An Act relating to the small superannuation accounts scheme

Part 1—Introduction

1 Short title [see Note 1]

This Act may be cited as the Small Superannuation Accounts Act 1995.

2 Commencement

This Act commences on 1 July 1995.

3 Simplified explanation

The following is a simplified explanation of this Act:

• The Australian Taxation Office administers a Special Account. Notional accounts are kept within the Special Account. Employers may deposit money for their employees instead of making superannuation contributions. These deposits are credited to the notional accounts.

• The account offers employees with small balances an opportunity to avoid the erosion of those balances by fees.

• Employees may request that account balances be transferred to a nominated superannuation fund or RSA.

• Except in special cases, employees will not have direct access to their account balances.

• Interest will be calculated on the daily balance of the account and credited to the account on a quarterly basis.

• Interest is exempt from income tax.

• If an account balance exceeds $1,200, interest will only be credited on the first $1,200 of the balance. This is an incentive for employees to request that balances of more than $1,200 be transferred to a superannuation fund.

• Under the Income Tax Assessment Act 1936, employers may get income tax deductions for deposits. There is an annual deduction limit of $1,200 per employee.

• Under the Superannuation Guarantee (Administration) Act 1992, deposits made by an employer will be treated as superannuation contributions.

• The accounts may also be credited with Government co‑contributions payable under the Superannuation (Government Co‑contribution for Low Income Earners) Act 2003. The rules for these deposits differ in some respects from those that apply to other deposits.

4 Definitions

In this Act, unless the contrary intention appears:

account means a notional account kept in accordance with section 12.

child, of a person, means a child of the person within the meaning of the Superannuation Industry (Supervision) Act 1993.

complying superannuation fund has the same meaning as in the Income Tax Assessment Act 1997.

Note: The Income Tax Assessment Act 1997 defines complying superannuation fund by reference to section 45 of the Superannuation Industry (Supervision) Act 1993.

dependant, in relation to an individual, includes the spouse and any child of the person.

Note: This expression is only used in the definition of superannuation contribution.

deposit means a payment under section 25.

deposit form means a statement under section 26.

depositor means a person who makes a payment under section 25.

employee has the meaning given by the Schedule.

Note: The Schedule extends the ordinary meaning of employee.

employer has the meaning given by the Schedule.

Note: The Schedule extends the ordinary meaning of employer.

employment has a meaning corresponding to employee and employer.

Government co‑contribution in respect of an individual means a Government co‑contribution payable in respect of the individual under the Superannuation (Government Co‑contribution for Low Income Earners) Act 2003.

leave Australia has the same meaning as in the Migration Act 1958.

person has a meaning affected by sections 87 and 90.

Note 1: Under section 87, partnerships are treated as persons.

Note 2: Under section 90, unincorporated associations are treated as persons.

provider, in relation to an RSA, has the same meaning as in the Retirement Savings Accounts Act 1997.

quarter means a period of 3 months beginning on 1 July, 1 October, 1 January or 1 April in:

(a) the financial year beginning on 1 July 1995; or

(b) any later financial year.

RSA has the same meaning as in the Retirement Savings Accounts Act 1997.

RSA provider has the same meaning as in the Retirement Savings Accounts Act 1997.

Special Account means the Superannuation Holding Accounts Special Account continued in existence by section 8.

spouse of a person includes:

(a) another person (whether of the same sex or a different sex) with whom the person is in a relationship that is registered under a law of a State or Territory prescribed for the purposes of section 22B of the Acts Interpretation Act 1901 as a kind of relationship prescribed for the purposes of that section; and

(b) another person who, although not legally married to the person, lives with the person on a genuine domestic basis in a relationship as a couple.

Note: This expression is only used in the definition of dependant.

superannuation accounts law means:

(a) this Act; and

(b) the regulations; and

(c) Part III of the Taxation Administration Act 1953, in so far as that Part relates to this Act or the regulations.

superannuation contribution, in relation to an individual, means a contribution made to a superannuation fund, an RSA or a superannuation scheme for the purpose of making provision for superannuation benefits for, or for dependants of, the individual.

superannuation fund means a provident, benefit, superannuation or retirement fund.

superannuation scheme means a scheme for the payment of superannuation, retirement or death benefits.

tax file number has the meaning given by section 202A of the Income Tax Assessment Act 1936.

Unallocated Interest Pool means the Unallocated Interest Pool kept in accordance with section 42.

5 Crown to be bound

This Act binds the Crown in right of the Commonwealth, of each of the States, of the Australian Capital Territory, of the Northern Territory and of Norfolk Island.

6 Act to be administered by the Commissioner of Taxation

The Commissioner of Taxation has the general administration of this Act.

Note: An effect of this provision is that people who acquire information under this Act are subject to the confidentiality obligations and exceptions in Division 355 in Schedule 1 to the Taxation Administration Act 1953.

Part 2—Superannuation Holding Accounts Special Account

7 Simplified outline

The following is a simplified outline of this Part:

• The Superannuation Holding Accounts Special Account is continued in existence.

• The Special Account is not a superannuation fund.

8 Superannuation Holding Accounts Special Account

(1) The Superannuation Holding Accounts Account is continued in existence as the Superannuation Holding Accounts Special Account.

Note: The Superannuation Holding Accounts Account was established by subsection 5(3) of the Financial Management Legislation Amendment Act 1999.

(2) The Account is a Special Account for the purposes of the Financial Management and Accountability Act 1997.

Note: An amount standing to the credit of the Special Account may be invested under section 39 of the Financial Management and Accountability Act 1997.

9 Special Account is not a superannuation fund

Special Account is not a superannuation fund

(1) For the purposes of a law of the Commonwealth:

(a) the Special Account is taken not to be a superannuation fund; and

(b) the scheme embodied in this Act is taken not to be a superannuation scheme.

Avoidance of doubt

(2) Subsection (1) is enacted to avoid doubt.

Part 3—Accounts

Division 1—Simplified outline

11 Simplified outline

The following is a simplified outline of this Part:

• Notional accounts are to be kept within the Special Account in the names of particular individuals.

• Section 13 outlines credits to accounts.

• Section 14 outlines debits to accounts.

• The Commissioner of Taxation may open or close an account.

• Accounts may have a nil balance.

• An individual may only have one account.

• Account balances are not held on trust.

• An individual’s account balance will be notified to the individual in certain circumstances.

Division 2—Keeping of accounts

12 Accounts

Accounts to be kept

(1) Separate notional accounts are to be kept within the Special Account in the names of particular individuals.

Individual’s account

(2) An account kept in the name of an individual is to be known as the individual’s account.

Note: Section 4 provides that account means a notional account kept in accordance with this section.

Division 3—Outline of credits and debits to accounts

13 Outline of credits to accounts

The following is a simplified outline of the types of credits that may be made to an individual’s account.

Deposits by employers

• Under section 25, the individual’s employer or former employer may make a deposit in respect of the individual. The employer or former employer will make the deposit instead of making a superannuation contribution in respect of the individual. The deposit will result in a credit to the individual’s account.

Superannuation guarantee shortfalls

• Under section 65 of the Superannuation Guarantee (Administration) Act 1992, if there is a shortfall component of a payment of superannuation guarantee charge in relation to the individual, the Commissioner of Taxation may credit the shortfall component to the individual’s account.

Interest

• Under Part 6, interest may be credited to the individual’s account.

14 Outline of debits to accounts

The following is a simplified outline of the types of debits that may be made to an individual’s account. These debits also involve debiting the Special Account.

