New Business Tax System (Consolidation, Value Shifting, Demergers and Other Measures) Act 2002

No. 90, 2002

An Act about income tax to implement a New Business Tax System, and for related purposes

New Business Tax System (Consolidation, Value Shifting, Demergers and Other Measures) Act 2002

No. 90, 2002

An Act about income tax to implement a New Business Tax System, and for related purposes

Contents

1 Short title

2 Commencement

3 Schedule(s)

4 Amendment of income tax assessments

Schedule 1—Consolidation: membership rules

Income Tax Assessment Act 1997

Schedule 2—Consolidation: miscellaneous changes to asset cost provisions

Income Tax Assessment Act 1997

Schedule 3—Consolidation: new Subdivision 705‑B (tax cost setting amount on group formation)

Income Tax Assessment Act 1997

Schedule 4—Consolidation: reset cost base assets held on revenue account

Income Tax Assessment Act 1997

705‑40 Tax cost setting amount for reset cost base assets held on revenue account

Schedule 5—Consolidation: imputation

Income Tax Assessment Act 1997

Schedule 6—Consolidation: international tax

Income Tax Assessment Act 1997

Schedule 7—Consolidation: application and transitional asset cost provisions

Income Tax (Transitional Provisions) Act 1997

Schedule 8—Consolidation: amendment of transitional provisions for losses

Income Tax (Transitional Provisions) Act 1997

Schedule 9—Consolidation: transitional provisions for international tax

Income Tax (Transitional Provisions) Act 1997

Schedule 10—Consolidation: consequential provisions for international tax

Income Tax Assessment Act 1936

Schedule 11—Consolidation: amendment of transitional provision about limiting access to group concessions

New Business Tax System (Consolidation) Act (No. 1) 2002

Schedule 12—Consolidation: amendments of Dictionary

Income Tax Assessment Act 1997

Schedule 13—Exempting entities and former exempting entities

Income Tax Assessment Act 1997

Schedule 14—Loss integrity rules: global method of valuing assets

Part 1—Income Tax Assessment Act 1997

Part 2—Income Tax (Transitional Provisions) Act 1997

Part 3—Dictionary amendments

Income Tax Assessment Act 1997

Part 4—Application of amendments

Schedule 15—Value shifting

Part 1—New Divisions inserted in the Income Tax Assessment Act 1997

Part 2—Amendment of the Income Tax (Transitional Provisions) Act 1997

Part 3—Consequential amendment of the Income Tax Assessment Act 1997

Division 1—Amendments

Division 2—Saving and transitional provisions

Part 4—Consequential amendment of the Income Tax Assessment Act 1936

Part 5—Dictionary amendments

Income Tax Assessment Act 1997

Schedule 16—Demerger relief

Part 1—CGT relief

Income Tax Assessment Act 1997

Part 2—Dividend relief

Income Tax Assessment Act 1936

Part 3—Consequential amendments

Income Tax Assessment Act 1997

Part 4—Transitional

Part 5—Application

New Business Tax System (Consolidation, Value Shifting, Demergers and Other Measures) Act 2002

No. 90, 2002

An Act about income tax to implement a New Business Tax System, and for related purposes

[Assented to 24 October 2002]

The Parliament of Australia enacts:

This Act may be cited as the New Business Tax System (Consolidation, Value Shifting, Demergers and Other Measures) Act 2002.

(1) Each provision of this Act specified in column 1 of the table commences, or is taken to have commenced, on the day or at the time specified in column 2 of the table.

Commencement information | ||

Column 1 | Column 2 | Column 3 |

Provision(s) | Commencement | Date/Details |

1. Sections 1 to 4 and anything in this Act not elsewhere covered by this table | The day on which this Act receives the Royal Assent | 24 October 2002 |

2. Schedules 1 to 12 | Immediately after the commencement of the New Business Tax System (Consolidation) Act (No. 1) 2002 | 24 October 2002 |

3. Schedule 13 | Immediately after the commencement of the New Business Tax System (Imputation) Act 2002 | 29 June 2002 |

4. Schedules 14 and 15 | Immediately after the commencement of the New Business Tax System (Consolidation) Act (No. 1) 2002 | 24 October 2002 |

5. Schedule 16 | The day on which this Act receives the Royal Assent | 24 October 2002 |

Note: This table relates only to the provisions of this Act as originally passed by the Parliament and assented to. It will not be expanded to deal with provisions inserted in this Act after assent.

(2) Column 3 of the table is for additional information that is not part of this Act. This information may be included in any published version of this Act.

Each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

4 Amendment of income tax assessments

Section 170 of the Income Tax Assessment Act 1936 does not prevent the amendment of an assessment made before the commencement of this section for the purposes of giving effect to this Act.

Schedule 1—Consolidation: membership rules

Income Tax Assessment Act 1997

1 Subsection 703‑20(2) (table item 4)

Repeal the item.

Schedule 2—Consolidation: miscellaneous changes to asset cost provisions

Income Tax Assessment Act 1997

1 At the end of subsection 701‑25(4)

Add:

Note: As a consequence of fixing the trading stock’s value at the end of the income year under this subsection, no election would be available under section 70‑45 to value the trading stock at that time.

Note: The heading to subsection 701‑25(4) is altered by omitting “cost” and substituting “value”.

2 Subsection 701‑35(4)

After “ends”, insert “, or, if section 701‑30 applies, of the income year that is taken by subsection (3) of that section to end,”.

Note: The heading to subsection 701‑35(4) is altered by omitting “cost” and substituting “value”.

3 At the end of subsection 701‑35(4)

Add:

Note: As a consequence of fixing the trading stock’s value at the end of the income year under this subsection, no election would be available under section 70‑45 to value the trading stock at that time.

4 Subsection 701‑55(6)

After “above”, insert “is to apply in relation to the asset”.

5 Paragraph 701‑70(3)(a)

Repeal the paragraph, substitute:

(a) the following income year (the joining adjustment year):

(i) if the combining entity is the *head company and the joining time occurs at the start of an income year—the income year before that income year; or

(ii) if the combining entity is the head company and subparagraph (i) does not apply—the income year in which the joining time occurs; or

(iii) in any other case—the income year that ends, or, if section 701‑30 applies, the income year that is taken by subsection (3) of that section to end, at the joining time; and

6 Paragraphs 701‑70(3)(c) and (d)

Omit “income year”, substitute “adjustment year”.

7 Subsection 701‑70(5)

Omit “income year and”, substitute “adjustment year and”.

8 Paragraphs 701‑70(5)(a) and (b)

Omit “income year”, substitute “adjustment year”.

9 Subparagraph 701‑70(7)(b)(ii)

After “started”, insert “, or, if section 701‑30 applies, the income year that is taken by subsection (3) of that section to have started,”.

10 Paragraph 701‑75(3)(a)

Repeal the paragraph, substitute:

(a) the following income year (the leaving adjustment year):

(i) if the separating entity is the *head company—the income year in which the leaving time occurs; or

(ii) in any other case—the income year that starts, or, if section 701‑30 applies, the income year that is taken by subsection (3) of that section to start, at the leaving time.

11 Subsection 701‑75(5)

Omit “income year”, substitute “adjustment year”.

12 Paragraph 701‑80(3)(a)

Repeal the paragraph, substitute:

(a) the entity *acquired, at or before 11.45 am, by legal time in the Australian Capital Territory, on 21 September 1999, a *depreciating asset to which Division 40 applies and held the asset continuously until the entity became a *subsidiary member of the group; and

13 Subsection 705‑30(3)

After “*depreciating asset”, insert “to which Division 40 applies”.

14 Paragraph 705‑45(a)

Repeal the paragraph, substitute:

(a) the joining entity *acquired, at or before 11.45 am, by legal time in the Australian Capital Territory, on 21 September 1999, a *depreciating asset to which Division 40 applies and held the asset continuously until the joining time; and

15 After paragraph 705‑50(2)(a)

Insert:

(aa) subsection (5) does not apply to the asset; and

16 Paragraph 705‑50(3)(a)

After “franked dividends”, insert “or distributions included in the step 4 amount mentioned in step 4 in the table in section 705‑60”.

