Income Tax Assessment Act 1997

No. 38, 1997

Compilation No. 217

Compilation date: 12 December 2020

Includes amendments up to: Act No. 118, 2020

Registered: 22 December 2020

This compilation is in 12 volumes

Volume 1: sections 1‑1 to 36‑55

Volume 2: sections 40‑1 to 67‑30

Volume 3: sections 70‑1 to 121‑35

Volume 4: sections 122‑1 to 197‑85

Volume 5: sections 200‑1 to 253‑15

Volume 6: sections 275‑1 to 313‑85

Volume 7: sections 315‑1 to 420‑70

Volume 8: sections 615‑1 to 721‑40

Volume 9: sections 723‑1 to 880‑205

Volume 10: sections 900‑1 to 995‑1

Volume 11: Endnotes 1 to 3

Volume 12: Endnote 4

Each volume has its own contents

About this compilation

This compilation

This is a compilation of the Income Tax Assessment Act 1997 that shows the text of the law as amended and in force on 12 December 2020 (the compilation date).

The notes at the end of this compilation (the endnotes) include information about amending laws and the amendment history of provisions of the compiled law.

Uncommenced amendments

The effect of uncommenced amendments is not shown in the text of the compiled law. Any uncommenced amendments affecting the law are accessible on the Legislation Register (www.legislation.gov.au). The details of amendments made up to, but not commenced at, the compilation date are underlined in the endnotes. For more information on any uncommenced amendments, see the series page on the Legislation Register for the compiled law.

Application, saving and transitional provisions for provisions and amendments

If the operation of a provision or amendment of the compiled law is affected by an application, saving or transitional provision that is not included in this compilation, details are included in the endnotes.

Editorial changes

For more information about any editorial changes made in this compilation, see the endnotes.

Modifications

If the compiled law is modified by another law, the compiled law operates as modified but the modification does not amend the text of the law. Accordingly, this compilation does not show the text of the compiled law as modified. For more information on any modifications, see the series page on the Legislation Register for the compiled law.

Self‑repealing provisions

If a provision of the compiled law has been repealed in accordance with a provision of the law, details are included in the endnotes.

Contents

Chapter 3—Specialist liability rules

Part 3‑80—Roll‑overs applying to assets generally

Division 615—Roll‑overs for business restructures

Guide to Division 615 1

615‑1 What this Division is about

Subdivision 615‑A—Choosing to obtain roll‑overs

615‑5 Disposing of interests in one entity for shares in a company

615‑10 Redeeming or cancelling interests in one entity for shares in a company

Subdivision 615‑B—Further requirements for choosing to obtain roll‑overs

615‑15 Interposed company must own all the original interests

615‑20 Requirements relating to your interests in the original entity

615‑25 Requirements relating to the interposed company

615‑30 Interposed company must make a particular choice

615‑35 ADI restructures—disregard certain preference shares

Subdivision 615‑C—Consequences of roll‑overs

615‑40 CGT consequences

615‑45 Additional consequences—deferral of profit or loss

615‑50 Trading stock

615‑55 Revenue assets

615‑60 Disregard CGT exemption for trading stock

Subdivision 615‑D—Consequences for the interposed company

615‑65 Consequences for the interposed company

Division 620—Assets of wound‑up corporation passing to corporation with not significantly different ownership

Subdivision 620‑A—Corporations covered by Subdivision 124‑I

Guide to Subdivision 620‑A

620‑5 What this Subdivision is about

Application and object of this Subdivision

620‑10 Application

620‑15 Object

CGT consequences

620‑20 Disregard body’s capital gains and losses from CGT assets

620‑25 Cost base and pre‑CGT status of CGT asset for company

Consequences for depreciating assets

620‑30 Roll‑over relief for balancing adjustment events

Consequences for trading stock

620‑40 Body taken to have sold trading stock to company

Consequences for revenue assets

620‑50 Body taken to have sold revenue assets to company

Part 3‑90—Consolidated groups

Division 700—Guide and objects

Guide

700‑1 What this Part is about

700‑5 Overview of this Part

Objects

700‑10 Objects of this Part

Division 701—Core rules

Common rule

701‑1 Single entity rule

Head company rules

701‑5 Entry history rule

701‑10 Cost to head company of assets of joining entity

701‑15 Cost to head company of membership interests in entity that leaves group

701‑20 Cost to head company of assets consisting of certain liabilities owed by entity that leaves group

701‑25 Tax‑neutral consequence for head company of ceasing to hold assets when entity leaves group

Entity rules

701‑30 Where entity not subsidiary member for whole of income year

701‑35 Tax‑neutral consequence for entity of ceasing to hold assets when it joins group

701‑40 Exit history rule

701‑45 Cost of assets consisting of liabilities owed to entity by members of the group

701‑50 Cost of certain membership interests of which entity becomes holder on leaving group

Supporting provisions

701‑55 Setting the tax cost of an asset

701‑56 Application of subsection 701‑55(6)

701‑58 Effect of setting the tax cost of an asset that the head company does not hold under the single entity rule

701‑60 Tax cost setting amount

701‑60A Tax cost setting amount for asset emerging when entity leaves group

701‑61 Assets in relation to Division 230 financial arrangement—head company’s assessable income or deduction

701‑63 Right to future income and WIP amount asset

701‑65 Net income and losses for trusts and partnerships

701‑67 Assets in this Part are CGT assets, etc.

Exceptions

701‑70 Adjustments to taxable income where identities of parties to arrangement merge on joining group

701‑75 Adjustments to taxable income where identities of parties to arrangement re‑emerge on leaving group

701‑80 Accelerated depreciation

701‑85 Other exceptions etc. to the rules

Division 703—Consolidated groups and their members

Guide to Division 703 54

703‑1 What this Division is about

Basic concepts

703‑5 What is a consolidated group?

703‑10 What is a consolidatable group?

703‑15 Members of a consolidated group or consolidatable group

703‑20 Certain entities that cannot be members of a consolidated group or consolidatable group

703‑25 Australian residence requirements for trusts

703‑30 When is one entity a wholly‑owned subsidiary of another?

703‑33 Transfer time for sale of shares in company

703‑35 Treating entities as wholly‑owned subsidiaries by disregarding employee shares

703‑37 Disregarding certain preference shares following an ADI restructure

703‑40 Treating entities held through non‑fixed trusts as wholly‑owned subsidiaries

703‑45 Subsidiary members or nominees interposed between the head company and a subsidiary member of a consolidated group or a consolidatable group

Choice to consolidate a consolidatable group

703‑50 Choice to consolidate a consolidatable group

Consolidated group created when MEC group ceases to exist

703‑55 Creating consolidated groups from certain MEC groups

Notice of events affecting consolidated group

703‑58 Notice of choice to consolidate

703‑60 Notice of events affecting consolidated group

Effects of choice to continue group after shelf company becomes new head company

703‑65 Application

703‑70 Consolidated group continues in existence with interposed company as head company and original entity as a subsidiary member

703‑75 Interposed company treated as substituted for original entity at all times before the completion time

703‑80 Effects on the original entity’s tax position

Division 705—Tax cost setting amount for assets where entities become subsidiary members of consolidated groups

Guide to Division 705 75

705‑1 What this Division is about

Subdivision 705‑A—Basic case: a single entity joining an existing consolidated group

Guide to Subdivision 705‑A

705‑5 What this Subdivision is about

Application and object

705‑10 Application and object of this Subdivision

705‑15 Cases where this Subdivision does not have effect

Tax cost setting amount for assets that joining entity brings into joined group

705‑20 Tax cost setting amount worked out under this Subdivision

705‑25 Tax cost setting amount for retained cost base assets

705‑27 Reduction in tax cost setting amount that exceeds market value of certain retained cost base assets

705‑30 What is the joining entity’s terminating value for an asset?

705‑35 Tax cost setting amount for reset cost base assets

705‑40 Tax cost setting amount for reset cost base assets held on revenue account etc.