Transfer to superannuation fund or RSA

• Under section 61, the balance of the amount standing to the credit of the account may be debited from the Special Account and paid by the Commonwealth to a superannuation fund or RSA.

Balance of less than $200—individual has ceased to be employed by all depositors

• Under section 63, the balance of the amount standing to the credit of the account may be debited from the Special Account and paid by the Commonwealth to the individual if:

(a) the balance is less than $200; and

(b) the individual has ceased to be employed by all depositors.

Receipt of Commonwealth income support payments

• Under section 64, the balance of the amount standing to the credit of the account may be debited from the Special Account and paid by the Commonwealth to the individual if the individual is in receipt of Commonwealth income support payments for a sufficient period.

Disability

• Under section 65, the balance of the amount standing to the credit of the account may be debited from the Special Account and paid by the Commonwealth to the individual if the individual has retired because of permanent disability.

Individual turns 65

• Under section 66, the balance of the amount standing to the credit of the account may be debited from the Special Account and paid by the Commonwealth to the individual if the individual has turned 65.

Individual at least 55 years old and not an Australian resident

• Under section 67, the balance of the amount standing to the credit of the account may be debited from the Special Account and paid by the Commonwealth to the individual if the individual is at least 55 years old and is not an Australian resident for income tax purposes and:

(a) the individual is not in employment; or

(b) the individual is in employment, but the duties of the individual’s employment are performed wholly or principally outside Australia.

Former temporary resident

• The balance of the amount standing to the credit of an individual’s account may be debited from the Special Account if the individual is a former temporary resident.

Death of individual

• Under section 68, if the individual dies, the balance of the amount standing to the credit of the account may be debited from the Special Account and paid by the Commonwealth to the individual’s legal personal representative.

Refunds of deposits

• Under Part 8, an amount standing to the credit of the account may be debited from the Special Account and paid by the Commonwealth for the purposes of refunding deposits that were:

(a) accompanied by false or defective deposit forms; or

(b) made by mistake.

Division 4—Opening and closing of accounts

15 Opening of accounts

Power

(1) The Commissioner of Taxation may open an account in the name of a particular individual.

Duty

(2) The Commissioner of Taxation must open an account in the name of a particular individual if:

(a) the individual does not already have an account; and

(b) a person makes a deposit, or a purported deposit, in respect of the individual.

Payment split under Family Law Act

(3) If an account is subject to a payment split, then the Commissioner may open an account in the name of the non‑member spouse.

(4) The balance of the account when it is opened is an amount worked out in accordance with the regulations.

(5) The balance of the member spouse’s account is to be reduced by the amount worked out under subsection (4).

(6) The Commissioner must give the member spouse a written notice setting out the balance (if any) of the member spouse’s account after the reduction.

(7) In this section:

member spouse has the same meaning as in Part VIIIB of the Family Law Act 1975.

non‑member spouse has the same meaning as in Part VIIIB of the Family Law Act 1975.

payment split means a payment split under Part VIIIB of the Family Law Act 1975.

16 Closing of accounts

The Commissioner of Taxation may close an individual’s account if the balance of the account is nil and:

(a) the balance of the account was nil throughout the preceding period of 2 years; or

(b) the balance of the account has been withdrawn under section 61, 65, 66, 67, 67A or 91E; or

(c) the individual has died; or

(d) the individual asks the Commissioner of Taxation to close the account; or

(e) the balance of the account has been debited from the Special Account under Part 9 (which deals with inactive accounts).

Note 1: Section 61 deals with individuals who request transfer of account balances to RSAs or superannuation funds.

Note 2: Section 65 deals with individuals who retire because of disability.

Note 3: Section 66 deals with individuals who have turned 65.

Note 4: Section 67 deals with individuals who are not Australian residents for income tax purposes etc.

Note 5: Section 67A deals with individuals who have permanently departed from Australia.

Note 6: Section 91E deals with debiting of accounts to recover overpayments of Government co‑contributions.

Division 5—Rules about accounts

17 Accounts may have a nil balance

Nil balance

(1) An account may have a nil balance.

Examples

(2) The following are examples of cases where an account might have a nil balance:

(a) no money has been credited to the account;

(b) the balance of the account has been withdrawn under Part 7;

(c) the balance of the account has been refunded to an employer or former employer under Part 8;

(d) the balance of the account has been debited from the Special Account under Part 9 (which deals with inactive accounts).

18 One account per individual

Only one account

(1) Only one account may be kept in respect of a particular individual.

Amalgamation etc.

(2) A contravention of subsection (1) does not affect the validity of an account. However, if the Commissioner of Taxation becomes aware that 2 or more accounts are being kept in respect of the same individual, the Commissioner of Taxation must amalgamate the accounts into a single account.

19 Account balances not held on trust etc.

(1) Money credited to an individual’s account:

(a) is not held on trust; and

(b) is not special public money for the purposes of section 16 of the Financial Management and Accountability Act 1997.

(2) The Commonwealth is not liable to pay, repay or refund money credited to an individual’s account except as provided by this Act.

Note: Under section 69A of the Superannuation Guarantee (Administration) Act 1992, if a shortfall component of superannuation guarantee charge has been incorrectly credited to an individual’s account, the account may be debited for the purposes of reversing the credit.

Division 6—Notification of account balances

20 Notification of opening balance

As soon as practicable after the first occasion on which an amount is credited to an individual’s account, the Commissioner must give the individual a written notice setting out the balance of the account.

21 Individual may request details of account balance

When section applies

(1) This section applies to an individual’s account if the individual asks the Commissioner of Taxation to give the individual a written notice setting out the balance of the account.

Form of request

(2) The request must be:

(a) in writing; and

(b) in a form approved in writing by the Commissioner of Taxation.

Compliance with request

(3) The Commissioner of Taxation must comply with the request.

22 Annual notification of account balance

When section applies

(1) This section applies to an individual’s account if:

(a) the balance of the account exceeds nil as at the end of a financial year; and

(b) the individual’s current address is known to the Commissioner of Taxation.

Notification

(2) As soon as practicable after the end of the financial year, the Commissioner of Taxation must give the individual a written notice setting out the balance of the account as at the end of the financial year.

23 Notification when account balance reaches $1,200

When section applies

(1) This section applies to an individual’s account if:

(a) a particular credit to the account increases the balance of the account from a figure of less than $1,200 to a figure of $1,200 or more; and

(b) the individual’s current address is known to the Commissioner of Taxation.

Notification

(2) As soon as practicable after the credit is made, the Commissioner of Taxation must give the individual a written notice:

(a) setting out the balance of the account; and

(b) explaining the effect of sections 49 and 61; and

(c) suggesting that the individual make a request under section 61.

Note 1: Section 49 imposes a limit on the accrual of interest to accounts with balances of more than $1,200.

Note 2: Section 61 provides for the transfer of the balance of the account to a superannuation fund.

Part 4—Deposits

24 Simplified outline

The following is a simplified outline of this Part:

• A person may make a payment to the Commissioner of Taxation under section 25 in respect of an individual. The payment is called a deposit.

• The deposit must be accompanied by a deposit form.

• The deposit form must include certain declarations.

• The 2 key declarations are:

(a) that the depositor is the employer, or former employer, of the individual; and

(b) that the depositor is making the deposit instead of making a superannuation contribution in respect of the individual.

• A defect in the deposit form will not result in the invalidity of the deposit.

• A deposit form may deal with multiple payments.

• Deposits are not held on trust.

25 Deposits

A person (the depositor) may make a payment (the deposit) to the Commissioner of Taxation under this section in respect of an individual if, and only if, the payment is made before 1 July 2006.