17 Paragraph 705‑50(6)(a)

After “*depreciating asset”, insert “to which Division 40 applies”.

18 Subsection 705‑65(3)

Omit “the *members of the joined group had, just before the joining time, *disposed of their *membership interests in the joining entity”, substitute “a *CGT event had happened just before the joining time in relation to the *membership interest”.

19 Subsection 705‑65(3)

Omit “the membership interests” (twice occurring), substitute “the membership interest”.

20 After subsection 705‑65(3)

Insert:

Reduction if section 165‑115ZD could apply

(3A) If, on the assumption that:

(a) the *members of the joined group had, just before the joining time, *disposed of their *membership interest in the joining entity; and

(b) the consideration received by the members for the disposal were equal to the *market value of the membership interest at that time;

the *reduced cost base of the membership interest would have been reduced as a result of the operation of section 165‑115ZD of this Act or the Income Tax (Transitional Provisions) Act 1997, then the reduced cost base of the membership interest that is to be used in subsection (1) of this section is reduced by the amount of that reduction.

21 Subsection 705‑65(4)

After “subsection (3)”, insert “or (3A)”.

22 Subsection 705‑65(4)

After “*CGT event”, insert “or a *realisation event”.

23 After subsection 705‑65(5)

Insert:

Reduction in reduced cost base under subsection 165‑115ZA(3) to be added back

(5A) If:

(a) in working out the *reduced cost base of the *membership interest for the purposes of subsection (1), a reduction has taken place under subsection 165‑115ZA(3) (about alterations in ownership or control of loss companies); and

(b) the reduction is to some extent attributable to so much of an amount that was taken into account both in working out the amount of the reduction and in working out:

(i) the step 5 amount under section 705‑100; or

(ii) the step 6 amount under section 705‑110;

the reduced cost base is, to the extent mentioned in paragraph (b), increased by:

(c) if subparagraph (b)(i) applies—the amount of that reduction; or

(d) if subparagraph (b)(ii) applies—the amount of that reduction multiplied by the *general company tax rate.

24 Subsection 705‑70(1) (note)

Repeal the note.

25 After subsection 705‑70(1)

Insert:

Where liability valued differently for joined group

(1A) However, if, in accordance with those *accounting standards or statements, the amount of an accounting liability of the joining entity would be different when it became an accounting liability of the joined group, the different amount is treated as the amount of the liability.

Note: Liabilities that the joining entity owes to members of the joined group would not be excluded under subsection (1) or (1A) even though the standards or statements require that they be eliminated in consolidated accounts of a parent entity and its subsidiaries.

26 Subsection 705‑75(3)

Omit “and (4)”, substitute “, (3) and (3A)”.

Note: The heading to subsection 705‑75(3) is altered by omitting “and (4)” and substituting “, (3) and (3A)”.

27 At the end of section 705‑75

Add:

Application of subsection 705‑65(4)

(4) Subsection 705‑65(4) applies in relation to assets mentioned in subsection (2) of this section in a corresponding way to that in which it applies in relation to members’ *membership interests.

Reduction in reduced cost base under subsection 165‑115ZA(3) to be added back

(5) If:

(a) in working out the *reduced cost base of a *member’s asset for the purposes of subsection (2), a reduction has taken place under subsection 165‑115ZA(3) (about alterations in ownership or control of loss companies); and

(b) the reduction is to some extent attributable to so much of an amount that was taken into account both in working out the amount of the reduction and in working out:

(i) the step 5 amount under section 705‑100; or

(ii) the step 6 amount under section 705‑110;

the reduced cost base is, to the extent mentioned in paragraph (b), increased by:

(c) if subparagraph (b)(i) applies—the amount of that reduction; or

(d) if subparagraph (b)(ii) applies—the amount of that reduction multiplied by the *general company tax rate.

28 Section 705‑90

Repeal the section, substitute:

(1) For the purposes of step 3 in the table in section 705‑60, the step 3 amount is worked out in accordance with this section.

Undistributed profits

(2) First work out the undistributed profits of the joining entity at the joining time. These are the amounts that, in accordance with *accounting standards, or statements of accounting concepts made by the Australian Accounting Standards Board, are retained profits of the joining entity that could be recognised in the joining entity’s statement of financial position if that statement were prepared as at the joining time.

Extent to which dividends paid out of undistributed profits would be frankable

(3) Then work out the extent to which the undistributed profits, if they had been distributed as dividends at the joining time, could have been franked in accordance with section 160AQF of the Income Tax Assessment Act 1936 on the assumptions in subsection (4) of this section.

Assumptions for purposes of subsection (3)

(4) The assumptions are that the joining entity’s franking account balance at the end of the income year that ends, or, if section 701‑30 applies, of the income year that is taken by subsection (3) of that section to end, at the joining time had been adjusted to take account of franking credits or franking debits that would arise if the following were paid just before the joining time:

(a) the income tax, or *refund of income tax, on the joining entity’s taxable income for that income year; and

(b) any income tax, or refund of income tax, that has not yet been paid (regardless of whether it has become payable or due for payment) on the joining entity’s taxable income for any earlier income year, other than one excluded by subsection (5).

Exclusion of certain income years where previous membership of a consolidated group

(5) If the joining entity was previously a *subsidiary member of a *consolidated group, any income year earlier than the one that started, or, if section 701‑30 applies, the one that is taken by subsection (3) of that section to have started, when the joining entity ceased to be a subsidiary member of that group is excluded for the purposes of paragraph (4)(b) of this section.

Undistributed profits must have accrued to joined group and not recouped losses

(6) Next:

(a) work out the extent to which the undistributed profits that, if they had been distributed as dividends at the joining time, could have been so franked accrued to the joined group before the joining time (subsection (7) states what it means for a profit to accrue to the joined group before the joining time); and

(b) then exclude those that recouped losses of any *sort that accrued to the joined group before the joining time (subsection (8) states what it means for a loss to accrue to the joined group before the joining time).

The result is the step 3 amount.

Profit accruing to the joined group before the joining time

(7) A profit accrued to the joined group before the joining time if, on the following assumptions:

(a) that it was distributed to holders of *membership interests as it accrued; and

(b) that entities interposed between the *head company and the joining entity successively distributed any of it immediately after receiving it;

it would have been received by the entity that is the head company at the joining time, in respect of membership interests that it held continuously until that time either directly or indirectly through interposed entities.

Loss accruing to the joined group before the joining time

(8) A loss accrued to the joined group before the joining time if and to the extent that, assuming that as it arose it were instead a profit that was accruing, a distribution of that profit would have been a distribution made to the joined group out of profits that accrued to the joined group before the joining time.

Use of reliable estimates

(9) In working out:

(a) for the purposes of subsection (4), the amount of income tax, or *refund of income tax, on the joining entity’s taxable income for a particular income year and the extent to which it has not yet been paid; or

(b) for the purposes of subsection (7), the amount of a profit that accrued to the joined group during a particular period; or

(c) for the purposes of subsection (8), the amount of a loss that accrued to the joined group during a particular period;

use the most reliable basis for estimation that is available.

29 Subparagraph 705‑95(b)(i)

Omit “705‑90(5)”, substitute “705‑90(7)”.

30 Subparagraph 705‑95(b)(ii)

Omit “705‑90(4)”, substitute “705‑90(8)”.

31 Paragraph 705‑100(1)(b)

Omit “705‑90(4)”, substitute “705‑90(8)”.

32 Subsection 705‑100(2)

Repeal the subsection, substitute:

(2) However, a loss is not to be taken into account under subsection (1) to the extent that it reduced the undistributed profits comprising the step 3 amount in the table in section 705‑60.

33 Paragraph 705‑110(2)(b)

Omit “705‑90(4)”, substitute “705‑90(8)”.

34 Subsection 705‑115(1) (paragraph (b) of the definition of owned deductions)

Omit “was earned”, substitute “accrued”.