705‑45 Reduction in tax cost setting amount for accelerated depreciation assets

705‑47 Reduction in tax cost setting amount for some privatised assets

705‑55 Order of application of sections 705‑40, 705‑45 and 705‑47

705‑56 Modification for tax cost setting in relation to finance leases

705‑57 Adjustment to tax cost setting amount where loss of pre‑CGT status of membership interests in joining entity

705‑58 Assets and liabilities not set off against each other

705‑59 Exception: treatment of linked assets and liabilities

How to work out the allocable cost amount

705‑60 What is the joined group’s allocable cost amount for the joining entity?

705‑62 No double counting of amounts in allocable cost amount

705‑65 Cost of membership interests in the joining entity—step 1 in working out allocable cost amount

705‑70 Liabilities of the joining entity—step 2 in working out allocable cost amount

705‑75 Liabilities of the joining entity—reductions for purposes of step 2 in working out allocable cost amount

705‑76 Liability arising from transfer or assignment of securitised assets

705‑80 Liabilities of the joining entity—reductions/increases for purposes of step 2 in working out allocable cost amount

705‑85 Liabilities of the joining entity—increases for purposes of step 2 in working out allocable cost amount

705‑90 Undistributed, taxed profits accruing to joined group before joining time—step 3 in working out allocable cost amount

705‑93 If pre‑joining time roll‑over from foreign resident company or head company—step 3A in working out allocable cost amount

705‑95 Pre‑joining time distributions out of certain profits—step 4 in working out allocable cost amount

705‑100 Losses accruing to joined group before joining time—step 5 in working out allocable cost amount

705‑105 Continuity of holding membership interests—steps 3 to 5 in working out allocable cost amount

705‑110 If joining entity transfers a loss to the head company—step 6 in working out allocable cost amount

705‑115 If head company becomes entitled to certain deductions—step 7 in working out allocable cost amount

How to work out a pre‑CGT factor for assets of joining entity

705‑125 Pre‑CGT proportion for joining entity

Subdivision 705‑B—Case of group formation

Guide to Subdivision 705‑B

705‑130 What this Subdivision is about

Application and object

705‑135 Application and object of this Subdivision

Modified application of Subdivision 705‑A

705‑140 Subdivision 705‑A has effect with modifications

705‑145 Order in which tax cost setting amounts are to be worked out where subsidiary members have membership interests in other subsidiary members

705‑147 Adjustment in working out step 3A of allocable cost amount to take account of membership interests held by subsidiary members in other such members

705‑155 Adjustments to restrict step 4 reduction of allocable cost amount to effective distributions to head company in respect of direct membership interests

705‑160 Adjustment to allocation of allocable cost amount to take account of owned profits or losses of certain entities that become subsidiary members

705‑163 Modified application of section 705‑57

Subdivision 705‑C—Case where a consolidated group is acquired by another

Guide to Subdivision 705‑C

705‑170 What this Subdivision is about

Application and object

705‑175 Application and object of this Subdivision

Modified application of Division 701 in relation to acquired group etc.

705‑180 Modifications of Division 701

Modified application of Subdivision 705‑A in relation to acquiring group

705‑185 Subdivision 705‑A has effect with modifications

Modifications of Subdivision 705‑A for the purposes of this Subdivision

705‑195 Modified application of subsection 705‑65(6)

705‑200 Modified application of section 705‑85

Subdivision 705‑D—Where multiple entities are linked by membership interests

Guide to Subdivision 705‑D

705‑210 What this Subdivision is about

Application and object

705‑215 Application and object of this Subdivision

Modified application of Subdivision 705‑A

705‑220 Subdivision 705‑A has effect with modifications

705‑225 Order in which tax cost setting amounts are to be worked out where linked entities have membership interests in other linked entities

705‑227 Adjustment in working out step 3A of allocable cost amount to take account of membership interests held by linked entities in other linked entities

705‑230 Adjustments to restrict step 4 reduction of allocable cost amount to effective distributions to head company in respect of direct membership interests

705‑235 Adjustment to allocation of allocable cost amount to take account of owned profits or losses of certain linked entities

705‑240 Modified application of section 705‑57

Subdivision 705‑E—Adjustments for errors etc.

Guide to Subdivision 705‑E

705‑300 What this Subdivision is about

Operative provisions

705‑305 Object of this Subdivision

705‑310 Operation of Part IVA of the Income Tax Assessment Act 1936

705‑315 Errors that attract special adjustment action

705‑320 Tax cost setting amounts taken to be correct

Division 707—Losses for head companies when entities become members etc.

Subdivision 707‑A—Transfer of losses to head company

Guide to Subdivision 707‑A

707‑100 What this Subdivision is about

707‑105 Who can utilise the loss?

Objects

707‑110 Objects of this Subdivision

Application

707‑115 What losses this Subdivision applies to

Transfer of loss from joining entity to head company

707‑120 Transfer of loss from joining entity to head company

707‑125 Modified business continuity test for companies’ post‑1999 losses

707‑130 Modified pattern of distributions test

707‑135 Transferring loss transferred to joining entity because business continuity test was satisfied

Effect of transfer of loss

707‑140 Effect of transfer of loss

Cancelling the transfer of the loss

707‑145 Cancelling the transfer of the loss

What happens if the loss is not transferred?

707‑150 Loss cannot be utilised for income year ending after the joining time

Subdivision 707‑B—Can a transferred loss be utilised?

Guide to Subdivision 707‑B

707‑200 What this Subdivision is about

Operative provisions

707‑205 Modified period for test for maintaining same ownership

707‑210 Utilisation of certain losses transferred from a company depends on company that made the losses earlier

Subdivision 707‑C—Amount of transferred losses that can be utilised

Guide to Subdivision 707‑C

707‑300 What this Subdivision is about

Object

707‑305 Object of this Subdivision

How much of a transferred loss can be utilised?

707‑310 How much of a transferred loss can be utilised?

707‑315 What is a bundle of losses?

707‑320 What is the available fraction for a bundle of losses?

707‑325 Modified market value of an entity becoming a member of a consolidated group

707‑330 Losses transferred from former head company

707‑335 Limit on utilising transferred losses if circumstances change during income year

707‑340 Utilising transferred losses while exempt income remains

707‑345 Other provisions are subject to this Subdivision

Subdivision 707‑D—Special rules about losses

707‑400 Head company’s business before and after consolidation not compared

707‑410 Exit history rule does not treat entity as having made a loss

707‑415 Application of losses with nil available fraction for certain purposes

Division 709—Other rules applying when entities become subsidiary members etc.

Subdivision 709‑A—Franking accounts

Guide to Subdivision 709‑A

709‑50 What this Subdivision is about

Object

709‑55 Object of this Subdivision

Treatment of franking accounts at joining time

709‑60 Nil balance franking account for joining entity

Treatment of subsidiary member’s franking account

709‑65 Subsidiary member’s franking account does not operate

Treatment of head company’s franking account

709‑70 Credits arising in head company’s franking account

709‑75 Debits arising in head company’s franking account

Franking distributions by subsidiary member

709‑80 Subsidiary member’s distributions on employee shares and certain preference shares taken to be distributions by the head company

709‑85 Non‑share distributions by subsidiary members taken to be distributions by head company

709‑90 Subsidiary member’s distributions to foreign resident taken to be distributions by head company

Payment of group liability by former subsidiary member

709‑95 Payment of group liability by former subsidiary member

709‑100 Refund of income tax to former subsidiary member

Subdivision 709‑B—Imputation issues

Guide to Subdivision 709‑B

709‑150 What this Subdivision is about

Operative provisions

709‑155 Testing consolidated groups

709‑160 Subsidiary member is exempting entity

709‑165 Subsidiary member is former exempting entity

709‑170 Head company and subsidiary are exempting entities

709‑175 Head company is former exempting entity

Subdivision 709‑C—Treatment of excess franking deficit tax offsets when entity becomes a subsidiary member of a consolidated group

Guide to Subdivision 709‑C

709‑180 What this Subdivision is about

709‑185 Joining entity’s excess franking deficit tax offsets transferred to head company

709‑190 Exit history rule not to treat leaving entity as having a franking deficit tax offset excess

Subdivision 709‑D—Deducting bad debts

Guide to Subdivision 709‑D

709‑200 What this Subdivision is about

Application and object

709‑205 Application of this Subdivision

709‑210 Object of this Subdivision

Limit on deduction of bad debt

709‑215 Limit on deduction of bad debt

Extension of Subdivision to debt/equity swap loss

709‑220 Limit on deduction of swap loss

Division 711—Tax cost setting amount for membership interests where entities cease to be subsidiary members of consolidated groups

Guide to Division 711 218

711‑1 What this Division is about

Application and object of this Division

711‑5 Application and object of this Division

Tax cost setting amount for membership interests etc.