26 Deposit to be accompanied by deposit form

The deposit must be accompanied by a written statement (the deposit form) that:

(a) is in a form approved in writing by the Commissioner of Taxation; and

(b) contains the information required by the form to be given; and

(c) contains the declarations required by sections 27, 28, 29 and 30; and

(d) sets out the individual’s tax file number (if known to the depositor); and

(e) is signed by or on behalf of the depositor.

27 Deposit to be made by employer or former employer

The deposit form must include a declaration that the depositor is the employer, or former employer, of the individual.

28 Deposit to be instead of superannuation contributions

The deposit form must include a declaration that the depositor is making the deposit:

(a) in respect of the employment, or former employment, of the individual by the depositor; and

(b) instead of making a superannuation contribution:

(i) in respect of the individual; and

(ii) of an amount equal to the deposit.

29 Deposit to be consistent with other laws etc.

The deposit form must include a declaration that, to the best of the knowledge of the depositor, the making of the deposit does not contravene:

(a) a law of the Commonwealth (other than this Act) or a law of a State or Territory; or

(b) an award, order, determination or industrial agreement in force under such a law; or

(c) a legally enforceable agreement.

30 Age limit

The deposit form must include a declaration that, to the best of the knowledge of the depositor, the individual was under 70 on at least one day during the period of employment to which the deposit relates.

31 Consequences of false declarations etc.

If the deposit is accompanied by a deposit form, or a purported deposit form, that:

(a) contains a declaration, or information, that is false or misleading; or

(b) has some other defect or irregularity;

that circumstance does not result in the invalidity of the deposit. However, it may result in the deposit being refunded under Part 8.

Note 1: A false or misleading statement may result in criminal liability under Part III of the Taxation Administration Act 1953.

Note 2: A false or misleading declaration may result in an employer being denied:

(a) an income tax deduction under section 82AAF of the Income Tax Assessment Act 1936; and

(b) concessional treatment under section 23 of the Superannuation Guarantee (Administration) Act 1992.

32 Deposit form may deal with multiple payments

Multiple payments

(1) A deposit form may deal with 2 or more payments made by the same person (whether the payments are made in respect of the same individual or in respect of different individuals).

Method of payment

(2) If a deposit form deals with 2 or more payments made by the same person, the person may give the Commissioner of Taxation, in respect of the sum of the payments:

(a) one or more valid cheques; or

(b) one or more money orders; or

(c) cash; or

(d) any combination of the above.

If the person does so, this Act has effect as if the person had given the Commissioner of Taxation a separate cheque for each of the payments.

33 Deposit not held on trust etc.

(1) A deposit, or purported deposit, made in respect of an individual:

(a) is not held on trust; and

(b) is not special public money for the purposes of section 16 of the Financial Management and Accountability Act 1997.

(2) A deposit, or purported deposit, made in respect of an individual is not repayable or refundable except as provided by this Act.

Part 5—Crediting of deposits

34 Simplified outline

The following is a simplified outline of this Part:

Deposits are to be credited to accounts by following these steps:

• credit the deposit to the Special Account;

• credit the deposit to the individual’s account.

35 Crediting of deposits

Step 1—Credit to Special Account

(1) An amount equal to a deposit or purported deposit made in respect of an individual is to be credited to the Special Account.

Step 2—Credit to individual’s account

(2) As soon as practicable after the amount is credited to the Special Account, the individual’s account is to be credited with an amount equal to the deposit or purported deposit.

Part 6—Crediting of interest

Division 1—Simplified outline

36 Simplified outline

The following is a simplified outline of this Part:

• Interest is funded by crediting amounts to the Special Account.

• Interest accrues to an account on the daily balance of the account. Interest only accrues on the first $1,200 of the balance of the account.

• Interest is credited each quarter on the allocation day.

• The allocation day is published in the Gazette.

• The rate at which interest accrues is called the allocation rate.

• The allocation rate is published in the Gazette.

• Interest will not accrue to an account in the following cases:

(a) a deposit is refunded;

(b) a shortfall component is incorrectly credited to the account;

(c) the $1,200 limit has been avoided by the use of multiple accounts.

Division 2—Gross interest amount and net interest amount

37 Simplified outline

The following is a simplified outline of this Division:

• The expressions gross interest amount and net interest amount are defined.

• Those expressions are used to work out:

(a) how interest is funded; and

(b) the rate at which interest accrues to an account.

38 Gross interest amount

For the purposes of this Part, the gross interest amount for a quarter is the sum of the following amounts:

(a) the income derived by the Commonwealth during the quarter from the investment of amounts standing to the credit of the Special Account;

(b) the amount (if any) determined by the Minister for Finance in relation to the quarter having regard to the amount standing to the credit of the Special Account that remains uninvested from time to time during the quarter.

39 Net interest amount

Net interest amount

(1) For the purposes of this Part, the net interest amount for a quarter is the gross interest amount for the quarter, reduced (but not below 0) by the sum of:

(a) the amount determined by the Commissioner of Taxation, where the amount represents a fair approximation of the costs incurred by the Commonwealth during the quarter in connection with the administration of this Act; and

(b) the amount, or the total of the amounts, allocated to the quarter under subsection (3).

Note: Gross interest amount is defined by section 38.

Carry‑forward amount

(2) For the purposes of this section, if:

(a) the amount determined under paragraph (1)(a) in relation to a quarter;

exceeds:

(b) the gross interest amount for the quarter;

the excess is taken to be the carry‑forward amount for the quarter.

Note: Gross interest amount is defined by section 38.

Allocation of carry‑forward amounts

(3) For the purposes of this section, the Minister for Finance may determine that:

(a) a carry‑forward amount for a quarter is to be allocated to a later quarter; or

(b) different parts of the carry‑forward amount for a quarter are to be allocated to different later quarters.

Amortisation

(4) For the purposes of this section, capital costs and development costs are to be amortised in accordance with generally accepted accounting principles.

Investment costs

(5) For the purposes of this section, the costs incurred by the Commonwealth in connection with the investment of amounts standing to the credit of the Special Account are taken to have been incurred in connection with the administration of this Act.

Division 3—Funding of interest

40 Simplified outline

The following is a simplified outline of this Division:

• Interest is funded by crediting the net interest amount to the Special Account.

• An Unallocated Interest Pool is to be kept within the Special Account.

• Unallocated interest is represented by the balance of the Unallocated Interest Pool.

• In special cases, the Unallocated Interest Pool may be supplemented by crediting an amount to the Special Account.

• Since interest only accrues on the first $1,200 of an account balance, it is possible for a surplus to build up in the Unallocated Interest Pool. The surplus can be debited from the Special Account.

41 Crediting of net interest amount to the Special Account

As soon as practicable after the end of a quarter, an amount equal to the net interest amount for the quarter is to be credited to the Special Account.

Note: Net interest amount is defined by section 39.

42 Unallocated Interest Pool

Pool

(1) For accounting purposes, a separate notional subcomponent, called the Unallocated Interest Pool, is to be kept within the Special Account.

Credits to Pool

(2) An amount credited to the Special Account under section 41 is to be credited to the Unallocated Interest Pool.

Debits from Pool

(3) The balance of the Unallocated Interest Pool is to be debited for the purposes of crediting interest to an individual’s account.

43 Supplementation of Unallocated Interest Pool

When section applies

(1) This section applies if the Minister for Finance is satisfied that:

(a) the balance of the Unallocated Interest Pool is nil; or

(b) the balance of the Unallocated Interest Pool is, or is likely to be, insufficient to meet the requirements of the Unallocated Interest Pool.