35 Subsection 705‑115(1) (paragraph (b) of the definition of owned deductions)

Omit “705‑90(5)”, substitute “705‑90(7)”.

36 Paragraph 705‑115(2)(c)

Repeal the paragraph, substitute:

(c) to the extent that the expenditure reduced the undistributed profits comprising the step 3 amount in the table in section 705‑60.

37 Group heading before section 705‑120

Repeal the heading.

38 Section 705‑120

Repeal the section.

39 Section 711‑20 (table items 5 and 6)

Repeal the items, substitute:

5 | If the amount remaining after step 4 is positive, it is the old group’s allocable cost amount for the leaving entity. Otherwise the old group’s allocable cost amount is nil. |

|

40 Subsection 711‑20(1) (note)

Omit “step 5”, substitute “step 4”.

41 Subsection 711‑35(1)

Omit “ltax rate”, substitute “tax rate”.

42 Subsection 711‑45(5)

Omit “joined group”, substitute “old group”.

43 Section 711‑50

Repeal the section.

44 Section 711‑60

Repeal the section.

Schedule 3—Consolidation: new Subdivision 705‑B (tax cost setting amount on group formation)

Income Tax Assessment Act 1997

1 Section 705‑125

Repeal the link note.

2 After Subdivision 705‑A

Insert:

Subdivision 705‑B—Case of group formation

705‑130 What this Subdivision is about

When a consolidated group comes into existence, the tax cost setting amount for the assets of each entity that becomes a subsidiary member is worked out by modifying the rules in Subdivision 705‑A, so that the amount reflects the cost to the group of acquiring the entity.

Table of sections

Application and object

705‑135 Application and object of this Subdivision

Modified application of Subdivision 705‑A

705‑140 Subdivision 705‑A has effect with modifications

705‑145 Order in which tax cost setting amounts are to be worked out where subsidiary members have membership interests in other subsidiary members

705‑150 Adjustment to result of step 3 in working out allocable cost amount where pre‑formation time roll‑over from head company to member of wholly‑owned group

705‑155 Adjustment in working out step 4 of allocable cost amount for successive distributions through interposed entities

705‑160 Adjustment to allocation of allocable cost amount to take account of owned losses of certain entities that become subsidiary members

[This is the end of the Guide.]

705‑135 Application and object of this Subdivision

Application

(1) This Subdivision has effect for the head company core purposes set out in subsection 701‑1(2) if one or more entities become *subsidiary members of a *consolidated group at the time (the formation time) it comes into existence as a consolidated group.

Note: This is the first exception to Subdivision 705‑A: see paragraph 705‑15(a).

Object

(2) The object of this Subdivision is to modify the rules in Subdivision 705‑A (which basically determine the tax cost setting amount for assets of an entity joining an existing *consolidated group) so that they have effect, and take account of different circumstances that apply, when a consolidated group comes into existence.

Note: The main circumstance is where one of the entities has membership interests in another. In such a case, the order in which the rules in Subdivision 705‑A are applied will affect the tax cost setting amounts for the assets of the entities.

Modified application of Subdivision 705‑A

705‑140 Subdivision 705‑A has effect with modifications

(1) Subdivision 705‑A has effect in relation to each entity becoming a *subsidiary member of the *consolidated group at the formation time in the same way as that Subdivision has effect in relation to an entity becoming a subsidiary member of a consolidated group in circumstances covered by that Subdivision.

(2) However, that effect of Subdivision 705‑A is subject to modifications set out in this Subdivision.

Object

(1) The object of this section is to ensure that where, on becoming *subsidiary members, entities hold assets consisting of *membership interests in other subsidiary members, the *head company’s cost of becoming the holder of the assets of all of the entities that become subsidiary members correctly reflects the group’s cost of acquiring the entities.

Tax cost setting amounts to be worked out from top down

(2) If, on becoming *subsidiary members, entities hold *membership interests in any other entities that become subsidiary members, the *tax cost setting amounts for the assets of entities holding membership interests must be worked out before the tax cost setting amounts for the assets of the entities in which the membership interests are held.

Note: The tax cost setting amount in respect of assets of any subsidiary member in which the head company, but no other subsidiary member, holds membership interests can be worked out in any order in relation to the calculations for other subsidiary members.

Tax cost setting amount for higher entity’s membership interests to be used in working out lower entity’s tax cost setting amount

(3) The tax cost setting amount worked out for assets of an entity mentioned in subsection (2) consisting of *membership interests in another such entity is to be used as the amount for those interests under subsection 705‑65(1) (step 1 of allocable cost amount) in working out the tax cost setting amount for assets of that other entity.

Note 1: Subsection 705‑65(1) adds together amounts worked out in accordance with section 705‑65 representing the cost of the membership interests that each member of the group holds in the entity. If any of those membership interests is held by another subsidiary member, subsection (3) above will replace the amount otherwise applicable with the tax cost setting amount that will have been worked out for the interests in accordance with subsection (2) above.

Note 2: The tax cost setting amount worked out for the membership interests has no relevance other than for the purpose mentioned in subsection (3). This is because, under the single entity principle, intra group membership interests are ignored while entities are members of the group. If an entity ceases to be a member, section 701‑15 and Division 711 set the tax cost of membership interests in the entity at that time.

Value shifting etc. provisions not to apply to later CGT events involving membership interests

(4) However, despite subsection (3), subsection 705‑65(4) (which prevents the later operation of value shifting etc. provisions) still applies to the *membership interests.

Rights and options to acquire membership interests

(5) For the purposes of this section, if, on becoming a *subsidiary member, an entity holds a right or option (including a contingent right or option), created or issued by another entity that becomes a subsidiary member at the same time, to acquire a *membership interest in that other entity, that right or option is treated as if it were a membership interest in that other entity.

Object

(1) The object of this section is to ensure that, in working out the group’s *allocable cost amount for certain entities that become *subsidiary members of the group at the formation time, an adjustment is made to take account of roll‑overs under Subdivision 126‑B or section 160ZZO of the Income Tax Assessment Act 1936 before the formation time.

When section applies

(2) This section applies if:

(a) before the formation time, there was a roll‑over under Subdivision 126‑B or section 160ZZO of the Income Tax Assessment Act 1936 in relation to a *CGT event (the head company roll‑over event) that happened in relation to an asset (the head company roll‑over asset), where:

(i) an entity (the head company roll‑over recipient) that becomes a *subsidiary member of the group was the recipient company in relation to the roll‑over; and

(ii) the originating company in relation to that roll‑over was the entity that becomes the *head company of the group; and

(b) between the roll‑over and the formation time, no other CGT event happened in relation to the head company roll‑over asset:

(i) for which there was another roll‑over satisfying the requirements of paragraph (a); or

(ii) for which there was not a roll‑over under Subdivision 126‑B or section 160ZZO of the Income Tax Assessment Act 1936; and

(c) the head company roll‑over asset is not a *pre‑CGT asset at the formation time; and

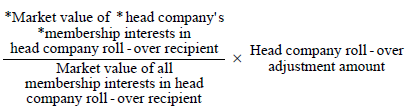

(d) the sum of the *cost bases of all of the *head company’s *CGT assets just before the head company roll‑over event exceeded or was less than the sum of the cost bases of all of the head company’s CGT assets just after the head company roll‑over event (the excess or shortfall being the head company roll‑over adjustment amount).

Adjustment to result of step 3 in allocable cost amount for head company roll‑over recipient

(3) For the purpose of working out the group’s *allocable cost amount for the head company roll‑over recipient, the result of step 3 in the table in section 705‑60 is reduced (if the head company roll‑over adjustment amount is an excess), or increased (if the head company roll‑over adjustment amount is a shortfall), by the amount worked out as follows:

where:

market value of all membership interests in head company roll‑over recipient means the *market value, at the formation time, of all *membership interests in the head company roll‑over recipient that are held by entities that become *members of the group at that time.