711‑10 Tax cost setting amount worked out under this Division

711‑15 Tax cost setting amount where no multiple exit

711‑20 What is the old group’s allocable cost amount for the leaving entity?

711‑25 Terminating values of the leaving entity’s assets—step 1 in working out allocable cost amount

711‑30 What is the head company’s terminating value for an asset?

711‑35 If head company becomes entitled to certain deductions—step 2 in working out allocable cost amount

711‑40 Liabilities owed to the leaving entity by members of the old group—step 3 in working out allocable cost amount

711‑45 Liabilities etc. owed by the leaving entity—step 4 in working out allocable cost amount

711‑46 Liability arising from transfer or assignment of securitised assets

711‑55 Tax cost setting amount for membership interests where multiple exit

711‑65 Membership interests treated as having been acquired before 20 September 1985

711‑70 Additional integrity rule if membership interests treated as having been acquired before 20 September 1985 under section 711‑65—application of Division 149 to head company

711‑75 Additional integrity rule if membership interests treated as having been acquired before 20 September 1985 under section 711‑65—application of CGT event K6

Division 713—Rules for particular kinds of entities

Subdivision 713‑A—Trusts

Working out a joined group’s allocable cost amount for a joining trust

713‑20 Increasing the step 1 amount for settled capital that could be distributed tax free in respect of discretionary interests

713‑25 Undistributed, realised profits that accrue to joined group before joining time and could be distributed tax free—step 3 in working out allocable cost amount

Determining destination of distribution by non‑fixed trust

713‑50 Factors to consider

Subdivision 713‑C—Some unit trusts treated like head companies of consolidated groups

Guide to Subdivision 713‑C

713‑120 What this Subdivision is about

Object of this Subdivision

713‑125 Object of this Subdivision

Choice to form a consolidated group

713‑130 Choosing to form a consolidated group

Effects of choice

713‑135 Effects of choice

713‑140 Modifications of the applied law

Subdivision 713‑E—Partnerships

Guide to Subdivision 713‑E

713‑200 What this Subdivision is about

Objects

713‑205 Objects of this Subdivision

Partnership cost setting interests etc.

713‑210 Partnership cost setting interests

713‑215 Terminating value for partnership cost setting interest

Setting tax cost of partnership cost setting interests

713‑220 Set tax cost of partnership cost setting interests if partner joins consolidated group

713‑225 Tax cost setting amount for partnership cost setting interest

Special rules where partnership joins consolidated group

713‑235 Partnership joins group—set tax cost of partnership assets

713‑240 Partnership joins group—tax cost setting amount for partnership asset

Special rules where partnership leaves consolidated group

713‑250 Partnership leaves group—standard provisions modified

713‑255 Partnership leaves group—tax cost setting amount for partnership cost setting interests

713‑260 Partnership leaves group—tax cost setting amount for assets consisting of being owed certain liabilities

713‑265 Partnership leaves group—adjustments to allocable cost amount of partner who also leaves group

Subdivision 713‑L—Life insurance companies

Guide to Subdivision 713‑L

713‑500 What this Subdivision is about

General modifications for life insurance companies

713‑505 Head company treated as a life insurance company

713‑510 Certain subsidiaries of life insurance companies cannot be members of consolidated group

713‑510A Disregard single entity rule in working out certain amounts in respect of life insurance company

Life insurance companies’ liabilities on joining consolidated group

713‑511 Treatment of certain liabilities for income year when life insurance company joins consolidated group

Tax cost setting rules for life insurance companies joining consolidated group

713‑515 Certain assets taken to be retained cost base assets where life insurance company joins group

713‑520 Valuing certain liabilities where life insurance company joins group

713‑525 Obligation to value certain assets and liabilities at joining time

Losses of life insurance companies joining consolidated group

713‑530 Treatment of certain losses of life insurance company

Losses of life insurance companies’ subsidiaries joining consolidated group

713‑535 Losses of entities whose membership interests are complying superannuation assets of life insurance company

713‑540 Losses of entities whose membership interests are segregated exempt assets of life insurance company

Imputation rules for life insurance companies joining consolidated group

713‑545 Treatment of franking surplus in franking account of life insurance subsidiary joining group

713‑550 Treatment of head company’s franking account after joining

Liabilities for life insurance companies leaving consolidated group

713‑565 Treatment of certain liabilities for income year when life insurance company leaves consolidated group

Losses for life insurance companies leaving consolidated group

713‑570 Certain losses transferred to leaving company

Tax cost setting rules for life insurance companies leaving consolidated group

713‑575 Terminating value of certain assets where life insurance company leaves group

713‑580 Valuing certain liabilities where life insurance company leaves group

713‑585 Obligation to value certain assets and liabilities at leaving time

Subdivision 713‑M—General insurance companies

Guide to Subdivision 713‑M

713‑700 What this Subdivision is about

Tax cost setting rules for general insurance companies joining consolidated group

713‑705 Certain assets taken to be retained cost base assets where general insurance company joins group

Liabilities and reserves of general insurance companies joining and leaving consolidated groups

713‑710 Treatment of liabilities and reserves for income year when general insurance company joins or leaves group

713‑715 If general insurance company joins consolidated group

713‑720 If general insurance company leaves consolidated group

713‑725 Treatment of certain assets and liabilities of general insurance companies

Division 715—Interactions between this Part and other areas of the income tax law

Subdivision 715‑A—Treatment of unrealised losses existing when ownership or control of a company changes before or during consolidation

Object

715‑15 Object of this Subdivision

Effect on Subdivision 165‑CC of a company becoming a member of a consolidated group

715‑25 Subdivision 165‑CC stops applying to earlier changeover time

715‑30 Meaning of 165‑CC tagged asset

715‑35 Meaning of final RUNL

165‑CC tagged assets that affect tax cost setting amounts

715‑50 Step 1 amount is reduced if membership interest in subsidiary member is 165‑CC tagged asset and business continuity test is failed

715‑55 Step 2 amount is affected if liability of subsidiary member is 165‑CC tagged asset of another group member and business continuity test is failed

165‑CC tagged assets that form loss denial pools of head company when consolidated group is formed

715‑60 Assets that the head company already owns

715‑70 Assets of subsidiary member that become those of head company

How Subdivision 165‑CC applies to consolidated groups

715‑75 Extension of single entity rule and entry history rule

Effect on Subdivision 165‑CC of entity leaving consolidated group

715‑80 Application of sections 715‑85 to 715‑110

715‑85 First changeover time for leaving company at or after leaving time

715‑90 How business continuity test applies if leaving time is changeover time for leaving company

715‑95 If ownership and control of leaving entity have not changed since head company’s last changeover time

715‑100 First choice: adjustable values of leaving assets reduced to nil

715‑105 Second choice: head company’s final RUNL applied in reducing adjustable values of leaving assets that are loss assets

715‑110 Third choice: loss denial pool of leaving entity created

Effect of assets in loss denial pool of head company becoming assets of leaving entity

715‑120 What happens

715‑125 First choice: adjustable values of leaving assets reduced to nil

715‑130 Second choice: pool’s loss denial balance applied in reducing adjustable values of leaving assets that are loss assets

