or prospecting for *taxable resources in the *project area for the mining project interest;

(b) extracting taxable resources from the project area;

(c) doing anything to, or with, taxable resources extracted or produced from the project area before they reach the form and location they are in when a *mining revenue event happens in relation to them;

(d) obtaining access to the project area for any of the other activities mentioned in this subsection (other than paragraph (h));

(e) acquiring, constructing or maintaining anything to be used, or reasonably expected to be used, for any of the activities mentioned in any of paragraphs (a) to (d) (even if no such activity is happening at the time the acquisition, construction or maintenance happens);

(f) rehabilitating the project area, or any other land affected by any activity mentioned in any of paragraphs (a) to (e);

(g) closing down any activity mentioned in any of paragraphs (a) to (f);

(h) any activity done in furtherance of an activity mentioned in any of paragraphs (a) to (g).

If 2 or more provisions of this Act include the same amount in a miner’s *mining expenditure (whether for the same *MRRT year or a different MRRT year), the amount is included only under the provision that is most appropriate.

Subdivision 35‑B—Excluded expenditure

Table of sections

35‑35 Cost of acquiring rights and interests in projects

35‑40 Royalties

35‑45 Meanings of mining royalty and private mining royalty

35‑50 Financing costs

35‑55 Hire purchase agreements

35‑60 Non‑adjacent land and buildings used in administrative or accounting activities

35‑65 Hedging or foreign exchange arrangements

35‑70 Rehabilitation bond and trust payments

35‑75 Payments of income tax or GST

35‑35 Cost of acquiring rights and interests in projects

(1) An amount of expenditure is excluded expenditure to the extent that it relates to acquiring, or acquiring an interest in, a *production right covering an area, unless the expenditure is in relation to the grant of the production right.

(2) An amount of expenditure is excluded expenditure to the extent that it relates to acquiring a mining project interest.

(3) An amount of expenditure is excluded expenditure to the extent that it relates to acquiring an interest in profits, receipts or expenditures of, or relating to, a mining project interest.

(1) An amount of expenditure is excluded expenditure to the extent that it is any of the following:

(a) a *mining royalty;

(b) a *private mining royalty;

(c) a payment that gives rise to a *royalty credit under paragraph 60‑20(1)(b) (payments by way of recoupment for mining royalties).

(2) Despite subsection (1), a *private mining royalty is not excluded expenditure, to the extent that:

(a) it is paid to an *entity as consideration for the entity performing services that form part of *upstream mining operations for a mining project interest; and

(b) it does not represent a share of the profits made from a *mining venture relating to the mining project interest.

(3) Despite subsection (1), a *private mining royalty is not excluded expenditure to the extent that it is paid to an entity under an agreement entered into with the entity:

(a) before 2 May 2010; and

(b) at a time when the entity is an STB (within the meaning of Division 1AB of Part III of the Income Tax Assessment Act 1936) other than an *excluded STB.

(4) Despite subsection (1), a *private mining royalty is not excluded expenditure, to the extent that it is by way of consideration for the carrying on of *mining operations in the *project area for a mining project interest, if it is paid:

(a) to a native title holder (within the meaning of the Native Title Act 1993) whose approved determination of native title (within the meaning of that Act) relates to the project area for the mining project interest; or

(b) to a registered native title claimant (within the meaning of the Native Title Act 1993) whose claimant application (within the meaning of that Act) relates to the project area for the mining project interest; or

(c) to a person who holds a right that:

(i) arises under another *Australian law dealing with the rights of *Aboriginal persons or *Torres Strait Islanders in relation to land or waters; and

(ii) relates to the project area for the mining project interest.

(5) To the extent a *private mining royalty is not *excluded expenditure because of subsection (3) or (4), it is not excluded expenditure under section 35‑35.

35‑45 Meanings of mining royalty and private mining royalty

(1) An amount of expenditure is a mining royalty to the extent the expenditure:

(a) is made in relation to a *taxable resource extracted under authority of a *production right; and

(b) is made under a *Commonwealth law, a *State law or a *Territory law; and

(c) either:

(i) is a *royalty; or

(ii) would be a royalty, if the taxable resource were owned by the Commonwealth, State or Territory (as the case requires) just before the recovery of the resource.

Note: Subparagraph (1)(c)(ii) covers a case where an amount is payable under an Australian law in relation to minerals owned by private landowners.

(2) An amount of expenditure is a private mining royalty if:

(a) it is:

(i) a *taxable resource or a quantity of something produced using a taxable resource; or

(ii) calculated by reference to a taxable resource or a quantity of something produced using a taxable resource; or

(iii) calculated by reference to the gross or net value of a taxable resource or something produced using a taxable resource; or

(iv) calculated by reference to the revenue, expenditure or profits made or incurred by an *entity in relation to a taxable resource or a quantity of something produced using a taxable resource; and

(b) it is not a *mining royalty.

An amount of expenditure is excluded expenditure to the extent that it relates to:

(a) an *arrangement that gives rise to a *financial arrangement; or

(b) an *equity interest that is a financial arrangement; or

(c) a *scheme that gives rise to an equity interest issued by the miner.

Examples:

(a) borrowing costs, exit fees or interest payments relating to a loan, or repayments of principal; and

(b) payments of dividends or payments for buying back or cancelling shares.

35‑55 Hire purchase agreements

(1) An amount of expenditure is excluded expenditure to the extent that it relates to a *hire purchase agreement.

(2) However, if an amount of expenditure is excluded expenditure for a miner under subsection (1) in relation to a *hire purchase agreement:

(a) the miner is taken to have incurred the amount mentioned in subsection (3) at the earliest time at which the property is *supplied to the miner under the agreement; and

(b) the miner is taken to have acquired the property for that amount at the time the amount is incurred; and

(c) the amount is not excluded expenditure under subsection (1) or section 35‑50.

(3) For the purposes of paragraph (2)(a), the amount is:

(a) if an amount is stated to be the cost or value of the property for the purposes of the agreement, and the miner and the hirer were dealing with each other at *arm’s length in connection with the agreement—the amount so stated; or

(b) otherwise—the amount that could reasonably have been expected to have been paid by the miner for the purchase of the property if:

(i) the hirer had actually sold the property to the miner at the start of the agreement; and

(ii) the hirer and the miner were dealing with each other at arm’s length in connection with the sale.

Note: The amount may be mining expenditure under this Division.

35‑60 Non‑adjacent land and buildings used in administrative or accounting activities

An amount of expenditure is excluded expenditure to the extent that:

(a) it relates to land or buildings that are not located at or adjacent to the *project area for a mining project interest that the miner has; and

(b) the land or buildings are for use in connection with administrative or accounting activities; and