Adjustment to result of step 3 in allocable cost amount for interposed entity

(4) Also, if this section applies, for the purpose of working out the group’s *allocable cost amount for any entity (the target entity) that:

(a) becomes a *subsidiary member of the group at the formation time; and

(b) is interposed at that time between the *head company and the head company roll‑over recipient; and

(c) is the first or only such interposed entity;

the result of step 3 in the table in section 705‑60 is reduced (if the head company roll‑over adjustment amount is an excess), or increased (if the head company roll‑over adjustment amount is a shortfall), by the amount worked out as follows:

where:

market value of all membership interests in head company roll‑over recipient has the same meaning as in subsection (3).

market value of head company’s indirect membership interests in head company roll‑over recipient means so much of the *market value, at the formation time, of the *head company’s *membership interests in the target entity as is attributable to membership interests that the entity holds directly, or indirectly through other interposed entities that become *subsidiary members of the group at the formation time, in the head company roll‑over recipient.

Note: If under subsection (3) or (4) the amount by which the result of step 3 is to be reduced exceeds that result, the excess is treated as a capital gain of the head company.

Object

(1) The object of this section is to ensure that, in working out the group’s *allocable cost amount for entities that become *subsidiary members of the group at the formation time, there is only one reduction under step 4 in the table in section 705‑60 (about pre‑formation time distributions out of certain profits) for distributions of the same profits.

When section applies

(2) This section applies if, apart from this section:

(a) in working out the group’s *allocable cost amount for an entity that becomes a *subsidiary member of the group at the formation time, there would be a reduction under step 4 in the table in section 705‑60 for a distribution (the first distribution) made by the entity; and

(b) in working out the group’s *allocable cost amount for a second entity that becomes a *subsidiary member of the group at that time, there would also be a reduction under that step for any of the first distribution that the second entity successively distributed as mentioned in paragraph 705‑95(a).

No step 4 reduction in respect of successive distribution of amount for which there has already been a step 4 reduction

(3) If this section applies, there is no reduction as mentioned in paragraph (2)(b).

Object

(1) The object of this section is to prevent a distortion under section 705‑35 in the allocation of *allocable cost amount to an entity that becomes a *subsidiary member of the group where that entity has *membership interests in another entity that has certain tax losses when it becomes a subsidiary member.

Adjustment to allocation of allocable cost amount

(2) If:

(a) an entity becomes a *subsidiary member of the group at the formation time; and

(b) the entity has *membership interests in a second entity that becomes a subsidiary member of the group at that time; and

(c) in working out the group’s *allocable cost amount for the second entity an amount is required to be subtracted (the loss subtraction amount) under step 5 in the table in section 705‑60 (about losses accruing before becoming a subsidiary member of the group);

then, for the purposes of working out under section 705‑35 the *tax cost setting amount for the assets of the first entity, the *market value of the first entity’s membership interests in the second entity is increased by the first entity’s interest in the loss subtraction amount (see subsection (3)).

First entity’s interest in loss subtraction amount

(3) The first entity’s interest in the loss subtraction amount is worked out using the formula:

Object

(1) The object of this section is to ensure that where, on becoming *subsidiary members, entities hold *membership interests in other subsidiary members, the pre‑CGT status of membership interests held by the *head company, and not the pre‑CGT status of membership interests held by other entities, is used to work out the *pre‑CGT factor under section 705‑125 for assets of the other subsidiary members.

Pre‑CGT factor to be worked out from top down

(2) If, on becoming *subsidiary members, entities hold *membership interests in any other entities that become subsidiary members, the *pre‑CGT factor for the assets of entities holding membership interests must be worked out before the pre‑CGT factor for the assets of the entities in which the membership interests are held.

[The next Division is Division 707.]

Schedule 4—Consolidation: reset cost base assets held on revenue account

Income Tax Assessment Act 1997

1 Section 705‑40

Repeal the section, substitute:

705‑40 Tax cost setting amount for reset cost base assets held on revenue account

(1) The *tax cost setting amount for a reset cost base asset that is *trading stock, a *depreciating asset or a *revenue asset must not exceed the greater of:

(a) the asset’s *market value; and

(b) the joining entity’s *terminating value for the asset.

(2) If subsection (1) reduces the asset’s *tax cost setting amount, the amount of the reduction is allocated among the other reset cost base assets (including other *trading stock, *depreciating assets and *revenue assets) other than excluded assets, so as to increase their tax cost setting amounts, in accordance with the principles set out in subsection (3).

Note: If any of the amount of the reduction cannot be allocated, it is instead treated as a capital loss of the head company.

(3) These are the principles:

(a) the allocation is to be in proportion to the *market values of the assets;

(b) the amount allocated to an item of *trading stock, to a *depreciating asset or to a *revenue asset must not cause its *tax cost setting amount to contravene subsection (1);

(c) any of the amount that cannot be allocated is to be reallocated, to the maximum extent possible, among the remaining reset cost base assets (other than excluded assets) by applying this subsection a further one or more times.

Schedule 5—Consolidation: imputation

Income Tax Assessment Act 1997

1 Paragraph 709‑60(3)(c)

Omit “item 6 of the table in section 160‑115”, substitute “item 5 of the table in section 205‑15”.

2 Subsection 709‑70(2) (note)

Omit “section 160‑115”, substitute “section 205‑15”.

3 Subsection 709‑75(2) (note)

Omit “section 160‑130”, substitute “section 205‑30”.

Schedule 6—Consolidation: international tax

Income Tax Assessment Act 1997

1 Section 711‑70 (link note)

Repeal the link note, substitute:

[The next Division is Division 717.]

2 After Division 711

Insert:

Division 717—International tax rules

Table of Subdivisions

717‑A Foreign tax credits

717‑D Attributable income: entry rules

717‑E Attributable income: exit rules

Subdivision 717‑A—Foreign tax credits

717‑1 What this Subdivision is about

If an entity becomes a subsidiary member of a consolidated group, its excess foreign tax credits are transferred to the head company of the group, for use in later income years. The head company receives any foreign tax credits that arise because the entity pays foreign tax while it is a subsidiary member of the group.

Table of sections

Objects

717‑5 Objects of this Subdivision

Foreign tax on amounts in head company’s assessable income

717‑10 Head company taken to be liable for subsidiary member’s foreign tax

Foreign tax on amounts not in head company’s assessable income

717‑15 Transferring subsidiary member’s excess foreign tax credits from earlier years to head company

717‑20 Where entity not subsidiary member for whole of income year

[This is the end of the Guide.]

717‑5 Objects of this Subdivision

(1) The main objects of this Subdivision are set out in subsections (2), (3) and (4).

(2) The first of those objects is to allow the *head company of a *consolidated group to get the benefit of foreign tax paid in respect of foreign income (within the meaning of the Income Tax Assessment Act 1936) included in the head company’s assessable income because another entity is or was a *subsidiary member of the group.

(3) The second of those objects is to allow the *head company of a *consolidated group to apply, in relation to an income year, *excess foreign tax credits of an entity (the joining entity) that becomes a *subsidiary member of the group at a time (the joining time) if:

(a) the income year starts after the joining time; and

(b) those excess foreign tax credits are from an income year ending before the joining time.

(4) The third of those objects is to prevent an entity (other than the *head company of the group) from applying *excess foreign tax credits mentioned in paragraph (3)(b) to increase its own credits in respect of foreign tax.

Foreign tax on amounts in head company’s assessable income

717‑10 Head company taken to be liable for subsidiary member’s foreign tax

(1) This section operates if:

(a) an entity was a *subsidiary member of a *consolidated group for all or part of an income year; and

(b) the assessable income of the *head company of the group for that income year included foreign income (within the meaning of the Income Tax Assessment Act 1936); and

(c) the entity paid, and was personally liable for, foreign tax (within the meaning of that Act) in respect of that foreign income (whether or not the entity was a subsidiary member of the group at the time of payment).

(2) Section 160AF of the Income Tax Assessment Act 1936 operates as if:

(a) the *head company had paid and been personally liable for the foreign tax; and

(b) the entity had not paid and had not been personally liable for the foreign tax.