715‑135 Third choice: loss denial pool of leaving entity created

Effect of first and second choices on various kinds of assets

715‑145 Effect of choice on adjustable value of leaving asset

General provisions about loss denial pools

715‑155 When asset leaves pool

715‑160 How loss denial balance is applied to losses realised on assets in pool

715‑165 When pool ceases to exist

Choices under this Subdivision

715‑175 When choice must be made

715‑180 Head company to notify leaving entity of choice

715‑185 Leaving entity may choose to cancel loss denial pool by reducing adjustable values of assets in the pool

Subdivision 715‑B—How Subdivision 165‑CD applies to consolidated groups and leaving entities

How Subdivision 165‑CD applies to consolidated groups

715‑215 Extension of single entity rule and entry history rule

715‑225 Working out adjusted unrealised loss using individual asset method

715‑230 No reductions or other consequences for interests subject to loss cancellation under Subdivision 715‑H

How Subdivision 165‑CD applies to leaving entity that is a company

715‑240 Application of sections 715‑245 to 715‑260

715‑245 If ownership or control of leaving entity has altered since head company’s last alteration time or formation of group

715‑250 If head company has had an alteration time but ownership and control of leaving entity have not altered since

715‑255 Consequences if leaving entity is a loss company at the leaving time

715‑260 If neither of sections 715‑245 and 715‑250 applies

715‑265 Head company does not have relevant equity or debt interest in a loss company if widely held top company does not have such an interest

How Subdivision 165‑CD applies to leaving entity that is a trust

715‑270 Subdivision 165‑CD applies

Subdivision 715‑C—Common rules for the purposes of Subdivisions 715‑A and 715‑B

715‑290 Additional assumptions to be made when using reference time

Subdivision 715‑D—Treatment of company’s deferred losses under Subdivision 170‑D on joining a consolidated group

Key terminology

715‑310 What is a 170‑D deferred loss, and when it revives

Deferred loss on 165‑CC tagged asset

715‑355 Head company’s own deferred losses at formation time

715‑360 Deferred losses brought in by subsidiary member

715‑365 How loss denial balance is applied when 170‑D deferred loss revives

Subdivision 715‑E—Interactions with Division 775 (Foreign currency gains and losses)

715‑370 Cost setting—reference time for determining currency exchange rate effect

Subdivision 715‑F—Interactions with Division 230 (financial arrangements)

715‑375 Cost setting on joining—amount of liability that is Division 230 financial arrangement

715‑378 Cost setting on joining—head company’s right to receive or obligation to provide payment

715‑379 Cost setting on leaving—amount of intragroup liability that is Division 230 financial arrangement

715‑379A Cost setting on leaving—head company’s or leaving entity’s right to receive or obligation to provide payment

715‑380 Exit history rule not to affect certain matters related to Division 230 financial arrangements

715‑385 Exit history rule and elective methods applying to Division 230 financial arrangements

Subdivision 715‑G—How value shifting rules apply to a consolidated group

715‑410 Extension of single entity rule and entry history rule

715‑450 No reductions or other consequences for interests subject to loss cancellation under Subdivision 715‑H

Subdivision 715‑H—Cancelling loss on realisation event for direct or indirect interest in a member of a consolidated group

715‑610 Cancellation of loss

715‑615 Exception for interests in entity leaving consolidated group

715‑620 Exception if loss attributable to certain matters

Subdivision 715‑J—Entry history rule and choices

Head company’s choice overriding entry history rule

715‑660 Head company’s choice overriding entry history rule

Choices head company can make ignoring entry history rule to override inconsistencies

715‑665 Head company’s choice to override inconsistency

Choices with ongoing effect

715‑670 Ongoing effect of choices made by entities before joining group

715‑675 Head company adopting choice with ongoing effect

Subdivision 715‑K—Exit history rule and choices

Choices leaving entity can make ignoring exit history rule

715‑700 Choices leaving entity can make ignoring exit history rule

Choices leaving entity can make ignoring exit history rule to overcome inconsistencies

715‑705 Choices leaving entity can make ignoring exit history rule to overcome inconsistencies

Subdivision 715‑U—Effect on conduit foreign income

715‑875 Extension of single entity rule and entry history rule

715‑880 No CFI for leaving entity

Subdivision 715‑V—Entity ceasing to be exempt from income tax on becoming subsidiary member of consolidated group

715‑900 Transition time taken to be just before joining time

Subdivision 715‑W—Effect on arrangements where CGT roll‑overs are obtained

715‑910 Effect on restructures—original entity becomes a subsidiary member

715‑915 Effect on restructures—original entity is a head company

715‑920 Effect on restructures—original entity is a head company that becomes a subsidiary member of another group

715‑925 Effect on restructures—original entity ceases being a subsidiary member

Division 716—Miscellaneous special rules

Subdivision 716‑A—Assessable income and deductions spread over several membership or non‑membership periods

Guide to Subdivision 716‑A

716‑1 What this Division is about

Operative provisions

716‑15 Assessable income spread over 2 or more income years

716‑25 Deductions spread over 2 or more income years

716‑70 Capital expenditure that is fully deductible in one income year

Assessable income and deductions arising from share of net income of a partnership or trust, or from share of partnership loss

716‑75 Application

716‑80 Head company’s assessable income and deductions

716‑85 Entity’s assessable income and deductions for a non‑membership period

716‑90 Entity’s share of assessable income or deductions of partnership or trust

716‑95 Special rule if not all partnership or trust’s assessable income or deductions taken into account in working out amount

716‑100 Spreading period

Subdivision 716‑E—Tax cost setting for exploration and prospecting assets

716‑300 Prime cost method of working out decline in value

Subdivision 716‑G—Low‑value and software development pools

Assets in joining entity’s low‑value pool

716‑330 Head company’s deductions for decline in value of assets in joining entity’s low‑value pool

Entity leaving group with asset allocated to head company’s low‑value pool

716‑335 Entity leaving group with asset allocated to head company’s low‑value pool

Depreciating assets arising from expenditure in joining entity’s software development pool

716‑340 Depreciating assets arising from expenditure in joining entity’s software development pool

Software development pools if entity leaves consolidated group

716‑345 Head company taken not to have incurred expenditure

Subdivision 716‑S—Miscellaneous consequences of tax cost setting

716‑400 Tax cost setting and bad debts

716‑440 Membership interests in joining entity not subject to CGT under Division 855—foreign entity ceasing to hold interests

Subdivision 716‑V—Research and Development

716‑500 Head company bound by agreements binding on subsidiary members

716‑505 History for entitlement to tax offset: joining entity

716‑510 History for entitlement to tax offset: leaving entity

Subdivision 716‑Z—Other

716‑800 Allocating amounts to periods if head company and subsidiary member have different income years

716‑850 Grossing up threshold amounts for periods of less than 365 days

716‑855 Working out the cost base or reduced cost base of a pre‑CGT asset after certain roll‑overs

716‑860 CGT event straddling joining or leaving time

Division 717—International tax rules

Subdivision 717‑A—Foreign income tax offsets

717‑1 What this Subdivision is about

Object

717‑5 Object of this Subdivision

Foreign income tax on amounts in head company’s assessable income

717‑10 Head company taken to be liable for subsidiary member’s foreign income tax

Subdivision 717‑D—Transfer of certain surpluses under CFC provisions and former FIF and FLP provisions: entry rules

Guide to Subdivision 717‑D

717‑200 What this Subdivision is about

Object

717‑205 Object of this Subdivision

Transfers

717‑210 Attribution surpluses

717‑220 FIF surpluses

717‑227 Deferred attribution credits

Subdivision 717‑E—Transfer of certain surpluses under CFC provisions and former FIF and FLP provisions: exit rules

Guide to Subdivision 717‑E

717‑235 What this Subdivision is about

Object

717‑240 Object of this Subdivision

Transfers

717‑245 Attribution surpluses

717‑255 FIF surpluses

717‑262 Deferred attribution credits

Subdivision 717‑O—Offshore banking units

Guide to Subdivision 717‑O

717‑700 What this Subdivision is about

717‑705 Object of this Subdivision

717‑710 Head company treated as OBU

Division 719—MEC groups

Subdivision 719‑A—Modified application of Part 3‑90 to MEC groups

719‑2 Modified application of Part 3‑90 to MEC groups

Subdivision 719‑B—MEC groups and their members

719‑4 What this Subdivision is about

Basic concepts

719‑5 What is a MEC group?