Supplementation

(2) The Minister for Finance may determine that the Unallocated Interest Pool is to be supplemented by a specified amount.

Crediting of the supplementation amount

(3) The specified amount is to be credited to the Special Account.

Credit to Unallocated Interest Pool

(4) The Unallocated Interest Pool is to be credited by the specified amount.

44 Debiting of unallocated interest

(1) If the Commissioner of Taxation is satisfied that the balance of the Unallocated Interest Pool exceeds the requirements of the Unallocated Interest Pool, the Commissioner of Taxation must determine that the excess is surplus to the requirements of the Unallocated Interest Pool.

(2) The Unallocated Interest Pool is to be debited by an amount equal to the excess.

(3) An amount equal to the excess is to be debited from the Special Account.

Division 4—Allocation day and allocation rate

45 Simplified outline

The following is a simplified outline of this Division:

• The allocation day for a quarter is published in the Gazette. The allocation day is the day on which interest is credited to accounts.

• The allocation rate for a quarter is published in the Gazette. The allocation rate is the rate at which interest accrues to an account.

• The allocation rate is worked out under section 47.

46 Gazettal of allocation day and allocation rate

(1) As soon as practicable after an amount is credited to the Special Account under section 41 in respect of a quarter (the current quarter), the Commissioner of Taxation must, by notice published in the Gazette, declare that, for the purposes of this Part:

(a) a specified day in the quarter next following the current quarter is the allocation day for the current quarter; and

(b) a specified percentage is the allocation rate for the current quarter.

Note: To work out the allocation rate see section 47.

(2) The declaration has effect accordingly.

47 Calculation of the allocation rate

Application of steps

(1) To work out the allocation rate for a quarter, apply the following steps.

Adjusted total balances

(2) Calculate the adjusted total balances for the quarter by:

(a) working out, for each day in the quarter, the total balances of all the accounts; and

(b) adding up those totals; and

(c) dividing the result by the number of days in the quarter.

For the purposes of this calculation, if an account balance actually exceeds $1,200, the account balance is taken to be $1,200.

Provisional rate

(3) Calculate the provisional rate for the quarter as a percentage (to 4 decimal places) using the formula:

where:

Net interest amount means the net interest amount for the quarter;

Adjusted total balances means the adjusted total balances for the quarter.

Note: Net interest amount is defined by section 39.

Total balances

(4) Calculate the total balances for the quarter by:

(a) working out, for each day in the quarter, the total balances of all the accounts; and

(b) adding up those totals; and

(c) dividing the result by the number of days in the quarter.

Capped rate

(5) Calculate the capped rate as a percentage (to 4 decimal places) using the formula:

where:

Gross interest amount means the gross interest amount for the quarter;

Total balances means the total balances for the quarter.

Note: Gross interest amount is defined by section 38.

Allocation rate—comparison between provisional rate and capped rate

(6) Compare the provisional rate with the capped rate:

(a) if the provisional rate is less than or equal to the capped rate—the allocation rate equals the provisional rate; or

(b) if the provisional rate exceeds the capped rate—the allocation rate equals the capped rate.

Division 5—Crediting of interest

48 Simplified outline

The following is a simplified outline of this Division:

• Interest accrues to an account on the daily balance of the account. Interest only accrues on the first $1,200 of the balance of the account.

• Interest is credited each quarter on the allocation day.

49 Accrual of interest on first $1,200 of daily balance

(1) Interest accrues to an account each day on the balance of the account as at the end of that day.

(2) For the purposes of this Division, if an account balance actually exceeds $1,200, the account balance is taken to be $1,200.

50 Rate of accrual, and crediting, of interest

When section applies

(1) This section applies to interest that accrues under section 49.

Allocation day event, withdrawal event and inactive account debit event

(2) Both:

(a) the rate of accrual of interest to an account in respect of a particular day (the accrual day) in a particular quarter; and

(b) the time at which accrued interest in respect of the accrual day is to be credited to the account;

depends on whichever of the following events first happens after the accrual day:

(c) the occurrence of the allocation day for the quarter (this event is to be known as the allocation day event);

(d) the withdrawal under Part 7 of the balance of the account (this event is to be known as the withdrawal event);

(e) the debiting of the balance of the account from the Special Account under Part 9 (this event is to be known as the inactive account debit event).

Allocation day event

(3) If the allocation day event comes first:

(a) the rate of accrual is the percentage worked out (to 6 decimal places) using the formula:

where:

Allocation rate means the allocation rate for the quarter; and

(b) the accrued interest is to be credited to the account on the allocation day.

Withdrawal event

(4) If the withdrawal event comes first:

(a) the rate of accrual is the percentage worked out (to 6 decimal places) using the formula:

where:

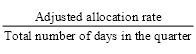

Adjusted allocation rate means the last allocation rate that was published in the Gazette before the accrual day; and

(b) the accrued interest is to be credited to the account on the day before the day of the withdrawal.

Inactive account debit event

(5) If the inactive account debit event comes first:

(a) the rate of accrual is the percentage worked out (to 6 decimal places) using the formula:

where:

Adjusted allocation rate means the last allocation rate that was published in the Gazette before the accrual day; and

(b) the accrued interest is to be credited to the account on the day of the debit.

Transitional—withdrawal event before first allocation day

(6) Despite paragraph (4)(a), if the withdrawal event occurs before the allocation day for the quarter beginning on 1 July 1995, that paragraph has effect, in relation to that event, as if the adjusted allocation rate were 0.4% or such higher rate as the Minister for Finance determines.

51 Rounding up

If the total amount of interest to be credited to an account on a particular day (when expressed as a number of cents) is not a number of whole cents, that total must be rounded up to the nearest cent.

Division 6—Interest not to accrue in certain cases

52 Simplified outline

The following is a simplified outline of this Division:

• Interest will not accrue to an account in the following cases:

(a) a deposit is refunded;

(b) a shortfall component is incorrectly credited to the account;

(c) the $1,200 limit has been avoided by the use of multiple accounts.

53 Interest does not accrue on refunded deposits

No interest

(1) Despite section 49, interest does not accrue, and is taken never to have accrued, under that section in respect of so much of the balance of an account as is refunded under Part 8.

Reversing interest credit

(2) If interest has been credited to an individual’s account in contravention of subsection (1), the Commissioner of Taxation must debit the account by the amount of the credit. The debit must be made before the account balance is debited by the amount of the refund payment.

Unallocated Interest Pool to be credited

(3) The Unallocated Interest Pool is to be credited by the amount of a debit under subsection (2).

54 Interest does not accrue on shortfall components incorrectly credited to accounts

When section applies

(1) This section applies if:

(a) an amount credited to an account under section 65 of the Superannuation Guarantee (Administration) Act 1992 exceeds the amount that should have been credited to the account; and

(b) the balance of the account is attributable, in whole or in part, to the credit.

No interest

(2) Despite section 49, interest does not accrue, and is taken never to have accrued, under that section in respect of so much of the balance of the account as is attributable to the excess.

Debit reversing interest credit

(3) If interest has been credited to the account in contravention of subsection (2), the Commissioner of Taxation must debit the account by the amount of the credit.

Unallocated Interest Pool to be credited

(4) The Unallocated Interest Pool is to be credited by the amount of a debit under subsection (3).

55 Amalgamated accounts—no interest if $1,200 limit avoided

When section applies

(1) This section applies if:

(a) the Commissioner becomes aware that 2 or more accounts (the separate accounts) are being kept in respect of the same individual; and

(b) the Commissioner of Taxation amalgamates the separate accounts into a single account; and

(c) immediately after the amalgamation, the balance of the amalgamated account exceeds $1,200.