Note: Section 160AF of the Income Tax Assessment Act 1936 provides a foreign tax credit (which is a tax offset) of an amount that depends on:

(a) foreign tax that an entity paid, and was personally liable for, in respect of foreign income included in the entity’s assessable income; and

(b) the amount of Australian tax payable (worked out as described in that section) in respect of the foreign income.

(3) This section does not limit the operation of section 160AF of the Income Tax Assessment Act 1936.

Foreign tax on amounts not in head company’s assessable income

(1) This section operates for the purposes of section 160AFE of the Income Tax Assessment Act 1936 in relation to an income year if:

(a) an entity (the joining entity) becomes a *subsidiary member of a *consolidated group at a time (the joining time); and

(b) the joining time is:

(i) before the start of that income year; and

(ii) after the start of an earlier income year (the earlier year); and

(c) the joining entity has *excess foreign tax credits (the transfer credits) from the earlier year.

(2) For those purposes:

(a) the *head company of the group is taken to have the transfer credits; and

(b) the joining entity is taken not to have the transfer credits; and

(c) if, apart from paragraph (a), the head company has *excess foreign tax credits from the earlier year—the transfer credits are taken to be included in those excess foreign tax credits.

(3) Subsection (2) also has effect for the purposes of a subsequent operation of this section.

Example: An entity becomes a subsidiary member of a consolidated group in an income year. This section operates in relation to a later income year so that the entity no longer has the transfer credits mentioned in paragraph (1)(c) (see paragraph (2)(b)). The entity later leaves the group and becomes a subsidiary member of a second consolidated group. In a subsequent operation of this section in relation to the head company of the second group, the entity will not have those transfer credits, because of the previous operation of paragraph (2)(b).

(4) This section operates separately in relation to each class of foreign income (within the meaning of the Income Tax Assessment Act 1936) identified in subsection 160AF(7) of that Act, as if:

(a) the *head company’s foreign income of that class for an income year were the whole of the head company’s foreign income for that year; and

(b) the joining entity’s foreign income of that class for an income year were the whole of the joining entity’s foreign income for that year.

717‑20 Where entity not subsidiary member for whole of income year

(1) This section operates if:

(a) an entity (the joining entity) is a *subsidiary member of a *consolidated group for some but not all of an income year (the joining year); and

(b) there are one or more periods in the joining year (each of which is a non‑membership period) during which the entity is not a subsidiary member of any *consolidated group.

Note: Section 701‑30 treats each non‑membership period as a separate income year for some purposes.

(2) Subsection (3) has effect for the purposes of section 701‑30 in relation to the joining entity.

(3) In working out amounts for the joining entity under subsection 701‑30(3) in relation to each non‑membership period, make these assumptions:

(a) if the joining year starts at the same time as the earliest of those non‑membership periods:

(i) subsection 160AFE(2) of the Income Tax Assessment Act 1936 operates in relation to the joining entity for that non‑membership period; and

(ii) subsection 160AFE(2) of that Act does not operate in relation to the joining entity for the later non‑membership periods (if any);

(b) otherwise—subsection 160AFE(2) of that Act does not operate in relation to the joining entity for any of the non‑membership periods.

(4) Subsection (5) has effect for the purposes of section 717‑15 in relation to the *head company of the *consolidated group for a later income year.

(5) In working out the amount (if any) of the joining entity’s transfer credits (within the meaning of paragraph 717‑15(1)(c)) from the joining year, do not include the amount of the joining entity’s *excess foreign tax credits from a non‑membership period (if any) that ends at the same time the joining year ends.

[The next Subdivision is Subdivision 717‑D.]

Subdivision 717‑D—Attributable income: entry rules

717‑200 What this Subdivision is about

Each attribution surplus, attributed tax account surplus, FIF attribution surplus and FIF attributed tax account surplus relating to a company that becomes a subsidiary member of a consolidated group is transferred to the head company of the group.

Table of sections

Object

717‑205 Object of this Subdivision

Transfers

717‑210 Attribution surpluses

717‑215 Attributed tax account surpluses

717‑220 FIF attribution surpluses

717‑225 FIF attributed tax account surpluses

717‑230 Calculating FIF income where a company joins the group

[This is the end of the Guide.]

717‑205 Object of this Subdivision

The main object of this Subdivision is to avoid double taxation by transferring from a company (the joining company) that becomes a *subsidiary member of a *consolidated group at a time (the joining time) to the *head company of the group the benefit of each of these:

(a) the attribution surplus (if any) for an attribution account entity (within the meaning of Part X of the Income Tax Assessment Act 1936) in relation to the joining company just before the joining time;

(b) the attributed tax account surplus (if any) for an attribution account entity (within the meaning of Part X of the Income Tax Assessment Act 1936) in relation to the joining company just before the joining time;

(c) the FIF attribution surplus (if any) for a FIF attribution account entity (within the meaning of Part XI of the Income Tax Assessment Act 1936) in relation to the joining company just before the joining time;

(d) the FIF attributed tax account surplus (if any) for a *FIF (within the meaning of Part XI of the Income Tax Assessment Act 1936) in relation to the joining company just before the joining time.

(1) This section operates for the purposes of Part X of the Income Tax Assessment Act 1936 if:

(a) a company (the joining company) becomes a *subsidiary member of a *consolidated group at a time (the joining time); and

(b) just before the joining time there was an attribution surplus for an attribution account entity in relation to the joining company for the purposes of that Part; and

(c) just before the joining time the joining company’s attribution account percentage in relation to the attribution account entity for the purposes of that Part was more than nil.

Credit in relation to the head company

(2) An attribution credit arises at the joining time for the attribution account entity in relation to the *head company of the group. The credit is equal to the attribution surplus.

Debit in relation to the joining company

(3) An attribution debit arises at the joining time for the attribution account entity in relation to the joining company. The debit is equal to the attribution surplus.

717‑215 Attributed tax account surpluses

Section 717‑210 also operates as described in the table:

Transfer of attributed tax account surpluses by section 717‑210 | ||

Item | Section 717‑210 operates in relation to this thing (within the meaning of Part X of the Income Tax Assessment Act 1936): | In the same way as it operates in relation to this thing: |

1 | Attributed tax account surplus | Attribution surplus |

2 | Attributed tax account credit | Attribution credit |

3 | Attributed tax account debit | Attribution debit |

717‑220 FIF attribution surpluses

Section 717‑210 also operates for the purposes of Part XI of the Income Tax Assessment Act 1936 as described in the table:

Transfer of FIF attribution surpluses by section 717‑210 | ||

Item | Section 717‑210 operates in relation to this thing (within the meaning of Part XI of the Income Tax Assessment Act 1936): | In the same way as it operates in relation to this thing: |

1 | FIF attribution surplus | Attribution surplus |

2 | FIF attribution account entity | Attribution account entity |

3 | FIF attribution account percentage | Attribution account percentage |

4 | FIF attribution credit | Attribution credit |

5 | FIF attribution debit | Attribution debit |

Note: Section 717‑230 may affect the calculation of the FIF attribution surplus for the FIF attribution account entity in relation to the joining company just before the joining time.

717‑225 FIF attributed tax account surpluses

Section 717‑210 also operates for the purposes of Part XI of the Income Tax Assessment Act 1936 as described in the table:

Transfer of FIF attributed tax account surpluses by section 717‑210 | ||

Item | Section 717‑210 operates in relation to this thing (within the meaning of Part XI of the Income Tax Assessment Act 1936): | In the same way as it operates in relation to this thing: |

1 | FIF attributed tax account surplus | Attribution surplus |

2 | *FIF | Attribution account entity |

3 | FIF attribution account percentage | Attribution account percentage |

4 | FIF attributed tax account credit | Attribution credit |

5 | FIF attributed tax account debit | Attribution debit |

Note: Section 717‑230 may affect the calculation of the FIF attributed tax account surplus for the FIF in relation to the joining company just before the joining time.