719‑10 What is a potential MEC group?

719‑15 What is an eligible tier‑1 company?

719‑20 What is a top company and a tier‑1 company?

719‑25 Head company, subsidiary members and members of a MEC group

719‑30 Treating entities as wholly‑owned subsidiaries by disregarding employee shares

719‑35 Treating entities held through non‑fixed trusts as wholly‑owned subsidiaries

719‑40 Special conversion event—potential MEC group

719‑45 Application of sections 703‑20 and 703‑25

Choice to consolidate a potential MEC group

719‑50 Eligible tier‑1 companies may choose to consolidate a potential MEC group

719‑55 When choice starts to have effect

Provisional head company

719‑60 Appointment of provisional head company

719‑65 Qualifications for the provisional head company of a MEC group

719‑70 Income year of new provisional head company to be the same as that of former provisional head company

Head company

719‑75 Head company

Notice of events affecting group

719‑76 Notice of choice to consolidate

719‑77 Notice in relation to new eligible tier‑1 members etc.

719‑78 Notice of special conversion event

719‑79 Notice of appointment of provisional head company after formation of group

719‑80 Notice of events affecting MEC group

Effects of change of head company

719‑85 Application

719‑90 New head company treated as substituted for old head company at all times before the transition time

719‑95 No consequences of old head company becoming, and new head company ceasing to be, subsidiary member of the group

Subdivision 719‑BA—Group conversions involving MEC groups

719‑120 Application

719‑125 Head company of new group retains history of head company of old group

719‑130 Provisions of this Part not to apply to conversion

719‑135 Provisions of this Part applying to conversion despite section 719‑130

719‑140 Other provisions of this Part not applying to conversion

Subdivision 719‑C—MEC group cost setting rules: joining cases

Guide to Subdivision 719‑C

719‑150 What this Subdivision is about

Application and object

719‑155 Object of this Subdivision

Modified application of tax cost setting rules for joining

719‑160 Tax cost setting rules for joining have effect with modifications

719‑165 Trading stock value and registered emissions unit value not set for assets of eligible tier‑1 companies

719‑170 Modified effect of subsections 705‑175(1) and 705‑185(1)

Subdivision 719‑F—Losses

Guide to Subdivision 719‑F

719‑250 What this Subdivision is about

Maintaining the same ownership to be able to utilise loss

719‑255 Special rules

719‑260 Special test for utilising a loss because a company maintains the same owners

719‑265 What is the test company?

719‑270 Assumptions about the test company having made the loss for an income year

719‑275 Assumptions about nothing happening to affect direct and indirect ownership of the test company

719‑280 Assumptions about the test company failing to meet the conditions in section 165‑12

Business continuity test and change of head company

719‑285 Business continuity test and change of head company

Bundles of losses and their available fractions

719‑300 Application

719‑305 Subdivision 707‑C affects utilisation of losses made by ongoing head company while it was head company

719‑310 Adjustment of available fractions for bundles of losses previously transferred to ongoing head company

719‑315 Further adjustment of available fractions for all bundles

719‑320 Limit on utilising losses other than the prior group losses

719‑325 Cancellation of all losses in a bundle

Subdivision 719‑H—Imputation issues

719‑425 Guide to Subdivision 719‑H

Operative provisions

719‑430 Transfer of franking account balance on cessation event

719‑435 Distributions by subsidiary members of MEC group taken to be distributions by head company

Subdivision 719‑I—Bad debts

Guide to Subdivision 719‑I

719‑450 What this Subdivision is about

Maintaining the same ownership to be able to deduct bad debt

719‑455 Special test for deducting a bad debt because a company maintains the same owners

719‑460 Assumptions about nothing happening to affect direct and indirect ownership of the test company

719‑465 Assumptions about the test company failing to meet the conditions in section 165‑123

Subdivision 719‑J—MEC group cost setting rules: leaving cases

Guide to Subdivision 719‑J

719‑500 What this Subdivision is about

719‑505 Application and object of this Subdivision

719‑510 Modified operation of paragraphs 711‑15(1)(b) and (c)

Subdivision 719‑K—MEC group cost setting rules: pooling cases

Guide to Subdivision 719‑K

719‑550 What this Subdivision is about

719‑555 Application and object of this Subdivision

719‑560 Pooled interests

719‑565 Setting cost of reset interests

719‑570 Cost setting amount

Subdivision 719‑T—Interactions between this Part and other areas of the income tax law: special rules for MEC groups

How Subdivision 165‑CC applies to MEC groups

719‑700 Changeover times under section 165‑115C or 165‑115D

719‑705 Additional changeover times for head company of MEC group

How Subdivision 165‑CD applies to MEC groups

719‑720 Alteration times under section 165‑115L or 165‑115M

719‑725 Additional alteration times for head company of MEC group

719‑730 Some alteration times only affect interests in top company

719‑735 Some alteration times affect only pooled interests

719‑740 Head company does not have relevant equity or debt interest in a loss company if widely held top company does not have such an interest

How indirect value shifting rules apply to a MEC group

719‑755 Effect on MEC group cost setting rules if head company is losing entity or gaining entity for indirect value shift

Cancelling loss on realisation event for direct or indirect interest in a subsidiary member of a MEC group

719‑775 Cancellation of loss

719‑780 Exception for pooled interests in eligible tier‑1 companies

719‑785 Exception for interests in top company

719‑790 Exception for interests in entity leaving MEC group

719‑795 Exception if loss attributable to certain matters

Division 721—Liability for payment of tax where head company fails to pay on time

Guide to Division 721 476

721‑1 What this Division is about

Object

721‑5 Object of this Division

When this Division operates

721‑10 When this Division operates

Joint and several liability of contributing member

721‑15 Head company and contributing members jointly and severally liable to pay group liability

721‑17 Notice of joint and several liability for general interest charge

721‑20 Limit on liability where group first comes into existence

Tax sharing agreements

721‑25 When a group liability is covered by a tax sharing agreement

721‑30 TSA contributing members liable for contribution amounts

721‑32 Notice of general interest charge liability under TSA

721‑35 When a TSA contributing member has left the group clear of the group liability

721‑40 TSA liability and group liability are linked

Chapter 3—Specialist liability rules

Part 3‑80—Roll‑overs applying to assets generally

Division 615—Roll‑overs for business restructures

Table of Subdivisions

Guide to Division 615

615‑A Choosing to obtain roll‑overs

615‑B Further requirements for choosing to obtain roll‑overs

615‑C Consequences of roll‑overs

615‑D Consequences for the interposed company

Guide to Division 615

615‑1 What this Division is about

You can choose for transactions under a scheme to restructure a company’s or unit trust’s business to be tax neutral if, under the scheme:

(a) you cease to own shares in the company or units in the trust; and

(b) in exchange, you become the owner of new shares in another company.

Subdivision 615‑A—Choosing to obtain roll‑overs

Table of sections

615‑5 Disposing of interests in one entity for shares in a company

615‑10 Redeeming or cancelling interests in one entity for shares in a company

615‑5 Disposing of interests in one entity for shares in a company

(1) You can choose to obtain a roll‑over if:

(a) you are a *member of a company or a unit trust (the original entity); and

(b) you and at least one other entity (the exchanging members) own all the *shares or units in it; and

(c) under a *scheme for reorganising its affairs, the exchanging members *dispose of all their shares or units in it to a company (the interposed company) in exchange for shares in the interposed company (and nothing else); and

(d) the requirements in Subdivision 615‑B are satisfied.

Note 1: For paragraph (c), see section 124‑20 if an exchanging member uses a share sale facility.