Note: Section 18 empowers the Commissioner to amalgamate the separate accounts.

No interest if $1,200 limit avoided

(2) If, because of the $1,200 limit referred to in subsection 49(2):

(a) the total amount of interest that accrued to the separate accounts before the day of the amalgamation;

exceeds:

(b) the total amount of interest that would have accrued to the amalgamated account if it were assumed that the amalgamated account had been in existence at all times since the earliest time at which any of the separate accounts was opened;

then, despite section 49, the excess interest is taken never to have accrued under that section.

Debit to amalgamated account

(3) If excess interest has been credited in contravention of subsection (2), the Commissioner of Taxation must debit the amalgamated account by an amount equal to the amount of the credit.

Credit to Unallocated Interest Pool

(4) The Unallocated Interest Pool is to be credited by the amount of a debit under subsection (3).

Part 7—Withdrawal of account balances

Division 1—Simplified outline

56 Simplified outline

The following is a simplified outline of this Part:

• There are 3 types of withdrawals of account balances:

(a) transfers of account balances to superannuation funds or RSAs;

(b) direct withdrawals of account balances by individuals;

(c) withdrawals of account balances after death.

• Under Part 8, a depositor has 14 days to apply for a refund of a deposit on the grounds that the deposit was made by mistake. During the 14‑day period, the individual’s account will be frozen.

Division 2—No withdrawals for 14 days after deposit credited to account etc.

57 Simplified outline

The following is a simplified outline of this Division:

• An individual’s account will be frozen for 14 days after a deposit is credited to the account.

• The delay gives the depositor a chance to apply for a refund of the deposit.

• If the depositor applies for a refund of the deposit, the 14‑day period will be extended until the application is finalised.

• Accounts will be frozen for 14 days after a shortfall component is credited to the account.

• The delay gives the Commissioner of Taxation a chance to correct mistakes.

58 No withdrawals for 14 days after deposit credited to account etc.

When section applies

(1) This section applies to an individual’s account if:

(a) a deposit, or purported deposit, was made in respect of the individual; and

(b) as a result of the deposit or purported deposit, an amount was credited to the account under Part 5 at a particular time (the deposit time); and

(c) a request under this Part (the individual’s request) is made during the period of 14 days beginning at the deposit time.

Individual’s request frozen for 14 days

(2) The individual’s request has no effect at any time during that 14‑day period.

Note: This gives the depositor a chance to apply for a refund of the deposit.

Individual’s request frozen for additional period

(3) If an application for a refund of the deposit or purported deposit was made under section 73 during that 14‑day period, then:

(a) if the refund application is granted—the individual’s request has no effect at any time; or

(b) if the refund application is refused—the individual’s request has no effect at a particular time if:

(i) the time is after the refund application is made but before the end of the period of 21 days after the giving of the notice of refusal; or

(ii) if, during that 21‑day period, the refund applicant asks the Commissioner of Taxation to reconsider the refund application—the time is during the period when that reconsideration, or any later application to the Administrative Appeals Tribunal, has not been finalised.

When reconsiderations finalised

(4) For the purposes of this section, a reconsideration of a decision is taken not to have been finalised during the period of 28 days after:

(a) if, because of the operation of subsection 82(5), the decision is taken to be confirmed—the day on which the decision is taken to have been confirmed; or

(b) in any other case—the day on which the decision on the reconsideration is notified to the refund applicant.

59 No withdrawals for 14 days after shortfall component credited to account

When section applies

(1) This section applies to an individual’s account if:

(a) an amount was credited to the account under section 65 of the Superannuation Guarantee (Administration) Act 1992 at a particular time (the credit time); and

(b) a request under this Part is made during the period of 14 days beginning at the credit time.

Request frozen for 14 days

(2) The request has no effect at any time during that 14‑day period.

Note: This gives the Commissioner a chance to correct mistakes.

Division 3—Timing of withdrawals

60 Timing of withdrawals

24‑hour delay

(1) If a request is made under this Part, the Commissioner of Taxation must wait at least 24 hours before complying with the request.

Note: This delay enables interest to be credited to the account.

When withdrawal occurs

(2) For the purposes of this Act, the balance of an account is taken to have been withdrawn at the time when a payment is made under this Part in respect of the account.

Division 4—Transfer of account balances to RSAs and superannuation funds

61 Transfer to RSA or superannuation fund

Transfer request

(1) This section applies to an individual’s account if:

(a) the individual gives the Commissioner of Taxation a request (the transfer request) to transfer the account balance to a specified RSA or to the trustee of a specified fund for the benefit of the individual; and

(b) the fund passes the compliance test set out in subsection (2).

Note: Subsection (7) provides for the transfer request to be given by the individual personally or by the trustee acting on behalf of the individual.

Compliance test for funds

(2) For the purposes of this section, a fund passes the compliance test if:

(a) the fund is an exempt public sector superannuation scheme within the meaning of the Superannuation Industry (Supervision) Act 1993; or

(b) at the time of the transfer request, the Commissioner of Taxation has obtained a written statement, provided by or on behalf of the trustee of the fund, that the fund:

(i) is a regulated superannuation fund within the meaning of the Superannuation Industry (Supervision) Act 1993; and

(ii) is not subject to a direction under section 63 of that Act.

Note: Section 63 of the Superannuation Industry (Supervision) Act 1993 deals with funds that have been directed not to accept contributions from an employer‑sponsor.

Form of transfer request

(3) The transfer request must be:

(a) in writing; and

(b) in a form approved in writing by the Commissioner of Taxation.

Compliance with transfer request

(4) The Commissioner of Taxation must pay to the provider of the RSA, or to the trustee, for the benefit of the individual, an amount equal to the account balance immediately before the payment is made. However, this rule does not apply if the Commissioner of Taxation is satisfied that the RSA provider or the trustee is unwilling to accept the payment.

Special Account to be debited

(5) The Special Account is debited for the purposes of making the payment.

Individual’s account to be debited

(6) When the payment is made, the individual’s account is debited by the amount of the payment.

Authorisation of trustee by individual etc.

(7) The transfer request may be given by:

(a) the individual personally; or

(b) the RSA provider or the trustee acting on the individual’s behalf in accordance with an authority given by the individual.

If paragraph (b) applies, the transfer request must be accompanied by a copy of the authority.

Form of authorisation

(8) An authority referred to in subsection (7) must be:

(a) in writing; and

(b) in a form approved in writing by the Commissioner of Taxation.

Definitions

(9) In this section:

fund includes a public sector superannuation scheme within the meaning of the Superannuation Industry (Supervision) Act 1993.

trustee has the same meaning as in the Superannuation Industry (Supervision) Act 1993.

61A Commissioner may transfer account balance to RSA or superannuation fund

(1) The Commissioner of Taxation may pay the balance of an individual’s account to:

(a) an RSA of the individual; or

(b) the trustee of a complying superannuation fund for crediting to an account of the individual within that fund.

(2) To avoid doubt, the Commissioner of Taxation may make the payment under subsection (1) without a request from the individual under section 61.

(3) The Special Account is debited for the purposes of making the payment under subsection (1).

(4) When the payment under subsection (1) is made, the individual’s account is debited by the amount of the payment.

(5) In this section:

trustee of a superannuation fund means:

(a) if there is a trustee (within the ordinary meaning of that expression) of the fund—the trustee; or

(b) otherwise—the person who manages the fund.

Division 5—Direct withdrawals of account balances by individuals

62 Simplified outline

The following is a simplified outline of this Division:

• The balance of an individual’s account may be withdrawn if:

(a) the balance is less than $200; and

(b) the individual has ceased to be employed by all depositors.

• The balance of an individual’s account may be withdrawn if the individual is in receipt of Commonwealth income support payments for a sufficient period.

• The balance of an individual’s account may be withdrawn if the individual has retired because of permanent disability.

• The balance of an individual’s account may be withdrawn if the individual has turned 65.

• The balance of an individual’s account may be withdrawn if the individual is at least 55 years old and is not an Australian resident for income tax purposes and:

(a) the individual is not in employment; or

(b) the individual is in employment, but the duties of the individual’s employment are performed wholly or principally outside Australia.

• The balance of an individual’s account may be withdrawn if the individual is a former temporary resident.

63 Withdrawal of account balance of less than $200, where individual has ceased to be employed by depositor etc.

Withdrawal request

(1) This section applies to an individual’s account if:

(a) the balance of the account is attributable, in whole or in part, to:

(i) one or more deposits, or purported deposits, made by one or more employers or former employers of the individual; or

(ii) one or more shortfall components of payments of superannuation guarantee charge made by one or more employers or former employers of the individual; and

(b) the individual satisfies the Commissioner of Taxation that the individual has ceased to be employed by each of the employers or former employers; and

(c) the individual gives the Commissioner of Taxation a request (the withdrawal request) for the withdrawal of the account balance; and

(d) the balance of the account is less than $200 immediately before the time when the account balance is withdrawn.

Form of withdrawal request

(2) The withdrawal request must be:

(a) in writing; and

(b) in a form approved in writing by the Commissioner of Taxation.

Compliance with withdrawal request

(3) The Commissioner of Taxation must pay to the individual an amount equal to the account balance immediately before the payment is made.

Special Account to be debited

(4) The Special Account is debited for the purposes of making the payment.

Individual’s account to be debited

(5) When the payment is made, the individual’s account is debited by the amount of the payment.

64 Withdrawal of account balance—receipt of Commonwealth income support payments

Withdrawal request

(1) This section applies to an individual’s account if:

(a) the individual gives the Commissioner of Taxation a request (the withdrawal request) for the withdrawal of the account balance; and

(b) the individual has been in receipt of one or more Commonwealth income support payments for:

(i) if the person is at least 55 years of age—a period of at least 39 weeks, or for 2 or more periods that total at least 39 weeks, since the person turned 55; or

(ii) in any case—for an unbroken period of at least 26 weeks (other than such a period that ended before the withdrawal request was given); and

(c) the individual gives the Commissioner of Taxation:

(i) written evidence of the individual’s receipt of relevant Commonwealth income support payments provided by the Commonwealth Department or agency that is responsible for administering the payment; or

(ii) such other evidence of the individual’s receipt of relevant Commonwealth income support payments as is prescribed.

Form of withdrawal request

(2) The withdrawal request must be:

(a) in writing; and

(b) in a form approved in writing by the Commissioner of Taxation.

Compliance with withdrawal request

(3) The Commissioner of Taxation must pay to the individual an amount equal to the account balance immediately before the payment is made.

Special Account to be debited

(4) The Special Account is debited for the purposes of making the payment.

Individual’s account to be debited

(5) When the payment is made, the individual’s account is debited by the amount of the payment.

(6) For the purposes of subparagraph (1)(b)(ii), if an individual obtains evidence covered by subparagraph (1)(c)(i), the individual is, subject to evidence to the contrary, to be taken to have continued to have received the Commonwealth income support payment concerned for 21 days after the date of the written evidence.

(7) In this section:

Commonwealth income support payment means:

(a) any of the following payments (as defined in section 23 of the Social Security Act 1991):

(i) a social security benefit (other than an austudy payment or a youth allowance paid to a person who is undertaking full‑time study);

(ii) a social security pension;

(iii) a service pension;

(iv) an income support supplement; or

(b) a drought relief payment under the Farm Household Support Act 1992 as in force immediately before the commencement of the Farm Household Support Amendment (Restart and Exceptional Circumstances) Act 1997; or

(c) an exceptional circumstances relief payment under the Farm Household Support Act 1992; or

(d) a payment of salary or wages made under the employment scheme of the Commonwealth that is known as the Community Development Employment Projects Scheme; or

(e) any other payment prescribed for the purposes of this definition.

65 Withdrawal of account balance—retirement on grounds of disability

Withdrawal request

(1) This section applies to an individual’s account if:

(a) the individual gives the Commissioner of Taxation a request (the withdrawal request) for the withdrawal of the account balance; and

(b) the individual satisfies the Commissioner of Taxation that the individual is not in employment; and

(c) the individual last ceased to be an employee because of the disability of the individual; and

(d) 2 legally qualified medical practitioners have certified that the disability is likely to result in the individual being unable ever to be employed in a capacity for which the individual is reasonably qualified because of education, training or experience.

Form of withdrawal request

(2) The withdrawal request must be:

(a) in writing; and

(b) in a form approved in writing by the Commissioner of Taxation.

Compliance with withdrawal request

(3) The Commissioner of Taxation must pay to the individual an amount equal to the account balance immediately before the payment is made.

Special Account to be debited

(4) The Special Account is debited for the purposes of making the payment.

Individual’s account to be debited

(5) When the payment is made, the individual’s account is debited by the amount of the payment.

66 Withdrawal of account balance—individual turns 65

When section applies

(1) This section applies to an individual’s account if the individual has turned 65.

Withdrawal decision

(2) The Commissioner of Taxation may decide to pay to the individual an amount equal to the balance of the account immediately before the payment is made.

Withdrawal request

(3) The individual may give the Commissioner of Taxation a request (the withdrawal request) to make a payment under subsection (2).

Form of withdrawal request

(4) The withdrawal request must be:

(a) in writing; and

(b) in a form approved in writing by the Commissioner of Taxation.

Compliance with withdrawal request

(5) The Commissioner of Taxation must comply with the withdrawal request.

Special Account to be debited

(6) The Special Account is debited for the purposes of making the payment.

Individual’s account to be debited

(7) When the payment is made, the individual’s account is debited by the amount of the payment.

67 Withdrawal of account balance—individual not an Australian resident

Withdrawal request

(1) This section applies to an individual’s account if:

(a) the individual gives the Commissioner of Taxation a request (the withdrawal request) for the withdrawal of the account balance; and

(b) the individual satisfies the Commissioner of Taxation that the individual is not a resident (within the meaning of the Income Tax Assessment Act 1936); and

(ba) the individual is at least 55 years old when he or she gives the withdrawal request; and

(c) the individual satisfies the Commissioner of Taxation that:

(i) the individual is not in employment; or

(ii) the individual is in employment, but the duties of the individual’s employment are performed wholly or principally outside Australia.

Note: Australia is defined by subsection (6).

Form of withdrawal request

(2) The withdrawal request must be:

(a) in writing; and

(b) in a form approved in writing by the Commissioner of Taxation.

Compliance with withdrawal request

(3) The Commissioner of Taxation must pay to the individual an amount equal to the account balance immediately before the payment is made.

Special Account to be debited

(4) The Special Account is debited for the purposes of making the payment.

Individual’s account to be debited

(5) When the payment is made, the individual’s account is debited by the amount of the payment.

Definition

(6) In this section:

Australia has the same meaning as in the Income Tax Assessment Act 1936.

67A Withdrawal of account balance—former temporary resident

Withdrawal request

(1) This section applies to an individual’s account if:

(a) the individual gives the Commissioner of Taxation a request (the withdrawal request) for the withdrawal of the account balance; and

(b) the individual satisfies the Commissioner of Taxation that before, on or after the commencement of this section, the individual:

(i) was, under the Migration Act 1958, the holder of a temporary visa that has ceased to be in effect; and

(ii) left Australia after starting to be the holder of the visa (whether the visa ceased to be in effect before, when or after the person left); and

(c) the individual satisfies the Commissioner of Taxation that the individual:

(i) is not, under the Migration Act 1958, the holder of a permanent visa; and

(ii) is neither an Australian citizen nor a New Zealand citizen.

Form of withdrawal request

(2) The withdrawal request must be:

(a) in writing; and

(b) in a form approved in writing by the Commissioner of Taxation.

Compliance with withdrawal request

(3) The Commissioner of Taxation must pay to the individual an amount equal to the account balance immediately before the payment is made.

Special Account to be debited

(4) The Special Account is debited for the purposes of making the payment.

Individual’s account to be debited

(5) When the payment is made, the individual’s account is debited by the amount of the payment.

Division 6—Withdrawals of account balances after death

68 Withdrawal of account balance—death of individual

Withdrawal request

(1) This section applies to an individual’s account if:

(a) the individual has died; and

(b) the individual’s legal personal representative gives the Commissioner of Taxation a request (the withdrawal request) for the withdrawal of the account balance.

Form of withdrawal request

(2) The withdrawal request must be:

(a) in writing; and

(b) in a form approved in writing by the Commissioner of Taxation.

Compliance with withdrawal request

(3) The Commissioner of Taxation must pay to the legal personal representative an amount equal to the account balance immediately before the payment is made.

Special Account to be debited

(4) The Special Account is debited for the purposes of making the payment.

Individual’s account to be debited

(5) When the payment is made, the individual’s account is debited by the amount of the payment.

Division 7—Notification of refusal of requests

69 Notification of refusal of requests

(1) This section applies if:

(a) a person makes a request under this Part; and

(b) the Commissioner of Taxation refuses the request.

(2) The Commissioner of Taxation must give the person written notice of the refusal.

Division 8—Recovery of account balances

70 Recovery of account balances

If a person is entitled to be paid an amount by the Commissioner of Taxation under this Part, the amount may be recovered, as a debt due to the person by the Commonwealth, by action in a court of competent jurisdiction.

Part 8—Refunds of deposits

71 Simplified outline

The following is a simplified outline of this Part:

• The Commissioner of Taxation may refund a deposit if the deposit form was false or defective.

• A depositor may apply for the refund of a deposit if it was made by mistake. The refund application must be made within 14 days after the deposit was credited to the account.

72 Refunds—false or defective deposit forms etc.

When section applies

(1) This section applies if:

(a) a deposit or purported deposit was made in respect of an individual; and

(b) the individual’s account was credited with an amount equal to the deposit or purported deposit; and

(c) the credit was made in consequence of the deposit or purported deposit; and

(d) the deposit or purported deposit was accompanied by a deposit form, or a purported deposit form, that, in so far as it related to the deposit or purported deposit:

(i) contained a declaration, or information, that was false or misleading in a material particular; or

(ii) had some other defect or irregularity; and

(e) the balance of the individual’s account is attributable, in whole or in part, to the deposit or purported deposit.

Refund payment

(2) The Commissioner of Taxation may decide to pay to the depositor or purported depositor an amount (the refund payment) equal to the deposit or purported deposit.

Special Account to be debited

(3) The Special Account is debited for the purposes of making the refund payment.

Individual’s account to be debited

(4) When the refund payment is made, the individual’s account is debited by the amount of the refund payment.

Part 7 obligations prevail

(5) The Commissioner of Taxation must not exercise a power conferred by this section in a manner that would be inconsistent with an obligation imposed on him or her by Part 7.

Note: Part 7 deals with withdrawals.

73 Refunds—deposit made by mistake

When section applies

(1) This section applies if:

(a) a deposit or purported deposit was made in respect of an individual; and

(b) the individual’s account was credited with an amount equal to the deposit or purported deposit; and

(c) the credit was made in consequence of the deposit or purported deposit; and

(d) the deposit or purported deposit was paid due to a clerical error or due to some other mistake; and

(e) the balance of the individual’s account is attributable, in whole or in part, to the deposit or purported deposit; and

(f) within 14 days after the credit was made, the depositor or purported depositor applies to the Commissioner of Taxation for a refund of the deposit or purported deposit.

Form of application

(2) The application must be:

(a) in writing; and

(b) in a form approved in writing by the Commissioner of Taxation.

Refund payment

(3) The Commissioner of Taxation must pay to the depositor or purported depositor an amount (the refund payment) equal to the deposit or purported deposit.

Special Account to be debited

(4) The Special Account is debited for the purposes of making the refund payment.

Individual’s account to be debited

(5) When the refund payment is made, the individual’s account is debited by the amount of the refund payment.

Obligations under this section prevail over obligations under Part 7

(6) In the event of a conflict between:

(a) an obligation imposed on the Commissioner of Taxation by this section; and

(b) an obligation imposed on the Commissioner of Taxation by Part 7;

the first‑mentioned obligation prevails.

Note: Part 7 deals with withdrawals.

Notification of refusal of application

(7) If the Commissioner of Taxation refuses an application under this section, the Commissioner of Taxation must give the applicant written notice of the refusal.

74 Recovery of refunds

If a person is entitled to be paid an amount by the Commissioner of Taxation under this Part, the amount may be recovered, as a debt due to the person by the Commonwealth, by action in a court of competent jurisdiction.

Part 9—Inactive accounts

75 Simplified outline

The following is a simplified outline of this Part:

• If an individual’s account is inactive for 10 years, the account balance is to be debited from the Special Account.

• The individual may claim the account balance from the Commissioner of Taxation.

• The Commissioner of Taxation must keep a register of individuals’ account balances debited.

76 No activity for 10 years

When section applies

(1) This section applies to an individual’s account if no amount was credited to the account under:

(a) Part 5 of this Act; or

(b) section 65 of the Superannuation Guarantee (Administration) Act 1992;

at any time during a period of 10 consecutive financial years.

Note 1: Part 5 of this Act deals with deposits.

Note 2: Section 65 of the Superannuation Guarantee (Administration) Act 1992 deals with the crediting of superannuation guarantee shortfalls.

Statement to be given to the Commissioner

(2) As soon as practicable after the end of that period, the Commissioner must record information about the account.

Tax file number

(3) If the individual’s tax file number is known to the Commissioner, the record made for the purposes of subsection (2) must set out that tax file number.

Debit from the Special Account

(4) As soon as practicable after the end of that period, an amount equal to the balance of the individual’s account as at the end of that period is to be debited from the Special Account.

Debiting of individual’s account balance

(5) If an amount is debited from the Special Account under subsection (4), the individual’s account is debited by an amount equal to the amount debited from the Special Account.

Claim by individual

(6) If an amount has been debited from the Special Account under subsection (4), the individual may request the Commissioner of Taxation to pay to the individual an amount equal to the amount debited from the Special Account.

Claim by individual’s legal personal representative

(7) If:

(a) an amount has been debited from the Special Account under subsection (4) in respect of the individual’s account; and

(b) the individual has died;

the individual’s legal personal representative may request the Commissioner of Taxation to pay to the legal personal representative an amount equal to the amount debited from the Special Account in respect of the individual’s account.

Payments

(8) The Commissioner of Taxation must comply with a request under subsection (6) or (7).

Appropriation

(9) The Consolidated Revenue Fund is appropriated for the purposes of subsection (8).

77 Register

In addition to the particulars that are required by section 19 of the Superannuation (Unclaimed Money and Lost Members) Act 1999 to be set out in the register kept under that section, that register must set out:

(a) particulars of amounts debited from the Special Account under section 76 in respect of particular individuals; and

(b) particulars of the individuals, which may include the tax file numbers of the individuals.

Part 10—Tax file numbers

78 Simplified outline

The following is a simplified outline of this Part:

• An individual may quote his or her tax file number to the Commissioner of Taxation.

79 Individual may quote his or her tax file number

(1) An individual may quote his or her tax file number to the Commissioner of Taxation in connection with the operation, or the possibility of the future operation, of this Act in relation to the individual.

Note: This means that an individual’s tax file number may be quoted before or after an account is opened in the name of the individual.

(2) The tax file number may be quoted:

(a) in response to a request made by the Commissioner of Taxation; or

(b) on the individual’s own initiative.

Part 11—Review of decisions

80 Simplified outline

The following is a simplified outline of this Part:

• A person who is dissatisfied with a reviewable decision of the Commissioner of Taxation may seek a reconsideration of the decision.

• A person who is dissatisfied with a reconsidered decision may have the reconsidered decision reviewed by the Administrative Appeals Tribunal.

• The Commissioner of Taxation must tell people about their rights to have decisions reconsidered and reviewed.

81 Reviewable decisions

For the purposes of this Part, a reviewable decision is a decision made by the Commissioner of Taxation under this Act (other than a decision under Division 2, 3 or 4 of Part 6 or a decision relating to the approval of a form).

Note: Decisions under Division 2, 3 or 4 of Part 6 relate to the funding of interest and the calculation of the allocation rate etc.

82 Reconsideration of reviewable decisions

Request for reconsideration

(1) A person who is affected by a reviewable decision may, if dissatisfied with the decision, request the Commissioner of Taxation to reconsider the decision.

Note: Reviewable decision is defined by section 81.

How request must be made

(2) The request must be made by written notice given to the Commissioner of Taxation within the period of 21 days after the day on which the person first receives notice of the decision, or within such further period as the Commissioner of Taxation allows.

Request must set out reasons

(3) The request must set out the reasons for making the request.

Commissioner of Taxation to reconsider decision

(4) Upon receipt of the request, the Commissioner of Taxation must reconsider the decision and may, subject to subsection (5), confirm or revoke the decision or vary the decision in such manner as the Commissioner of Taxation thinks fit.

Deemed confirmation of decision if delay

(5) If the Commissioner of Taxation does not confirm, revoke or vary a decision before the end of the period of 60 days after the day on which the Commissioner of Taxation received the request under subsection (1) to reconsider the decision, the Commissioner of Taxation is taken, at the end of that period, to have confirmed the decision under subsection (4).

Notice of Commissioner of Taxation’s action

(6) If the Commissioner of Taxation confirms, revokes or varies a decision before the end of the period referred to in subsection (5), the Commissioner of Taxation must give written notice to the person telling the person:

(a) the result of the reconsideration of the decision; and

(b) the reasons for confirming, varying or revoking the decision, as the case may be.

83 AAT review of Commissioner of Taxation’s decisions

Applications may be made to the Administrative Appeals Tribunal for review of decisions of the Commissioner of Taxation that have been confirmed or varied under subsection 82(4).

84 Modification of the Administrative Appeals Tribunal Act 1975

Period for making certain AAT applications

(1) If a decision is taken to be confirmed because of subsection 82(5) of this Act, section 29 of the Administrative Appeals Tribunal Act 1975 applies as if the prescribed time for making application for review of the decision were the period of 28 days beginning on the day on which the decision is taken to be confirmed.

Section 41 of AAT Act

(2) If a request is made under subsection 82(1) of this Act in respect of a reviewable decision, section 41 of the Administrative Appeals Tribunal Act 1975 applies as if the making of the request were the making of an application to the Administrative Appeals Tribunal for review of that decision.

85 Statements to accompany notification of decisions

Original decision

(1) If a written notice is given to a person affected by a reviewable decision telling the person that the reviewable decision has been made, that notice is to include a statement to the effect that:

(a) the person may, if dissatisfied with the decision, seek a reconsideration of the decision by the Commissioner of Taxation in accordance with subsection 82(1); and

(b) the person may, subject to the Administrative Appeals Tribunal Act 1975, if dissatisfied with a decision made by the Commissioner of Taxation upon that reconsideration confirming or varying the first‑mentioned decision, make application to the Administrative Appeals Tribunal for review of the decision so confirmed or varied.

Note: Reviewable decision is defined by section 81.

Reconsidered decision

(2) If:

(a) the Commissioner of Taxation confirms or varies a reviewable decision under subsection 82(4); and

(b) gives to a person written notice of the confirmation or variation of the decision;

that notice is to include a statement to the effect that the person may, subject to the Administrative Appeals Tribunal Act 1975, if dissatisfied with the decision so confirmed or varied, make application to the Administrative Appeals Tribunal for review of the decision.

Note: Reviewable decision is defined by section 81.

Validity of decision

(3) A failure to comply with this section does not affect the validity of a decision.

Part 12—Partnerships and unincorporated associations

Division 1—Partnerships

86 Simplified outline

The following is a simplified outline of this Division:

• Partnerships are treated as if they were persons.

• A document given to a partner of a partnership is treated as if it had been given to the partnership.

87 Treatment of partnerships

The superannuation accounts law applies to a partnership as if the partnership were a person, but it applies with the following changes:

(a) obligations that would be imposed on the partnership are imposed instead on each partner, but may be discharged by any of the partners;

(b) any offence against the superannuation accounts law that would otherwise be committed by the partnership is taken to have been committed by each partner who:

(i) aided, abetted, counselled or procured the relevant act or omission; or

(ii) was in any way knowingly concerned in, or party to, the relevant act or omission (whether directly or indirectly and whether by any act or omission of the partner).

Note: Superannuation accounts law is defined by section 4.

88 Giving of documents to partnerships

For the purposes of this Act, if a document is given to a partner of a partnership in accordance with section 28A of the Acts Interpretation Act 1901, the document is taken to have been given to the partnership.

Division 2—Unincorporated associations

89 Simplified outline

The following is a simplified outline of this Division:

• Unincorporated associations are treated as if they were persons.

• A document given to a member of the committee of management of an unincorporated association is treated as if it had been given to the unincorporated association.

90 Treatment of unincorporated associations

Persons

The superannuation accounts law applies to an unincorporated association as if the unincorporated association were a person, but it applies with the following changes:

(a) obligations that would be imposed on the unincorporated association are imposed instead on each member of the committee of management of the association, but may be discharged by any of those members;

(b) any offence against the superannuation accounts law that would otherwise be committed by the unincorporated association is taken to have been committed by each member of the committee of management of the association who:

(i) aided, abetted, counselled or procured the relevant act or omission; or

(ii) was in any way knowingly concerned in, or party to, the relevant act or omission (whether directly or indirectly and whether by any act or omission of the member).

Note: Superannuation accounts law is defined by section 4.

91 Giving of documents to unincorporated associations

For the purposes of this Act, if a document is given to a member of the committee of management of an unincorporated association in accordance with section 28A of the Acts Interpretation Act 1901, the document is taken to have been given to the unincorporated association.

Part 12A—Government co‑contributions for low income earners

91A Commissioner of Taxation may deposit Government co‑contributions for low income earners into individual’s account