717‑230 Calculating FIF income where a company joins the group

(1) This section modifies the operation of Part XI of the Income Tax Assessment Act 1936 if:

(a) a company (the joining company) becomes a *subsidiary member of a *consolidated group at a time (the joining time); and

(b) for the purposes of that Part, the FIF attribution account percentage of the joining company in relation to a FIF attribution account entity that is a *FIF is more than nil at the time (the surplus time) just before the joining time.

(2) That Part operates in relation to the joining company as if a notional accounting period of the *FIF in relation to the joining company ended at the time (the credit/debit time) just before the surplus time.

(3) That Part operates in relation to the joining company as if subsection 485(3) of that Act provided that the operative provision applied to the joining company in relation to the *FIF in respect of the notional accounting period of that FIF that ended in the year of income that included the credit/debit time.

(4) Paragraph 538(2)(d) of that Act operates in relation to the *head company of the *consolidated group in relation to the *FIF in respect of the notional accounting period of that FIF that included the joining time as if:

(a) the head company had acquired the interest or interests mentioned in that paragraph during that period (so far as those interests are held by the head company because the joining company became a *subsidiary member of the group); and

(b) the amount or value of the consideration paid or given by the head company in respect of the acquisition was equal to the amount worked out under paragraph 538(2)(a) of that Act in relation to the joining company in relation to the FIF in respect of the notional accounting period mentioned in subsection (2) of this section.

Note: The modifications made by this section:

(a) apply if a company joins a consolidated group during a notional accounting period of a FIF in which the company has an interest; and

(b) allow the appropriate calculation of amounts attributed under FIF rules to the head company and joining company before and after the joining time; and

(c) mean that foreign investment fund income that accrued to the joining company from the FIF will be included in the joining company’s assessable income and will give rise to a FIF attribution credit, and may also give rise to a FIF attribution debit, in relation to the joining company; and

(d) mean that the FIF attribution surplus and the FIF attributed tax account surplus for the FIF attribution account entity in relation to the joining company at the surplus time will take account of credits and debits arising at the credit/debit time and earlier.

Subdivision 717‑E—Attributable income: exit rules

717‑235 What this Subdivision is about

Each attribution surplus, attributed tax account surplus, FIF attribution surplus and FIF attributed tax account surplus relating to a company that ceases to be a subsidiary member of a consolidated group is transferred to that company from the head company of the group.

Table of sections

Object

717‑240 Object of this Subdivision

Transfer of Part X surpluses

717‑245 Attribution surpluses

717‑250 Attributed tax account surpluses

Transfer of Part XI surpluses

717‑255 FIF attribution surpluses

717‑260 FIF attributed tax account surpluses

717‑265 Calculating FIF income where a company leaves the group

[This is the end of the Guide.]

717‑240 Object of this Subdivision

The main object of this Subdivision is to avoid double taxation by transferring from the *head company of a *consolidated group to a company (the leaving company) that ceases to be a *subsidiary member of the group at a time (the leaving time) the benefit of each of these surpluses (to the extent that each surplus can be attributed to the leaving company):

(a) the attribution surplus (if any) for an attribution account entity (within the meaning of Part X of the Income Tax Assessment Act 1936) in relation to the head company just before the leaving time;

(b) the attributed tax account surplus (if any) for an attribution account entity (within the meaning of Part X of the Income Tax Assessment Act 1936) in relation to the head company just before the leaving time;

(c) the FIF attribution surplus (if any) for a FIF attribution account entity (within the meaning of Part XI of the Income Tax Assessment Act 1936) in relation to the head company just before the leaving time;

(d) the FIF attributed tax account surplus (if any) for a *FIF (within the meaning of Part XI of the Income Tax Assessment Act 1936) in relation to the head company just before the leaving time.

(1) This section operates for the purposes of Part X of the Income Tax Assessment Act 1936 if:

(a) a company (the leaving company) ceases to be a *subsidiary member of a *consolidated group at a time (the leaving time); and

(b) just before the leaving time there was, for the purposes of that Part, an attribution surplus for an attribution account entity in relation to the *head company of the group; and

(c) at the leaving time the leaving company’s attribution account percentage in relation to the attribution account entity for the purposes of that Part is more than nil.

Credit in relation to leaving company

(2) An attribution credit arises at the leaving time for the attribution account entity in relation to the leaving company. The credit is the amount worked out under subsection (4).

Debit in relation to head company

(3) An attribution debit arises at the leaving time for the attribution account entity in relation to the company that was the *head company of the group just before the leaving time. The debit is the amount worked out under subsection (4).

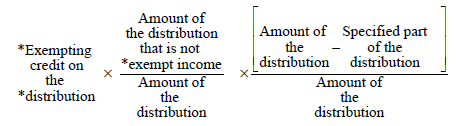

Amount of credit and debit

(4) The amount of the credit and debit is worked out using the formula:

717‑250 Attributed tax account surpluses

Section 717‑245 also operates as described in the table:

Transfer of attributed tax account surpluses by section 717‑245 | ||

Item | Section 717‑245 operates in relation to this thing (within the meaning of Part X of the Income Tax Assessment Act 1936): | In the same way as it operates in relation to this thing: |

1 | Attributed tax account surplus | Attribution surplus |

2 | Attributed tax account credit | Attribution credit |

3 | Attributed tax account debit | Attribution debit |

717‑255 FIF attribution surpluses

Section 717‑245 also operates for the purposes of Part XI of the Income Tax Assessment Act 1936 as described in the table:

Transfer of FIF attribution surpluses by section 717‑245 | ||

Item | Section 717‑245 operates in relation to this thing (within the meaning of Part XI of the Income Tax Assessment Act 1936): | In the same way as it operates in relation to this thing: |

1 | FIF attribution surplus | Attribution surplus |

2 | FIF attribution account entity | Attribution account entity |

3 | FIF attribution account percentage | Attribution account percentage |

4 | FIF attribution credit | Attribution credit |

5 | FIF attribution debit | Attribution debit |

Note: Section 717‑265 may affect the calculation of the FIF attribution surplus for the FIF attribution account entity in relation to the head company just before the leaving time.

717‑260 FIF attributed tax account surpluses

Section 717‑245 also operates for the purposes of Part XI of the Income Tax Assessment Act 1936 as described in the table:

Transfer of FIF attributed tax account surpluses by section 717‑245 | ||

Item | Section 717‑245 operates in relation to this thing (within the meaning of Part XI of the Income Tax Assessment Act 1936): | In the same way as it operates in relation to this thing: |

1 | FIF attributed tax account surplus | Attribution surplus |

2 | *FIF | Attribution account entity |

3 | FIF attribution account percentage | Attribution account percentage |

4 | FIF attributed tax account credit | Attribution credit |

5 | FIF attributed tax account debit | Attribution debit |

Note: Section 717‑265 may affect the calculation of the FIF attributed tax account surplus for the FIF in relation to the head company just before the leaving time.

717‑265 Calculating FIF income where a company leaves the group

(1) This section modifies the operation of Part XI of the Income Tax Assessment Act 1936 in relation to a company (the transferor company) if:

(a) the transferor company is the *head company of a *consolidated group at a time (the surplus time); and

(b) for the purposes of that Part, the FIF attribution account percentage of the transferor company in relation to a FIF attribution account entity that is a *FIF is more than nil at the surplus time; and

(c) another company (the leaving company) ceases to be a *subsidiary member of the group at the time (the leaving time) just after the surplus time; and

(d) for the purposes of that Part, the leaving company’s FIF attribution account percentage in relation to that FIF attribution account entity is more than nil at the leaving time.

(2) That Part operates in relation to the transferor company as if a notional accounting period of the *FIF in relation to the transferor company ended at the time (the credit/debit time) just before the surplus time.

(3) That Part operates in relation to the transferor company as if the next notional accounting period of the *FIF in relation to the transferor company started at the surplus time and continued until whichever of these times occurs first:

(a) the time when a notional accounting period of the FIF in relation to the transferor company would have ended apart from this section;

(b) the time when the period ends because of another application of this section.

(4) That Part operates in relation to the transferor company as if subsection 485(3) of that Act provided that the operative provision applied to the transferor company in relation to the *FIF in respect of the notional accounting period of that FIF that ended in the year of income that included the credit/debit time.

(5) Paragraph 538(2)(d) of that Act operates in relation to the leaving company in relation to the *FIF in respect of the notional accounting period of that FIF that included the leaving time as if:

(a) the leaving company had acquired the interest or interests mentioned in that paragraph during that period (so far as those interests are held by the leaving company because it ceased to be a *subsidiary member of the group); and

(b) the amount or value of the consideration paid or given by the leaving company in respect of the acquisition was equal to the amount worked out under paragraph 538(2)(a) of that Act in relation to the transferor company in relation to the FIF in respect of the notional accounting period mentioned in subsection (2) of this section.

Note: The modifications made by this section:

(a) apply if a company leaves a consolidated group during a notional accounting period of a FIF in which the company has an interest; and

(b) allow the appropriate calculation of amounts attributed under FIF rules to the transferor company and leaving company before and after the leaving time; and

(c) mean that foreign investment fund income that accrued to the transferor company from the FIF will be included in the transferor company’s assessable income and will give rise to a FIF attribution credit, and may also give rise to a FIF attribution debit, in relation to the transferor company; and

(d) mean that the FIF attribution surplus and the FIF attributed tax account surplus for the FIF attribution account entity in relation to the transferor company at the surplus time will take account of credits and debits arising at the credit/debit time and earlier.

[The next Division is Division 719.]

Schedule 7—Consolidation: application and transitional asset cost provisions

Income Tax (Transitional Provisions) Act 1997

1 Section 700‑1

Repeal the section, substitute:

700‑1 Application of Part 3‑90 of Income Tax Assessment Act 1997

Part 3‑90 of the Income Tax Assessment Act 1997, as inserted by the New Business Tax System (Consolidation) Bill (No. 1) 2002 and amended by the New Business Tax System (Consolidation, Value Shifting, Demergers and Other Measures) Act 2002, applies on and after 1 July 2002.

2 After Division 700

Insert:

Table of Subdivisions

701‑A Preliminary

701‑B Modified application of provisions

Table of sections

701‑1 Transitional group and transitional entity

701‑5 Chosen transitional entity

701‑10 Interpretation

701‑1 Transitional group and transitional entity

Group formed on 1 July 2002

(1) If a consolidated group came into existence on 1 July 2002:

(a) the group is a transitional group; and

(b) each entity that became a subsidiary member of the group on the day it came into existence is a transitional entity.

Group formed after 1 July 2002 but before 1 July 2003

(2) If a consolidated group came into existence after 1 July 2002 but before 1 July 2003:

(a) the group is a transitional group if at least one entity that became a subsidiary member of the group on the day the group came into existence is a transitional entity; and

(b) an entity is a transitional entity if:

(i) at no time after 1 July 2002 and before the group came into existence was the entity a wholly‑owned subsidiary of the entity (the future head company) that became the head company of the group; or

(ii) at some time during that period, the entity was a wholly‑owned subsidiary of the future head company and it remained such from the earliest time after 1 July 2002 when it was a wholly‑owned subsidiary of the future head company until the group came into existence.

Group formed during financial year starting on 1 July 2003

(3) If a consolidated group came into existence during the financial year starting on 1 July 2003:

(a) the group is a transitional group if at least one entity that became a subsidiary member of the group on the day the group came into existence is a transitional entity; and

(b) an entity is a transitional entity if:

(i) just before 1 July 2003, it was a wholly‑owned subsidiary of the future head company; and

(ii) it remained such from the earliest time after 1 July 2002 when it was a wholly‑owned subsidiary of the future head company until the group came into existence.

701‑5 Chosen transitional entity

(1) If a group is a transitional group, its head company may choose that the group’s transitional entity is a chosen transitional entity, or one or more of the group’s transitional entities are chosen transitional entities.

Period for making choice

(2) The choice must be made by the end of the period described in subsection 703‑50(3) for giving the Commissioner the choice under section 703‑50 that the group is taken to be consolidated.

Choice is irrevocable

(3) The choice cannot be revoked.

A reference in this Division to:

(a) a provision of the Income Tax Assessment Act 1997; or

(b) a consolidated group’s allocable cost amount for an entity;

is a reference to that provision as it applies to the group, or to the allocable cost amount as it is worked out for the entity, in accordance with Subdivision 705‑B of that Act and with this Division.

Subdivision 701‑B—Modified application of provisions

Table of sections

701‑15 Tax cost and trading stock value not set for assets of chosen transitional entities

701‑20 Working out allocable cost amount on formation for subsidiary members other than chosen transitional entities

701‑25 No operation of value shifting and loss transfer provisions to membership interests in chosen transitional entities

701‑30 Undistributed, unfrankable pre‑formation profits of non‑chosen transitional entities—adjustment to allocable cost amount and tax cost setting amount reduction for over‑depreciated assets

701‑35 CGT event for pre‑formation roll‑over after 16 May 2002 to be disregarded if cost base etc. would be different

701‑40 When entity leaves transitional group, head company may choose, for purposes of transitional group’s allocable cost amount, to increase terminating values of over‑depreciated assets

701‑45 When entity leaves transitional group, head company may choose, for purposes of transitional group’s allocable cost amount, to use formation time market values, instead of terminating values, for certain pre‑CGT assets

701‑15 Tax cost and trading stock value not set for assets of chosen transitional entities

Section 701‑10 (cost to head company of assets that entity brings into group) and subsection 701‑35(4) (setting value of trading stock at tax‑neutral amount) do not apply to the assets of a chosen transitional entity.

Note: The fact that the head company inherits the entity’s history under section 701‑5 when the entity becomes a subsidiary member of the group means that the entity’s assets would be treated as having the same cost as they would for the entity at that time.

When section applies

(1) This section applies if any of the transitional entities in the transitional group is a chosen transitional entity.

Allocable cost amount to be worked out in special way

(2) If this section applies, the group’s allocable cost amount for each of the entities, other than a chosen transitional entity, that become subsidiary members when the group comes into existence (each of which is a non‑chosen subsidiary) is worked out in a special way.

How to work out allocable cost amount

(3) The allocable cost amount for each non‑chosen subsidiary is the sum of:

(a) the head company adjusted allocable amount for the non‑chosen subsidiary (see subsection (4)); and

(b) for each sub‑group (see subsection (6)) that exists in relation to the non‑chosen subsidiary—the sub‑group’s notional allocable cost amount (see subsection(5)) for the non‑chosen subsidiary.

Head company adjusted allocable amount

(4) The head company adjusted allocable amount for the non‑chosen subsidiary is the amount that would be the transitional group’s allocable cost amount for that entity if;

(a) the holding of all sub‑group membership interests were disregarded; and

(b) only the following proportion of each of the step 2 to step 7 amounts in the table in section 705‑60 was taken into account:

where:

market value of all membership interests in non‑chosen subsidiary means the market value, at the time the group comes into existence, of all membership interests in the non‑chosen subsidiary that are held by entities that become members of the group at that time.

market value of head company’s direct and indirect membership interests in non‑chosen subsidiary means the market value, at the time the group comes into existence, of all membership interests in the non‑chosen subsidiary that the head company holds directly or indirectly through interposed entities that become subsidiary members of the group at that time and are not included in any sub‑group in relation to the non‑chosen subsidiary.