Note 2: After the completion of the scheme, later dealings between the interposed company and the original entity may be subject to the rules for consolidated groups (see Part 3‑90).

(2) You are taken to have chosen to obtain the roll‑over if:

(a) immediately before the completion time (see section 615‑15), the original entity is the *head company of a *consolidated group; and

(b) immediately after the completion time, the interposed company is the head company of the group.

Note: The consolidated group continues in existence because of section 703‑70.

615‑10 Redeeming or cancelling interests in one entity for shares in a company

(1) You can choose to obtain a roll‑over if you are a *member of a company or a unit trust (the original entity), and under a *scheme for reorganising its affairs:

(a) a company (the interposed company) *acquires one or more, but not all, of the *shares or units in the original entity; and

(b) these are the first shares or units that the interposed company acquires in the original entity; and

(c) you and at least one other entity (the exchanging members) own all the remaining shares or units in the original entity; and

(d) those remaining shares or units are redeemed or cancelled; and

(e) each exchanging member receives shares (and nothing else) in the interposed company in return for their shares or units in the original entity being redeemed or cancelled;

and the requirements in Subdivision 615‑B are satisfied.

Note: For paragraph (e), see section 124‑20 if an exchanging member uses a share sale facility.

(2) You are taken to have chosen to obtain the roll‑over if:

(a) immediately before the completion time (see section 615‑15), the original entity is the *head company of a *consolidated group; and

(b) immediately after the completion time, the interposed company is the head company of the group.

Note: The consolidated group continues in existence because of section 703‑70.

(3) The original entity, or its trustee if it is a unit trust, can issue other *shares or units to the interposed company as part of the *scheme.

Note: Some of the interposed company’s shares or units in the original entity may be taken to be acquired before 20 September 1985: see section 615‑65.

Subdivision 615‑B—Further requirements for choosing to obtain roll‑overs

Table of sections

615‑15 Interposed company must own all the original interests

615‑20 Requirements relating to your interests in the original entity

615‑25 Requirements relating to the interposed company

615‑30 Interposed company must make a particular choice

615‑35 ADI restructures—disregard certain preference shares

615‑15 Interposed company must own all the original interests

The interposed company must own all the *shares or units in the original entity immediately after the time (the completion time) all the exchanging members have had their shares or units in the original entity disposed of, redeemed or cancelled under the *scheme.

615‑20 Requirements relating to your interests in the original entity

(1) Immediately after the completion time, each exchanging member must own:

(a) a whole number of *shares in the interposed company; and

(b) a percentage of the shares in the interposed company that were issued to all the exchanging members that is equal to the percentage of the shares or units in the original entity that were:

(i) owned by the member; and

(ii) disposed of, redeemed or cancelled under the *scheme.

(2) The following ratios must be equal:

(a) the ratio of:

(i) the *market value of each exchanging member’s *shares in the interposed company; to

(ii) the market value of the shares in the interposed company issued to all the exchanging members (worked out immediately after the completion time);

(b) the ratio of:

(i) the market value of that member’s shares or units in the original entity that were disposed of, redeemed or cancelled under the *scheme; to

(ii) the market value of all the shares or units in the original entity that were disposed of, redeemed or cancelled under the scheme (worked out immediately before the first disposal, redemption or cancellation).

Example 1: There are 100 shares in A Pty Ltd (the original entity), all having the same rights. B Pty Ltd (the interposed company) acquires all the shares in A by issuing each shareholder in A 10 shares in itself for each share they have in A. All shares in B have the same rights. Bill owned 15 shares in A and received 150 shares in B in exchange.

Example 2: There are 1,000 units in the A unit trust (the original entity), all having the same rights. 2 new units in A are issued to B Pty Ltd (the interposed company), and all other units in A are cancelled. Each unitholder in A is issued 10 shares in B for each 100 units they have in A. All shares in B have the same rights. Alison owned 200 units in A and received 20 shares in B in exchange.

(3) Either:

(a) you are an Australian resident at the time your *shares or units in the original entity are disposed of, redeemed or cancelled under the *scheme; or

(b) if you are a foreign resident at that time:

(i) your shares or units in the original entity were *taxable Australian property immediately before that time; and

(ii) your shares in the interposed company are taxable Australian property immediately after the completion time.

615‑25 Requirements relating to the interposed company

(1) The *shares issued in the interposed company must not be *redeemable shares.

(2) Each exchanging member who is issued *shares in the interposed company must own the shares from the time they are issued until at least the completion time.

(3) Immediately after the completion time:

(a) the exchanging members must own all the *shares in the interposed company; or

(b) entities other than those members must own no more than 5 shares in the interposed company, and the *market value of those shares expressed as a percentage of the market value of all the shares in the interposed company must be such that it is reasonable to treat the exchanging members as owning all the shares.

615‑30 Interposed company must make a particular choice

(1) Unless subsection (2) applies, the interposed company must choose that section 615‑65 applies.

(2) The interposed company must choose that a *consolidated group continues in existence at and after the completion time with the interposed company as its *head company, if:

(a) immediately before the completion time, the consolidated group consisted of the original entity as head company and one or more other members (the other group members); and

(b) immediately after the completion time, the interposed company is the head company of a *consolidatable group consisting only of itself and the other group members.

Note: Sections 703‑65 to 703‑80 deal with the effects of the choice for the consolidated group.

(3) A choice under subsection (1) or (2) must be made:

(a) within 2 months after the completion time, if the choice is under subsection (1); or

(b) within 28 days after the completion time, if the choice is under subsection (2); or

(c) within such further time as the Commissioner allows.

The choice cannot be revoked.

(4) The way the interposed company prepares its *income tax returns is sufficient evidence of the making of the choice.

615‑35 ADI restructures—disregard certain preference shares

For the purposes of this Division, disregard any *shares in the original entity that can be disregarded under subsection 703‑37(4) if:

(a) the interposed company is a non‑operating holding company within the meaning of the Financial Sector (Transfer and Restructure) Act 1999; and

(b) a restructure instrument under Part 4A of that Act is in force in relation to the interposed company; and

(c) because of the restructure to which the instrument relates, an *ADI becomes a subsidiary (within the meaning of that Act) of the interposed company; and

(d) the original entity is:

(i) the ADI; or

(ii) part of an extended licensed entity (within the meaning of the *prudential standards) that includes the ADI.

Subdivision 615‑C—Consequences of roll‑overs

Table of sections

615‑40 CGT consequences

615‑45 Additional consequences—deferral of profit or loss

615‑50 Trading stock

615‑55 Revenue assets

615‑60 Disregard CGT exemption for trading stock

615‑40 CGT consequences

The consequences set out in Subdivision 124‑A also apply to a roll‑over under this Division as if that roll‑over were a roll‑over covered by Division 124 (about replacement‑asset roll‑overs).

Note: Those consequences generally involve:

(a) disregarding a capital gain or capital loss you make from the disposal, redemption or cancellation of your shares or units in the original entity; and

(b) working out the first element of the cost base of each of your new shares in the interposed entity by reference to the cost bases of your shares or units in the original entity.

615‑45 Additional consequences—deferral of profit or loss

The additional consequences in sections 615‑50 and 615‑55 apply if:

(a) under this Division:

(i) you are taken to have chosen to obtain the roll‑over; or

(ii) you otherwise choose to obtain the roll‑over; and

(b) if subparagraph (a)(ii) applies to you, you choose for these additional consequences to apply; and

(c) some or all of your *shares or units in the original entity at the time immediately before they were:

(i) disposed of as described in paragraph 615‑5(1)(c); or

(ii) redeemed or cancelled as described in paragraph 615‑10(1)(d);

had the character of being your *trading stock or *revenue assets; and

(d) the shares in the interposed company that you acquired in return for those shares or units have the same character.

Note 1: Apply this section separately for assets of each character.

Note 2: The CGT exemption for trading stock does not prevent you obtaining the roll‑over (see section 615‑60).

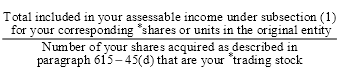

615‑50 Trading stock

(1) The amount included in your assessable income because of the disposal, redemption or cancellation of each of your *shares or units described in paragraph 615‑45(c) that was your *trading stock at the time mentioned in that paragraph is equal to:

(a) if the share or unit had been your trading stock ever since the start of the income year that included that time—the total of:

(i) its *value as trading stock at the start of the income year; and

(ii) the amount (if any) by which its cost had increased since the start of the income year; or

(b) otherwise—its cost at that time.

(2) For each of the *shares that you acquired as described in paragraph 615‑45(d) that is your *trading stock, you are taken to have paid:

(3) For the purposes of Division 70 (about trading stock), you, the original entity and the interposed company are taken to have dealt with each other in the ordinary course of *business and at *arm’s length for each of the transactions referred to in paragraph 615‑5(1)(c) or 615‑10(1)(d) or (e).

615‑55 Revenue assets

(1) For each of your *shares or units that:

(a) is described in paragraph 615‑45(c); and

(b) was a *revenue asset immediately before its disposal, redemption or cancellation;

your gross proceeds for that disposal, redemption or cancellation are taken to be the amount you would have needed to have received in order to have a nil profit and nil loss for that disposal, redemption or cancellation.

(2) For the purpose of calculating any profit or loss on a future disposal, cessation of ownership, or other realisation of a *share that:

(a) you acquired as described in paragraph 615‑45(d); and

(b) is a *revenue asset;

you are taken to have paid the following for your acquisition of that share:

615‑60 Disregard CGT exemption for trading stock

For the purposes of this Division, disregard section 118‑25 (which gives a CGT exemption for trading stock).

Subdivision 615‑D—Consequences for the interposed company

Table of sections

615‑65 Consequences for the interposed company

615‑65 Consequences for the interposed company

(1) This section applies if the interposed company so chooses under subsection 615‑30(1).

(2) A number of the *shares or units that the interposed company owns in the original entity (immediately after the completion time) are taken to have been *acquired before 20 September 1985 if any of the original entity’s assets as at the completion time were acquired by it before that day.

Note: Generally, a capital gain or capital loss you make from a CGT asset that you acquired before 20 September 1985 can be disregarded: see Division 104.

(3) That number (worked out as at the completion time) is the greatest possible whole number that (when expressed as a percentage of all the *shares or units) does not exceed:

(a) the *market value of the original entity’s assets that it *acquired before 20 September 1985; less

(b) its liabilities (if any) in respect of those assets;

expressed as a percentage of the market value of all the original entity’s assets less all of its liabilities.

(4) The first element of the *cost base of the interposed company’s *shares or units in the original entity that are not taken to have been *acquired before 20 September 1985 is:

(a) the total of the cost bases (as at the completion time) of the original entity’s assets that it acquired on or after that day; less

(b) its liabilities (if any) in respect of those assets.

The first element of the *reduced cost base of those shares or units is worked out similarly.

(5) A liability of the original entity that is not a liability in respect of a specific asset or assets of the original entity is taken to be a liability in respect of all the assets of the original entity.

Note: An example is a bank overdraft.

(6) If a liability is in respect of 2 or more assets, the proportion of the liability that is in respect of any one of those assets is equal to:

Division 620—Assets of wound‑up corporation passing to corporation with not significantly different ownership

Table of Subdivisions

620‑A Corporations covered by Subdivision 124‑I

Subdivision 620‑A—Corporations covered by Subdivision 124‑I

Guide to Subdivision 620‑A

620‑5 What this Subdivision is about

There are tax‑neutral consequences of a body, that is incorporated under one law and ceases to exist, disposing of an asset to a company incorporated under another law, if the ownership of the company is not significantly different from the ownership of the body.

Table of sections

Application and object of this Subdivision

620‑10 Application

620‑15 Object

CGT consequences

620‑20 Disregard body’s capital gains and losses from CGT assets

620‑25 Cost base and pre‑CGT status of CGT asset for company

Consequences for depreciating assets

620‑30 Roll‑over relief for balancing adjustment events

Consequences for trading stock

620‑40 Body taken to have sold trading stock to company

Consequences for revenue assets

620‑50 Body taken to have sold revenue assets to company

Application and object of this Subdivision

620‑10 Application

This Subdivision applies to a body that is incorporated under one law and ceases to exist, and to a company incorporated under another law, if section 124‑525 applies in relation to the body and the company.

Note: That section applies if the ownership of the company is not significantly different from the ownership of the body and rights relating to the body.

620‑15 Object

The object of this Subdivision is to ensure tax‑neutral consequences when the body ceases to hold an asset and also if the asset becomes held by the company.

CGT consequences

620‑20 Disregard body’s capital gains and losses from CGT assets

(1) This section applies if:

(a) the body *disposes of a *CGT asset to the company because the body ceases to exist; or

(b) another *CGT event happens to a CGT asset of the body because the body ceases to exist.

(2) A *capital gain or a *capital loss the body makes from the *CGT asset is disregarded.

620‑25 Cost base and pre‑CGT status of CGT asset for company

(1) This section applies to a *CGT asset if the body *disposes of it to the company because the body ceases to exist.

(2) The first element of the *CGT asset’s *cost base for the company is equal to the asset’s cost base for the body in connection with the *disposal.

(3) The first element of the *CGT asset’s *reduced cost base for the company is worked out similarly.

(4) If the body *acquired the *CGT asset before 20 September 1985, the company is taken to have acquired the CGT asset before that day.

Consequences for depreciating assets

620‑30 Roll‑over relief for balancing adjustment events

(1) This section applies if:

(a) there is a *balancing adjustment event because the body disposes of a *depreciating asset in an income year to the company because the body ceases to exist; and

(b) the disposal involves a *CGT event.

(2) This Act applies as if:

(a) there were roll‑over relief under subsection 40‑340(1) for the *balancing adjustment event; and

(b) the body were the transferor mentioned in that subsection and subsection 328‑243(1A); and

(c) the company were the transferee mentioned in that subsection and subsection 328‑243(1A).

Note: Some effects of this are as follows:

(a) the balancing adjustment event does not affect the body’s assessable income or deductions (see subsection 40‑345(1));

(b) the company can deduct for the decline in value of the asset on the same basis as the body did (see subsection 40‑345(2));

(c) Division 45 (Disposal of leases and leased plant) applies to the company as if it had done the things the body did (see subsection 40‑350(1)).

(3) Disregard paragraph 328‑243(1A)(c) in determining whether subsection 328‑243(1A) applies.

Consequences for trading stock

620‑40 Body taken to have sold trading stock to company

(1) This subsection applies to each item of *trading stock that the body disposes of to the company because the body ceases to exist.

(2) The body is taken to have sold, and the company is taken to have bought, the item (in the ordinary course of *business and dealing with each other at *arm’s length), at the time of the disposal (or just before that time if the disposal occurred when the body ceased to exist), for:

(a) the *cost of the item for the body; or

(b) if the body held the item as *trading stock at the start of the income year, the *value of the item for the body then.

(3) The company is taken to have held the item as *trading stock when it bought the item.

Consequences for revenue assets

620‑50 Body taken to have sold revenue assets to company

Disposal

(1) Subsections (2) and (3) apply to a *CGT asset:

(a) that the body *disposes of to the company because the body ceases to exist; and

(b) that is a *revenue asset of the body just before the disposal.

Note: Trading stock and depreciating assets are not revenue assets. See section 977‑50.

(2) The body is taken to have disposed of the *revenue asset to the company for an amount such that the body would not make a profit or a loss on the disposal.

(3) For the purpose of calculating any profit or loss on a future disposal of, cessation of owning, or other realisation of, the *revenue asset, the company is taken to have paid the body that amount for the disposal of the revenue asset to the company.

Ceasing to own or other realising

(4) Subsection (5) applies to a *CGT asset:

(a) that the body ceases to own, or otherwise realises, because the body ceases to exist; and

(b) that is a *revenue asset of the body just before the cessation or realisation.