Sub‑group’s notional allocable cost amount

(5) For each sub‑group that exists in relation to the non‑chosen subsidiary, there is a sub‑group’s notional allocable cost amount. That amount is the amount that would be a consolidated group’s allocable cost amount for the non‑chosen subsidiary if:

(a) the consolidated group came into existence at the same time as the transitional group and consisted only of the non‑chosen subsidiary and the entities comprising the sub‑group; and

(b) the chosen transitional entity in the sub‑group were the head company of the consolidated group; and

(c) the only membership interests that any entity in the sub‑group held in any other member of the consolidated group were the sub‑group membership interests (see subsection (6)) in relation to the sub‑group; and

(d) only the following proportion of each of the step 2 to step 7 amounts in the table in section 705‑60 was taken into account:

where:

market value of all membership interests in non‑chosen subsidiary means the market value, at the time the group comes into existence, of all membership interests in the non‑chosen subsidiary that are held by entities that become members of the group at that time.

market value of chosen transitional entity’s direct and indirect membership interests in non‑chosen subsidiary means the market value, at the time the group comes into existence, of all membership interests in the non‑chosen subsidiary that the chosen transitional entity holds directly or indirectly through interposed entities that are included in the sub‑group.

Sub‑group and sub‑group membership interests

(6) If a chosen transitional entity holds membership interests in a non‑chosen subsidiary, either directly or indirectly through one or more other entities, each of which is a non‑chosen subsidiary:

(a) the chosen transitional entity and each interposed non‑chosen subsidiary comprise a sub‑group in relation to the non‑chosen subsidiary (unless the non‑chosen subsidiary is included in a sub‑group in relation to another non‑chosen subsidiary); and

(b) the following membership interests are the sub‑group membership interests in relation to the sub‑group:

(i) the membership interests that the chosen transitional entity holds directly in the non‑chosen subsidiary or in any of the interposed non‑chosen subsidiaries;

(ii) the membership interests that each interposed non‑chosen subsidiary holds directly in the non‑chosen subsidiary or in any of the other interposed non‑chosen subsidiaries.

If any provision of this Act would, because of events that happened before the time the transitional group came into existence, apply to a CGT event that happens after that time to change the cost base or reduced cost base of the members’ membership interests in a chosen transitional entity, the provision does not so apply.

Note: For example, such a provision could otherwise apply where a loss transfer or value shift involving the entity has occurred.

Application of section to non‑chosen transitional entities where transitional group formed before 1 July 2003

(1) This section applies if the transitional group comes into existence before 1 July 2003. It applies to each transitional entity in the transitional group, other than a chosen transitional entity. This is so even if there are no chosen transitional entities at all.

Increase in step 3 of allocable cost amount on group formation

(2) The amount to be added under section 705‑90 (step 3 of allocable cost amount) of the Income Tax Assessment Act 1997 in working out the transitional group’s allocable cost amount for the transitional entity is increased by the additional undistributed profits (the step 3 unfrankable profits increase) that would form part of the step 3 amount under that section if:

(a) subsections (3) and (4), and paragraph (6)(b), of that section were disregarded; and

(b) it were a requirement of that section that, if any additional undistributed profits resulting from paragraph (a) of this subsection were distributed as dividends just before the group came into existence, the head company and each other transitional entity interposed between the head company and the transitional entity would be entitled to a rebate of income tax under section 46 or 46A of the Income Tax Assessment Act 1936 on the dividends.

Increase in tax deferral amount in relation to over‑depreciated assets

(3) The tax deferral amount for the purposes of applying section 705‑50 (reduction in tax cost setting amount for over‑depreciated assets) of the Income Tax Assessment Act 1997 in relation to an asset of the transitional entity that becomes that of the head company under subsection 701‑1(1) (the single entity rule) of that Act when the transitional group comes into existence is increased by the amount worked out under subsection (4) of this section.

Amount of increase in tax deferral amount

(4) The increase is equal to the amount that would have been the step 3 unfrankable profits increase if the undistributed profits constituting that increase were also required to satisfy the following requirements:

(a) the profits were not subject to income tax because of deductions for the asset’s decline in value;

(b) the decline in value represented the over‑depreciation of the asset;

(c) the deductions for the decline in value do not form part of a tax loss covered by the step 5 amount mentioned in step 5 in the table in section 705‑60 of the Income Tax Assessment Act 1997 in working out the transitional group’s allocable cost amount for the transitional entity.

If:

(a) after 16 May 2002 and before the transitional group came into existence, a CGT event happened in relation to an asset for which there was:

(i) a roll‑over under Subdivision 126‑B of the Income Tax Assessment Act 1997; or

(ii) roll‑over relief under section 40‑340 of that Act in a case covered by item 4 of the table in subsection (1) of that section; and

(b) the cost base or reduced cost base of that asset or any other asset that:

(i) became an asset of the head company when the transitional group came into existence because subsection 701‑1(1) (the single entity rule) of that Act applies; or

(ii) was otherwise an asset of the head company at that time;

differs at that time from what it would have been if the roll‑over had not occurred or there had been no such roll‑over relief;

then Part 3‑90 of the Income Tax Assessment 1997 applies as if the CGT event had not happened.

(1) This section applies if an entity ceases to be a subsidiary member of the transitional group and the requirements of subsections (2) to (5) are satisfied.

Asset held at leaving time

(2) Just before the entity ceases to be a subsidiary member, it must, disregarding subsection 701‑1(1) (the single entity rule) of the Income Tax Assessment Act 1997, hold an asset.

Reduction of asset’s tax cost setting amount for over‑depreciation

(3) When the transitional group came into existence:

(a) the asset must have become that of the head company of the transitional group because subsection 701‑1(1) of that Act applied in relation to a transitional entity; and

(b) section 705‑50 of that Act must have reduced by an amount (the reduction amount) the tax cost setting amount for the asset.

Asset held continuously within group

(4) The asset must, disregarding subsection 701‑1(1) of that Act, have been held at all times by the head company or a subsidiary member of the transitional group from when the transitional group came into existence until the entity ceases to be a subsidiary member of the transitional group.

Head company’s advice to leaving entity

(5) Before the entity ceases to be a subsidiary member of the transitional group, the head company must have advised the entity of the amount that the head company proposes to choose under subsection (6) of this section in relation to the asset.

Note: This information would need to be known by the entity if it later becomes a subsidiary member of another consolidated group and still holds the asset. This is because subsection 705‑50(5) of the Income Tax Assessment Act 1997 requires a reduction in the tax cost setting amount for the asset on joining that other group and the amount chosen by the head company under this section is relevant to working out that reduction.

Head company’s choice

(6) If this section applies, the head company may, in relation to the entity’s ceasing to be a subsidiary member, choose that the terminating value for the asset, that is to be used in applying step 1 of the table in section 711‑20 of the Income Tax Assessment Act 1997, is increased by so much of the reduction amount as the head company chooses.

(1) This section applies if:

(a) an entity ceases to be a subsidiary member of the transitional group; and

(b) just before the transitional group came into existence, the entity that became the head company held a pre‑CGT asset; and

(c) that holding of the asset did not occur as a result of a CGT event:

(i) for which there was a roll‑over under Subdivision 126‑B of the Income Tax Assessment Act 1997; and

(ii) that occurred after 11.45 am by legal time in the Australian Capital Territory on 21 September 1999; and

(d) just before the entity ceases to be a subsidiary member of the group, the asset is still a pre‑CGT asset and is held by the head company only because the entity is taken by subsection 701‑1(1) (the single entity rule) of the Income Tax Assessment Act 1997 to be a part of the head company.

(2) If this section applies, the head company may, in relation to the entity’s ceasing to be a subsidiary member, choose that the terminating value for the asset, that is to be used in applying step 1 of the table in section 711‑20 of the Income Tax Assessment Act 1997, is equal to its market value just before the transitional group came into existence.

Table of sections

702‑1 Modified application of section 40‑77 of this Act to assets that an entity brings into a consolidated group

702‑5 Modified application of subsection 40‑285(6) of this Act after entity brings assets into consolidated group

(1) This section applies if:

(a) an entity becomes a subsidiary member of a consolidated group; and

(b) just before it does so, section 40‑77 of this Act applies to an asset that it holds.

(2) For so long as the asset continues to be:

(a) an asset of the head company because subsection 701‑1(1) (the single entity rule) of the Income Tax Assessment Act 1997 applies; or