Note: Trading stock and depreciating assets are not revenue assets. See section 977‑50.

(5) The body is taken to have disposed of the *revenue asset for an amount such that the body would not make a profit or a loss on the disposal.

Part 3‑90—Consolidated groups

Division 700—Guide and objects

Table of sections

Guide

700‑1 What this Part is about

700‑5 Overview of this Part

Objects

700‑10 Objects of this Part

Guide

700‑1 What this Part is about

This Part allows certain groups of entities to be treated as single entities for income tax purposes.

Following a choice to consolidate, subsidiary members are treated as part of the head company of the group rather than as separate income tax identities. The head company inherits their income tax history when they become subsidiary members of the group. On ceasing to be subsidiary members, they take with them an income tax history that recognises that they are different from when they became subsidiary members.

This is supported by rules that:

(a) set the cost for income tax purposes of assets that subsidiary members bring into the group; and

(b) determine the income tax history that is taken into account when entities become, or cease to be, subsidiary members of the group; and

(c) deal with the transfer of tax attributes such as losses and franking credits to the head company when entities become subsidiary members of the group.

700‑5 Overview of this Part

(1) The single entity rule determines how the income tax liability of a consolidated group will be ascertained. The basic principle is contained in the Core Rules in Division 701.

(2) Essentially, a consolidated group consists of an Australian resident head company and all of its Australian resident wholly‑owned subsidiaries (which may be companies, trusts or partnerships). Special rules apply to foreign‑owned groups with no single Australian resident head company.

(3) An eligible wholly‑owned group becomes a consolidated group after notice of a choice to consolidate is given to the Commissioner.

(4) This Part also contains rules which set the cost for income tax purposes of assets of entities when they become subsidiary members of a consolidated group and of membership interests in those entities when they cease to be subsidiary members of the group.

(5) Certain tax attributes (such as losses and franking credits) of entities that become subsidiary members of a consolidated group are transferred under this Part to the head company of the group. These tax attributes remain with the group after an entity ceases to be a subsidiary member.

Objects

700‑10 Objects of this Part

The objects of this Part are:

(a) to prevent double taxation of the same economic gain realised by a consolidated group; and

(b) to prevent a double tax benefit being obtained from an economic loss realised by a consolidated group; and

(c) to provide a systematic solution to the prevention of such double taxation and double tax benefits that will:

(i) reduce the cost of complying with this Act; and

(ii) improve business efficiency by removing complexities and promoting simplicity in the taxation of wholly‑owned groups.

Division 701—Core rules

Table of sections

Common rule

701‑1 Single entity rule

Head company rules

701‑5 Entry history rule

701‑10 Cost to head company of assets of joining entity

701‑15 Cost to head company of membership interests in entity that leaves group

701‑20 Cost to head company of assets consisting of certain liabilities owed by entity that leaves group

701‑25 Tax‑neutral consequence for head company of ceasing to hold assets when entity leaves group

Entity rules

701‑30 Where entity not subsidiary member for whole of income year

701‑35 Tax‑neutral consequence for entity of ceasing to hold assets when it joins group

701‑40 Exit history rule

701‑45 Cost of assets consisting of liabilities owed to entity by members of the group

701‑50 Cost of certain membership interests of which entity becomes holder on leaving group

Supporting provisions

701‑55 Setting the tax cost of an asset

701‑56 Application of subsection 701‑55(6)

701‑58 Effect of setting the tax cost of an asset that the head company does not hold under the single entity rule

701‑60 Tax cost setting amount

701‑60A Tax cost setting amount for asset emerging when entity leaves group

701‑61 Assets in relation to Division 230 financial arrangement—head company’s assessable income or deduction

701‑63 Right to future income and WIP amount asset

701‑65 Net income and losses for trusts and partnerships

701‑67 Assets in this Part are CGT assets, etc.

Exceptions

701‑70 Adjustments to taxable income where identities of parties to arrangement merge on joining group

701‑75 Adjustments to taxable income where identities of parties to arrangement re‑emerge on leaving group

701‑80 Accelerated depreciation

701‑85 Other exceptions etc. to the rules

Common rule

701‑1 Single entity rule

(1) If an entity is a *subsidiary member of a *consolidated group for any period, it and any other subsidiary member of the group are taken for the purposes covered by subsections (2) and (3) to be parts of the *head company of the group, rather than separate entities, during that period.

Head company core purposes

(2) The purposes covered by this subsection (the head company core purposes) are:

(a) working out the amount of the *head company’s liability (if any) for income tax calculated by reference to any income year in which any of the period occurs or any later income year; and

(b) working out the amount of the head company’s loss (if any) of a particular *sort for any such income year.

Note: The single entity rule would affect the head company’s income tax liability calculated by reference to income years after the entity ceased to be a member of the group if, for example, assets that the entity held when it became a subsidiary member remained with the head company after the entity ceased to be a subsidiary member.

Entity core purposes

(3) The purposes covered by this subsection (the entity core purposes) are:

(a) working out the amount of the entity’s liability (if any) for income tax calculated by reference to any income year in which any of the period occurs or any later income year; and

(b) working out the amount of the entity’s loss (if any) of a particular *sort for any such income year.

Note: An assessment of the entity’s liability calculated by reference to income tax for a period when it was not a subsidiary member of the group may be made, and that tax recovered from it, even while it is a subsidiary member.

What is a sort of loss?

(4) Each of these paragraphs identifies a sort of loss:

(a) *tax loss;

(b) *film loss;

(c) *net capital loss.

This subsection lists all the sorts of loss.

Head company rules

701‑5 Entry history rule

For the head company core purposes in relation to the period after the entity becomes a *subsidiary member of the group, everything that happened in relation to it before it became a subsidiary member is taken to have happened in relation to the *head company.

Note 1: Other provisions of this Part may affect the tax history that is inherited (e.g. asset cost base history is affected by section 701‑10 and tax loss history is affected by Division 707).

Note 3: Section 165‑212E overrides this rule for the purposes of the business continuity test.

701‑10 Cost to head company of assets of joining entity

(1) This section has effect for the head company core purposes when the entity becomes a *subsidiary member of the group.

Assets to which section applies

(2) This section applies in relation to each asset that would be an asset of the entity at the time it becomes a *subsidiary member of the group, assuming that subsection 701‑1(1) (the single entity rule) did not apply.

Note: See subsection 705‑35(3) for the treatment of a goodwill asset resulting from the head company’s ownership and control of the joining entity.

Object

(3) The object of this section (and Division 705 which relates to it) is to recognise the cost to the *head company of such assets as an amount reflecting the group’s cost of acquiring the entity.

Setting tax cost of assets

(4) Each asset’s *tax cost is set at the time the entity becomes a *subsidiary member of the group at the asset’s *tax cost setting amount.

Multiple setting of tax cost for same trading stock or registered emissions unit

(5) However, if:

(a) the asset is *trading stock or a *registered emissions unit; and

(b) the asset’s *tax cost is set by this section at more than one time (each of which is a setting time) for the same income year;

then, except where subsection (6) applies, only the amount at which the tax cost is set at the last of the setting times is to be taken into account.

(6) If:

(a) the *head company’s *terminating value for the asset; or

(b) the *value of the asset at the start of the income year;

is required to be worked out for one or more occasions when an entity (whether or not the same entity) ceases to be a *subsidiary member of the group in the income year, then the amount at which the asset’s *tax cost is set by this section at a particular setting time is only taken into account in working out the head company’s terminating value for a particular occasion if:

(c) the setting time occurs before the occasion; and

(d) there is no intervening setting time or occasion.

701‑15 Cost to head company of membership interests in entity that leaves group

(1) If the entity ceases to be a *subsidiary member of the group, this section has effect for the head company core purposes, so far as they relate to the income year in which the entity ceases to be a subsidiary member or any later income year.

Note: This section could have effect, for example, if an entity ceases to be a subsidiary member of the group because: