Taxation Laws Amendment Act (No. 3) 2001

No. 73, 2001

Taxation Laws Amendment Act (No. 3) 2001

No. 73, 2001

Taxation Laws Amendment Act (No. 3) 2001

No. 73, 2001

An Act to amend the law relating to taxation, and for related purposes

Contents

1 Short title...................................

2 Commencement...............................

3 Schedule(s)..................................

Schedule 1—Amendments relating to the goods and services tax

Part 1—GST returns and payments

A New Tax System (Goods and Services Tax) Act 1999

Taxation Administration Act 1953

Part 2—Payment of GST by instalments

A New Tax System (Goods and Services Tax) Act 1999

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Part 3—Substituted accounting periods

A New Tax System (Goods and Services Tax) Act 1999

Part 4—Correction of errors

A New Tax System (Goods and Services Tax) Act 1999

Part 5—Phasing in input tax credits for motor vehicles etc.

A New Tax System (Goods and Services Tax Transition) Act 1999

Schedule 2—Pay as you go instalments

Part 1—Paying instalments using GDP‑adjusted notional tax

Taxation Administration Act 1953

Income Tax Assessment Act 1997

Part 2—Transitional rules

Part 3—Consequential amendments

Income Tax Assessment Act 1936

Taxation Administration Act 1953

Schedule 3—Deferral of due dates

Part 1—Amendments

Fringe Benefits Tax Assessment Act 1986

Income Tax Assessment Act 1936

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Part 2—Transitional rules

Part 3—Weekends and public holidays

Income Tax Assessment Act 1997

Taxation Administration Act 1953

Schedule 4—Amendments relating to Treasury Note yield rate and general interest charge

Part 1—Amendment of the Taxation Administration Act 1953

Taxation Administration Act 1953

Part 2—Consequential amendments of other Acts

Diesel and Alternative Fuels Grants Scheme Act 1999

Income Tax Assessment Act 1936

Product Grants and Benefits Administration Act 2000

Part 3—Application

Schedule 5—Technical amendments

Taxation Administration Act 1953

Taxation Laws Amendment Act (No. 3) 2001

No. 73, 2001

An Act to amend the law relating to taxation, and for related purposes

[Assented to 30 June 2001]

The Parliament of Australia enacts:

This Act may be cited as the Taxation Laws Amendment Act (No. 3) 2001.

(1) Subject to this section, this Act commences on the day on which it receives the Royal Assent.

(1A) Part 5 of Schedule 1 is taken to have commenced on 23 May 2001.

(2) Items 48 to 52 of Schedule 2 are taken to have commenced on 1 January 2001.

(3) Part 3 of Schedule 3 is taken to have commenced on 1 April 2001.

Subject to section 2, each Act that is specified in a Schedule to this Act is amended or repealed as set out in the applicable items in the Schedule concerned, and any other item in a Schedule to this Act has effect according to its terms.

Schedule 1—Amendments relating to the goods and services tax

Part 1—GST returns and payments

A New Tax System (Goods and Services Tax) Act 1999

1 After section 31‑5

Insert:

31‑8 When GST returns must be given—quarterly tax periods

(1) If a tax period applying to you is a *quarterly tax period, you must give your *GST return for the tax period to the Commissioner:

(a) as provided in the following table; or

(b) within such further period as the Commissioner allows.

When quarterly GST returns must be given | ||

Item | If this day falls within the quarterly tax period … | Give the GST return to the Commissioner on or before this day: |

1 | 1 September | the following 28 October |

2 | 1 December | the following 28 February |

3 | 1 March | the following 28 April |

4 | 1 June | the following 28 July |

(2) A tax period is a quarterly tax period if:

(a) it is a period of 3 months; or

(b) it would be a period of 3 months but for the application of section 27‑30 or 27‑35.

Note: Under section 27‑30, a tax period can be determined to take account of changes in tax periods. Under section 27‑35, the start or finish of a 3 month tax period can vary by up to 7 days from the start or finish of a normal quarter.

2 Section 31‑10 (heading)

Repeal the heading, substitute:

31‑10 When GST returns must be given—other tax periods

3 Subsection 31‑10(1)

After “a tax period”, insert “(other than a *quarterly tax period)”.

4 Subsection 31‑15(1)

Repeal the subsection, substitute:

(1) Your *GST return for a tax period must be in the *approved form.

5 Subsection 31‑20(2)

Repeal the subsection, substitute:

(2) The *approved form for a further or fuller *GST return may require information to be provided relating to:

(a) the tax period to which the return relates; or

(b) one or more preceding tax periods; or

(c) both the tax period to which the return relates, and one or more preceding tax periods.

6 After section 33‑1

Insert:

33‑3 When payments of net amounts must be made—quarterly tax periods

If:

(a) the *net amount for a tax period applying to you is greater than zero; and

(b) the tax period is a *quarterly tax period;

you must pay the net amount to the Commissioner as follows:

When quarterly GST payments must be made | ||

Item | If this day falls within the quarterly tax period … | Pay the net amount to the Commissioner on or before this day: |

1 | 1 September | the following 28 October |

2 | 1 December | the following 28 February |

3 | 1 March | the following 28 April |

4 | 1 June | the following 28 July |

7 Section 33‑5 (heading)

Repeal the heading, substitute:

33‑5 When payments of net amounts must be made—other tax periods

8 Subsection 33‑5(1)

After “a tax period”, insert “(other than a *quarterly tax period)”.

9 Subsections 33‑10(1) and (2)

Omit “under section 33‑5”.

10 Section 35‑10

Omit “under section 31‑5 or 31‑20”.

11 Subsections 51‑50(2), (2A) and (3)

Repeal the subsections, substitute:

(2) However, while an election made by the *joint venture operator under section 51‑52 has effect, the joint venture operator must, in relation to all the *GST joint ventures for which the joint venture operator is the joint venture operator, give to the Commissioner a single *GST return for each tax period applying to the joint venture operator.

(3) This section has effect despite section 31‑5 (which is about who must give GST returns).

12 Paragraph 51‑55(1)(b)

Omit “section 33‑5”, substitute “section 33‑3 or 33‑5 (as the case requires)”.

13 Subsection 54‑55(2)

Repeal the subsection.

14 Subsection 54‑55(4)

Repeal the subsection, substitute:

(4) This section has effect despite section 31‑5 (which is about who must give GST returns).

15 Paragraph 54‑60(1)(b)

Omit “section 33‑5”, substitute “section 33‑3 or 33‑5 (as the case requires)”.

16 Subsection 78‑85(2)

Repeal the subsection.

17 Subsection 78‑85(3)

Omit “, 31‑10 and 31‑15”, substitute “and 31‑10”.

18 Subsection 105‑15(2)

Repeal the subsection.

19 Subsection 105‑15(3)

Omit “, 31‑10 and 31‑15”, substitute “and 31‑10”.

20 Section 195‑1

Insert:

quarterly tax period has the meaning given by subsection 31‑8(2).

Taxation Administration Act 1953

21 Subsection 70(1AAB)

Omit “that states a net amount”.

22 Application

The amendments made by this Part of this Schedule apply, and are taken to have applied, in relation to GST returns, and net amounts, for tax periods ending on or after 22 February 2001.

Part 2—Payment of GST by instalments

A New Tax System (Goods and Services Tax) Act 1999

23 Section 17‑99 (after table item 9A)

Insert:

9B | Payment of GST by instalments | Division 162 |

24 Section 27‑99 (after table item 1)

Insert:

1AA | Payment of GST by instalments | Division 162 |

25 Section 31‑99 (after table item 4)

Insert:

4A | Payment of GST by instalments | Division 162 |

26 Section 33‑99 (after table item 5)

Insert:

5A | Payment of GST by instalments | Division 162 |

27 Section 37‑1 (after table item 21)

Insert:

21A | Payment of GST by instalments | Division 162 |

28 At the end of subsection 126‑5(3)

Add:

Note: If you are a *GST instalment payer your net amount is reduced by GST instalments you have paid: see section 162‑105.

29 Before Division 165

Insert:

Division 162—Payment of GST by instalments

Table of Subdivisions

162‑A Electing to pay GST by instalments

162‑B Consequences of electing to pay GST by instalments

162‑C GST instalments

162‑D Penalty payable in certain cases if varied instalment amounts are too low

162‑1 What this Division is about

You may be able to elect to pay GST by instalments. If you do, GST returns are given to the Commissioner annually, and quarterly instalments of GST are paid on the basis of the Commissioner’s or your estimates of what your annual GST liability will be (followed by a reconciliation based on the annual GST return).

If you can average your income for income tax purposes, you only pay the last 2 quarterly instalments.

Note: In some cases, you will only pay the last 2 quarterly instalments: see section 162‑105.

Subdivision 162‑A—Electing to pay GST by instalments

162‑5 Eligibility to elect to pay GST by instalments

(1) You are eligible to elect to pay GST by instalments if:

(a) you do not exceed the *instalment turnover threshold; and

(b) the current tax period applying to you is not affected by:

(i) an election under section 27‑10 (election of one month tax periods); or

(ii) a determination under section 27‑15 (determination of one month tax periods); or

(iii) a determination under section 27‑37 (special determination of tax periods on request); and

(c) your *current GST lodgment record is at least 4 months; and

(d) you have complied with all your obligations to give *GST returns to the Commissioner; and

(e) you are not in a *net refund position.

(2) The instalment turnover threshold is:

(a) $2 million; or

(b) such higher amount as the regulations specify.

(3) You are in a net refund position if the sum of all your *net amounts is less than zero, for the tax periods for which *GST returns fell due during the period referred to in the relevant item in the third column of this table.

When you are in a net refund position | ||

Item | If your *current GST lodgment record is… | Take into account this period to work out whether you are in a net refund position: |

1 | at least 13 months | the 12 months preceding the current tax period applying to you |

2 | at least 10 months, but less than 13 months | the 9 months preceding that current tax period |

3 | at least 7 months, but less than 10 months | the 6 months preceding that current tax period |

4 | less than 7 months | the 3 months preceding that current tax period |

(4) In working out *net amounts for the purposes of subsection (3), disregard any entitlements you had to special credits, under section 16 of the A New Tax System (Goods and Services Tax Transition) Act 1999, that were attributable to any of the tax periods referred to in that subsection.

162‑10 Your current GST lodgment record

(1) If you are not a *member of a *GST group, your current GST lodgment record is the period, immediately preceding the current tax period applying to you, that is covered by tax periods applying to you for which you have given *GST returns to the Commissioner.

(2) If you are a *member of a *GST group, your current GST lodgment record is the period, immediately preceding the current tax period applying to you, that is covered by tax periods applying to you:

(a) for which you have given *GST returns to the Commissioner; and

(b) during which the membership of the GST group has not changed.

(3) However, if you have been (but are not currently) the *representative member of a *GST group, any tax periods applying to you during which you were such a representative member are not to be counted towards your current GST lodgment record.

162‑15 Electing to pay GST by instalments

(1) You may, by notifying the Commissioner in the *approved form, elect to pay GST by instalments if you are eligible under section 162‑5.

(2) However, the Commissioner may disallow your election, even though you are eligible under section 162‑5, if the Commissioner is satisfied that you have a history of failing to comply with your obligations under a *taxation law.

Note: Disallowing your election is a reviewable GST decision (see Division 7 of Part VI of the Taxation Administration Act 1953).

(3) If your election is disallowed, it is taken never to have had effect.

(4) Your election cannot relate to more than one *financial year.

162‑20 Elections by representative members of GST groups

(1) A *representative member of a *GST group cannot elect to pay GST by instalments unless each *member of the GST group is eligible under section 162‑5.

(2) If the *representative member makes such an election, the *instalment tax period applying to the representative member also applies to each member. However, the members other than the representative member are not *GST instalment payers.

162‑25 When you must make your election

(1) You must make your election on or before 28 October in the *financial year to which it relates.

(2) However, if:

(a) during the *financial year but after 28 October in that financial year, you became eligible under section 162‑5 to elect to pay GST by instalments; and

(b) this subsection had not applied to you before; and

(c) your *current GST lodgment record is not more than 6 months;

you must make your election on or before the first day, after becoming eligible under section 162‑5, on which you would, but for this Division, be required under section 31‑8 to give a *GST return to the Commissioner.

(3) The Commissioner may, in accordance with a request you make in the *approved form, allow you to make your election on a specified day occurring after the day provided for under subsection (1) or (2).

Note: Refusing a request to be allowed to make an election on a specified day under this subsection is a reviewable GST decision (see Division 7 of Part VI of the Taxation Administration Act 1953).

162‑30 Duration of your election

(1) Your election has effect, and is taken to have had effect, for the whole of the *financial year in question.

(2) However, if:

(a) you make your election after 28 October in that *financial year; and

(b) part of that financial year is already covered by one or more tax periods for which you have given the Commissioner a *GST return;

your election has effect, and is taken to have had effect, only for the part of that financial year that is not covered by those tax periods.

(3) Your election does not cease to have effect because, after making the election, you exceed the *instalment turnover threshold at any time.

Subdivision 162‑B—Consequences of electing to pay GST by instalments

(1) You are a GST instalment payer while an election that you have made under section 162‑15 has effect.

(2) You are a GST instalment payer for the *financial year for which your election has effect.

(3) However, if your election has effect only for part of a *financial year, you are a GST instalment payer only for that part of that financial year.

162‑55 Tax periods for GST instalment payers

(1) The tax period that applies to you, if you are a *GST instalment payer for a *financial year, is that financial year.

(2) The tax period that applies to you, if you are a *GST instalment payer only for part of a *financial year, is that part of that financial year.

(3) A tax period under this section is an instalment tax period.

(4) This section has effect despite sections 27‑5, 27‑10, 27‑15 and 27‑30 (which are about tax periods).

162‑60 When GST returns for GST instalment payers must be given

(1) You must give your *GST return for the *instalment tax period to the Commissioner:

(a) if you are required under section 161 of the *ITAA 1936 to lodge a return in relation to a year of income corresponding to, or ending during, an instalment tax period applying to you—within the period, specified in the notice published in the Gazette under that section, for you to lodge as required under that section; or

(b) if paragraph (a) does not apply—on or before the 28 February following the end of the instalment tax period.

Note: Section 388‑55 in Schedule 1 to the Taxation Administration Act 1953 allows the Commissioner to defer the time for giving the GST return.

(2) However, in relation to an *instalment tax period that:

(a) ends on 30 June 2001; or

(b) would have ended on 30 June 2001 but for the application of section 27‑35;

the period referred to in paragraph (1)(a) that would otherwise end after 28 February 2002 is taken to end on that day.

Note: Under section 27‑35, the start or finish of a 3 month tax period could vary by up to 7 days from the start or finish of a normal quarter.

(3) This section has effect despite sections 31‑8 and 31‑10 (which are about when GST returns must be given).

162‑65 The form and contents of GST returns for GST instalment payers

(1) If you are a *GST instalment payer only for part of a *financial year, the *approved form for your *GST return for the *instalment tax period consisting of that part of the financial year may require that the return relate to:

(a) the instalment tax period; and

(b) the one or more preceding tax periods applying to you that fall within the financial year;

as if they are a single tax period consisting of the whole of the financial year.

(2) This section has effect in addition to, and does not limit the scope of, section 31‑15 (which is about the form and contents of GST returns).

162‑70 Payment of GST instalments

(1) If you are a *GST instalment payer, you must, for each *instalment tax period applying to you, pay to the Commissioner an amount (your GST instalment) for each *GST instalment quarter of the instalment tax period.

Note 1: GST instalments are worked out under Subdivision 162‑C.

Note 2: Entities covered by section 162‑80 only pay GST instalments on the last 2 GST instalment quarters.

(2) These are the GST instalment quarters for an *instalment tax period:

(a) the 3 months ending on 30 September during the period;

(b) the 3 months ending on 31 December during the period;

(c) the 3 months ending on 31 March during the period;

(d) the 3 months ending on 30 June during the period.

(3) However, if the *instalment tax period is only part of a *financial year, any 3 month periods referred to in subsection (2) that do not form part of the instalment tax period are not GST instalment quarters of the instalment tax period.

(4) You must pay your *GST instalment to the Commissioner as follows:

When GST instalments must be paid | ||

Item | If the GST instalment quarter ends on this day … | Pay the GST instalment to the Commissioner on or before this day: |

1 | 30 September | the following 28 October |

2 | 31 December | the following 28 February |

3 | 31 March | the following 28 April |

4 | 30 June | the following 28 July |

Note: Section 255‑10 in Schedule 1 to the Taxation Administration Act 1953 allows the Commissioner to defer the time for payment of the GST instalment.

(5) You may pay by *electronic payment any *GST instalments payable by you. Any amounts of a GST instalment that you do not pay by electronic payment must be paid in the manner determined in writing by the Commissioner.

162‑75 Giving notices relating to GST instalments

If:

(a) you are required to pay a *GST instalment; and

(b) the Commissioner requires you to give a notice relating to the GST instalment;

you must give the notice to the Commissioner, in the *approved form, on or before the day on which you are required to pay the GST instalment.

162‑80 Certain entities pay only 2 GST instalments for each year

(1) If:

(a) you are a *GST instalment payer for an *instalment tax period; and

(b) subsection (2) applies to you;

section 162‑70 has effect as if you are only required to pay *GST instalments for the last 2 *GST instalment quarters for the instalment tax period.

(2) This subsection applies to you if:

(a) both of the following conditions are satisfied:

(i) you are carrying on a *primary production business in an *income year corresponding to, or ending during, the *instalment tax period;

(ii) the *assessable income that was *derived from, or resulted from, a primary production business that you carried on in the *base year exceeded the amount of so much of your deductions in that year that are reasonably related to that income; or

(b) both of the following conditions are satisfied:

(i) you are a *special professional in an income year corresponding to, or ending during, the instalment tax period;

(ii) your *assessable professional income in the base year exceeded the amount of so much of your deductions in that year that are reasonably related to that income.

162‑85 A GST instalment payer’s concluding tax period

(1) If any of the following occurs:

(a) a *GST instalment payer who is an individual dies;

(b) a GST instalment payer ceases to *carry on any *enterprise;

(c) a GST instalment payer’s *registration is cancelled;

during an *instalment tax period applying to the GST instalment payer, the instalment tax period is not affected by the death, cessation or cancellation.

(2) However, any requirement to pay *GST instalments for a *GST instalment quarter of the *instalment tax period does not apply if the GST instalment quarter commences after:

(a) the death or cessation occurred; or

(b) the cancellation took effect.

(3) This section has effect despite sections 27‑40 (which is about an entity’s concluding tax period) and 162‑70.

(4) However, this section does not affect the application of those sections if:

(a) a *GST instalment payer who is an individual becomes bankrupt; or

(b) a GST instalment payer that is not an individual goes into liquidation or receivership or for any reason ceases to exist.

162‑90 The effect of bankruptcy, liquidation or receivership etc.

(1) If:

(a) a *GST instalment payer who is an individual becomes bankrupt; or

(b) a GST instalment payer that is not an individual goes into liquidation or receivership or for any reason ceases to exist;

the GST instalment payer must give the *GST return, for the *instalment tax period that ends because of the bankruptcy, liquidation, receivership or cessation, to the Commissioner:

(c) on or before the 21st day of the month following the end of the instalment tax period; or

(d) within such further period as the Commissioner allows.

(2) If the *net amount for the *instalment tax period is greater than zero, the *GST instalment payer must pay the net amount to the Commissioner on or before the 21st day of the month following the end of the instalment tax period.

(3) This section has effect despite sections 162‑60 (which is about when GST instalment payers must give GST returns) and 162‑110 (which is about when GST instalment payers must pay net amounts).

162‑95 The effect of changing the membership of GST groups

(1) If you are:

(a) a *GST instalment payer; and

(b) a *member of a *GST group whose membership changes during an *instalment tax period applying to you;

the instalment tax period ends when the membership of the GST group changes.

(2) The *representative member of the *GST group must give the *GST return for the *instalment tax period to the Commissioner:

(a) on or before the 21st day of the month following the end of the instalment tax period; or

(b) within such further period as the Commissioner allows.

(3) If the *net amount for the *instalment tax period is greater than zero, the *representative member of the *GST group must pay the net amount to the Commissioner on or before the 21st day of the month following the end of the instalment tax period.

(4) This section has effect despite sections 162‑55 (which is about tax periods for GST instalment payers), 162‑60 (which is about when GST instalment payers must give GST returns) and 162‑110 (which is about when GST instalment payers must pay net amounts).

162‑100 General interest charge on late payment

If you fail to pay some or all of a *GST instalment by the time by which the GST instalment is due to be paid, you are liable to pay the *general interest charge on the unpaid amount for each day in the period that:

(a) started at the beginning of the day by which the GST instalment was due to be paid; and

(b) finishes at the end of the last day on which, at the end of the day, any of the following remains unpaid:

(i) the GST instalment;

(ii) general interest charge on any of the instalment.

162‑105 Net amounts for GST instalment payers

If you are a *GST instalment payer, your *net amount for an *instalment tax period is the difference between:

(a) the amount that, but for this section, would be your *net amount under section 17‑5 or 126‑5 for the instalment tax period; and

(b) the sum of all of the *GST instalments payable by you for the *GST instalment quarters of the instalment tax period.

162‑110 When payments of net amounts must be made—GST instalment payers

(1) If:

(a) you are a *GST instalment payer; and

(b) the *net amount for an *instalment tax period applying to you is greater than zero;

you must pay the net amount to the Commissioner on or before the day on which, under section 162‑60, you are required to give to the Commissioner your *GST return for the instalment tax period.

(2) This section has effect despite sections 33‑3 and 33‑5 (which are about when payments of net amounts are made).

Subdivision 162‑C—GST instalments

162‑130 What are your GST instalments

(1) If you are a *GST instalment payer, your *GST instalments for the *GST instalment quarters of an *instalment tax period applying to you are worked out under subsections (2) and (3).

(2) Your *GST instalment for the first *GST instalment quarter is whichever of the following you choose:

(a) your *notified instalment amount for the GST instalment quarter; or

(b) your *varied instalment amount for the GST instalment quarter.

(3) Your *GST instalment for any other *GST instalment quarter is:

(a) if you have a *notified instalment amount for the GST instalment quarter—whichever of the following you choose:

(i) your notified instalment amount for the GST instalment quarter; or

(ii) your *varied instalment amount for the GST instalment quarter; or

(b) if you do not have a notified instalment amount for the GST instalment quarter—whichever of the following you choose:

(i) 25% of your *estimated annual GST amount relating to the preceding GST instalment quarter; or

(ii) your varied instalment amount for the GST instalment quarter.

Note: Subsection 162‑135(2) sets out when you will not have a notified instalment amount for a GST instalment quarter.

162‑135 Notified instalment amounts

(1) Your notified instalment amount for a *GST instalment quarter is the amount that is:

(a) worked out by the Commissioner; and

(b) notified by the Commissioner to you before the day on which the *GST instalment is due.

(2) However, the Commissioner is not to work out or notify a *notified instalment amount for a *GST instalment quarter if you had a *varied instalment amount for an earlier GST instalment quarter of the same *instalment tax period.

162‑140 Varied instalment amounts

(1) You may, by notifying the Commissioner in the *approved form, substitute another amount for:

(a) your *notified instalment amount for a *GST instalment quarter; or

(b) if paragraph 162‑130(3)(b) applies to a GST instalment quarter—your *GST instalment for the preceding GST instalment quarter.

The amount substituted is your varied instalment amount for the GST instalment quarter.

(2) The amount substituted must not be less than zero.

(3) You must give the notice to the Commissioner on or before the day on which the *GST instalment for the *GST instalment quarter is due.

(4) You must include in the notice an estimate of your *annual GST liability relating to the *instalment tax period in question. This estimate is your estimated annual GST amount relating to the *GST instalment quarter.

Note: You may be liable to penalty under Subdivision 162‑D if your variation of the notified instalment amount is too much of an underestimate of your total GST liability.

(5) However, if paragraph 162‑130(3)(b) applies to a *GST instalment quarter but you do not, under subsection (1) of this section, substitute another amount by notifying the Commissioner in the *approved form:

(a) your varied instalment amount for the GST instalment quarter is 25% of your *estimated annual GST amount relating to the preceding GST instalment quarter; and

(b) your estimated annual GST amount relating to the GST instalment quarter is your *estimated annual GST amount relating to the preceding GST instalment quarter.

162‑145 Your annual GST liability

(1) Your annual GST liability, for an *instalment tax period that is a *financial year, is the amount that would be your *net amount for the period if it were not reduced under section 162‑105.

(2) Your annual GST liability, for an *instalment tax period that is only part of a *financial year, is the sum of:

(a) the amount that would be your *net amount for the period if it were not reduced under section 162‑105; and

(b) your *early net amounts for the financial year (subtracting any of those amounts that are less than zero).

(3) Your early net amounts for the *financial year are your *net amounts for any tax periods that:

(a) started, or would but for section 27‑35 have started, at the start of or during that financial year; and

(b) ended before the start of the *instalment tax period applying to you that forms part of that financial year.

Note: Under section 27‑35, the start or finish of a 3 month tax period could vary by up to 7 days from the start or finish of a normal quarter.

Subdivision 162‑D—Penalty payable in certain cases if varied instalment amounts are too low

162‑170 What this Subdivision is about

There are 3 circumstances where a penalty can arise if a varied instalment amount is too low:

(a) your payments are too low a proportion of your annual GST liability (see section 162‑175);

(b) your estimated annual GST amount is too low a proportion of your annual GST liability (see section 162‑180);

(c) the varied instalment amount is too low a proportion of your estimated annual GST amount (see section 162‑185).

The penalty is based on the general interest charge rate, and the machinery provisions of Division 298 in Schedule 1 to the Taxation Administration Act 1953 apply.

Note: This section is an explanatory section.

162‑175 GST payments are less than 85% of annual GST liability

(1) You are liable to pay a penalty, for a *GST instalment quarter of an *instalment tax period applying to you, if you have a *varied instalment amount for the GST instalment quarter, and:

(a) if the instalment tax period is a *financial year—the sum of your *GST instalments for all the GST instalment quarters of the instalment tax period is less than 85% of your *annual GST liability for the instalment tax period; or

(b) if the instalment tax period is only part of a financial year—the sum of:

(i) your *GST instalments for all the GST instalment quarters of the instalment tax period; and

(ii) your *early net amounts for the financial year (subtracting any of those amounts that are less than zero);

is less than 85% of your annual GST liability for the instalment tax period.

(2) The amount of the penalty, for a particular day, is worked out by applying the *general interest charge:

(a) for each day in the period in section 162‑190; and

(b) in the way set out in subsection 8AAC(4) of the Taxation Administration Act 1953;

to your *GST instalment shortfall, under this section, for the *GST instalment quarter.

(3) Your GST instalment shortfall, under this section, for the *GST instalment quarter is the amount worked out as follows:

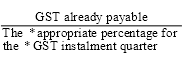

where:

GST already payable is the sum of:

(a) the *varied instalment amount; and

(b) all your other *GST instalments (if any) for earlier *GST instalment quarters of the *instalment tax period in question; and

(c) if the instalment tax period is only part of a *financial year—your *early net amounts for the financial year (subtracting any of those amounts that are less than zero).

(4) However, if:

(a) the *GST instalment quarter is not the first GST instalment quarter of the *instalment tax period in question; and

(b) you are liable for one or more penalties under this section in relation to any of the earlier GST instalment quarters of the instalment tax period;

then:

(c) your GST instalment shortfall, under this section, for the *GST instalment quarter is the difference between:

(i) the amount worked out using the formula in subsection (3); and

(ii) the sum of all your GST instalment shortfalls for those earlier GST instalment quarters; and

(d) if that sum is greater than the amount worked out using the formula in subsection (3)—you are not liable to pay a penalty under this section in relation to the GST instalment quarter.

(5) The appropriate percentage for a *GST instalment quarter is:

(a) if the GST instalment quarter ends on 30 September—25%; or

(b) if the GST instalment quarter ends on 31 December—50%; or

(c) if the GST instalment quarter ends on 31 March—75%; or

(d) if the GST instalment quarter ends on 30 June—100%.

162‑180 Estimated annual GST amount is less than 85% of annual GST liability

(1) You are liable to pay a penalty, for a *GST instalment quarter of an *instalment tax period applying to you, if:

(a) you have a *varied instalment amount for the GST instalment quarter; and

(b) you are not liable to pay a penalty, for the GST instalment quarter, under section 162‑175; and

(c) your *estimated annual GST amount relating to the GST instalment quarter is less than:

(i) 85% of your *annual GST liability for the instalment tax period; or

(ii) if the GST instalment quarter ends on 30 September 2001—75% of your *annual GST liability for the instalment tax period; and

(d) the varied instalment amount is less than or equal to 25% of your annual GST liability for the instalment tax period.

(2) The amount of the penalty, for a particular day, is worked out by applying the *general interest charge:

(a) for each day in the period in section 162‑190; and

(b) in the way set out in subsection 8AAC(4) of the Taxation Administration Act 1953;

to your *GST instalment shortfall, under this section, for the *GST instalment quarter.

(3) Your GST instalment shortfall, under this section, for the *GST instalment quarter is the amount worked out as follows:

(4) However, if:

(a) the *GST instalment quarter is not the first GST instalment quarter of the *instalment tax period in question; and

(b) you are liable for one or more penalties under this section in relation to any of the earlier GST instalment quarters of the instalment tax period;

then:

(c) your GST instalment shortfall, under this section, for the *GST instalment quarter is the difference between:

(i) the amount worked out using the formula in subsection (3); and

(ii) the sum of all your GST instalment shortfalls for those earlier GST instalment quarters; and

(d) if that sum is greater than the amount worked out using the formula in subsection (3)—you are not liable to pay a penalty under this section in relation to the GST instalment quarter.

(5) For the purpose of working out your *GST instalment shortfall under this section, your *estimated annual GST amount relating to the *GST instalment quarter is taken to be the amount worked out as follows, if the amount is less than that estimated annual GST amount:

where:

GST already payable is the sum of:

(a) the *varied instalment amount in question; and

(b) all your other *GST instalments (if any) for earlier *GST instalment quarters of the *instalment tax period in question; and

(c) if the instalment tax period is only part of a *financial year—your *early net amounts for the financial year (subtracting any of those amounts that are less than zero).

162‑185 Shortfall in GST instalments worked out on the basis of estimated annual GST amount

(1) You are liable to pay a penalty, for a *GST instalment quarter of an *instalment tax period applying to you, if:

(a) you have a *varied instalment amount for the GST instalment quarter; and

(b) you are not liable to pay a penalty, for the GST instalment quarter, under section 162‑175 or 162‑180; and

(c) the amount worked out by multiplying your *estimated annual GST amount relating to the GST instalment quarter by the *appropriate percentage for the GST instalment quarter exceeds the sum of:

(i) the varied instalment amount; and

(ii) all your other *GST instalments (if any) for earlier GST instalment quarters of the *instalment tax period in question; and

(iii) if the instalment tax period is only part of a *financial year—your *early net amounts for the financial year (subtracting any of those amounts that are less than zero).

(2) The amount of the penalty, for a particular day, is worked out by applying the *general interest charge:

(a) for each day in the period in section 162‑190; and

(b) in the way set out in subsection 8AAC(4) of the Taxation Administration Act 1953;

to your *GST instalment shortfall, under this section, for the *GST instalment quarter.

(3) Your GST instalment shortfall, under this section, for the *GST instalment quarter is the amount of the excess referred to in paragraph (1)(c).

162‑190 Periods for which penalty is payable

You are liable to pay the penalty under this Subdivision for each day in the period that:

(a) started at the beginning of the day by which the *GST instalment, for the *GST instalment quarter to which the charge relates, was due to be paid; and

(b) finishes at the end of the day before which you must, under section 162‑110, pay to the Commissioner your *net amount for the *instalment tax period that includes that GST instalment quarter.

(1) This section reduces your *GST instalment shortfall, for a *GST instalment quarter of an *instalment tax period applying to you, if:

(a) you are liable to pay a penalty under section 162‑175 or 162‑180 for a *GST instalment quarter of an *instalment tax period applying to you; and

(b) for that or any other GST instalment quarter of an *instalment tax period:

(i) you have a *notified instalment amount that is less than 25% of your *annual GST liability for the instalment tax period; or

(ii) you do not have a notified instalment amount, but the Commissioner is satisfied that, if you had such a notified instalment amount, it would be less than 25% of your annual GST liability for the instalment tax period.

(2) The *GST instalment shortfall is reduced by the amount worked out as follows:

where:

notified and other amounts is the sum of:

(a) the *notified instalment amount, or, if you do not have a notified instalment amount for the *GST instalment quarter, the amount that the Commissioner is satisfied would have otherwise been that notified instalment amount; and

(b) for each of the earlier GST instalment quarters (if any) of the *instalment tax period in question:

(i) the notified instalment amount; or

(ii) if you do not have a notified instalment amount for the *GST instalment quarter—the amount that the Commissioner is satisfied would have otherwise been that notified instalment amount; and

(c) if the instalment tax period is only part of a *financial year—your *early net amounts for the financial year (subtracting any of those amounts that are less than zero).

(3) If, because of the reduction, your *GST instalment shortfall for the *GST instalment quarter is zero or less than zero, you are not liable to pay a penalty under section 162‑175 or 162‑180 (as the case requires) in relation to the GST instalment quarter.

(4) If both this section and section 162‑200 apply to a particular *GST instalment shortfall, apply this section to the shortfall before applying section 162‑200.

162‑200 Reduction in penalties if GST instalment shortfall is made up in a later instalment

(1) This section reduces your *GST instalment shortfall, for a *GST instalment quarter of an *instalment tax period applying to you, if:

(a) you pay to the Commissioner a *GST instalment for a later GST instalment quarter of the instalment tax period; and

(b) that GST instalment exceeds 25% of your *annual GST liability for the instalment tax period.

The amount of that excess is called the top up.

(2) The *GST instalment shortfall is reduced by applying so much of the top up as does not exceed the GST instalment shortfall.

(3) However, if some of the top up has already been applied (under any other application or applications of this section) to reduce a *GST instalment shortfall for a different *GST instalment quarter of the *instalment tax period, the GST instalment shortfall is reduced by applying so much of the top up as has not already been applied, and does not exceed the GST instalment shortfall.

(4) The reduction under subsection (2) has effect for each day in the period that:

(a) started at the beginning of the day on which you paid the *GST instalment for the later *GST instalment quarter; and

(b) finishes at the end of the day before which you must, under section 162‑110, pay to the Commissioner your *net amount for the *instalment tax period.

162‑205 This Subdivision does not create a liability for general interest charge

For the avoidance of doubt, this Subdivision does not have the effect of making you liable to pay the *general interest charge.

30 Section 188‑5 (at the end of the table)

Add:

5 | Instalment turnover threshold | whether you can elect to pay GST by instalments (see subsection 162‑5(2)) |

31 Paragraph 188‑10(3)(a) (first occurring)

Reletter as paragraph (aa).

32 Before paragraph 188‑10(3)(b)

Insert:

(ab) the *instalment turnover threshold;

33 Section 195‑1

Insert:

annual GST liability, for an *instalment tax period, has the meaning given by section 162‑145.

34 Section 195‑1

Insert:

average income has the meaning given by subsection 392‑45(1) of the *ITAA 1997.

35 Section 195‑1

Insert:

appropriate percentage, for a *GST instalment quarter, has the meaning given by subsection 162‑175(5).

36 Section 195‑1

Insert:

assessable income has the meaning given by subsection 995‑1(1) of the *ITAA 1997.

37 Section 195‑1

Insert:

assessable professional income has the meaning given by subsection 405‑20(1) of the *ITAA 1997.

38 Section 195‑1

Insert:

base year has the meaning given by sections 45‑320 and 45‑470 in Schedule 1 to the Taxation Administration Act 1953.

39 Section 195‑1

Insert:

current GST lodgment record has the meaning given by section 162‑10.

40 Section 195‑1

Insert:

derived has a meaning affected by subsection 6‑5(4) of the *ITAA 1997.

41 Section 195‑1

Insert:

early net amount has the meaning given by subsection 162‑145(3).

42 Section 195‑1

Insert:

estimated annual GST amount has the meaning given by subsection 162‑140(4) and paragraph 162‑140(5)(b).

43 Section 195‑1

Insert:

general interest charge means the charge worked out under Division 1 of Part IIA of the Taxation Administration Act 1953.

44 Section 195‑1

Insert:

GST instalment has the meaning given by subsection 162‑70(1).

45 Section 195‑1

Insert:

GST instalment payer has the meaning given by section 162‑50.

46 Section 195‑1

Insert:

GST instalment quarter has the meaning given by subsections 162‑70(2) and (3).

47 Section 195‑1

Insert:

GST instalment shortfall, for a *GST instalment quarter in relation to which you are liable to pay a penalty under Subdivision 162‑D, means:

(a) if the penalty is payable under section 162‑175—the amount worked out under subsection 162‑175(3) or paragraph 162‑175(4)(c) (whichever is applicable); or

(b) if the penalty is payable under section 162‑180—the amount worked out under subsection 162‑180(3) or paragraph 162‑180(4)(c) (whichever is applicable); or

(c) if the penalty is payable under section 162‑185—the amount worked out under subsection 162‑185(3).

Note: The amount of a GST instalment shortfall can be reduced under section 162‑195 or 162‑200 (or both).

48 Section 195‑1

Insert:

instalment tax period has the meaning given by subsection 162‑55(3).

49 Section 195‑1

Insert:

instalment turnover threshold has the meaning given by subsection 162‑5(2).

50 Section 195‑1 (definition of net amount)

Omit “section 17‑5 and 126‑5”, substitute “sections 17‑5, 126‑5 and 162‑105”.

51 Section 195‑1

Insert:

net refund position has the meaning given by subsection 162‑5(3).

52 Section 195‑1

Insert:

notified instalment amount has the meaning given by subsection 162‑135(1).

53 Section 195‑1

Insert:

primary production business has the meaning given by subsection 995‑1(1) of the *ITAA 1997.

54 Section 195‑1

Insert:

special professional has the meaning given by subsection 405‑25(1) of the *ITAA 1997.

55 Section 195‑1

Insert:

varied instalment amount has the meaning given by subsection 162‑140(1) and paragraph 162‑140(5)(a).

Income Tax Assessment Act 1997

56 After paragraph 25‑5(1)(c)

Insert:

(ca) a penalty under Subdivision 162‑D of the *GST Act; or

57 At the end of section 26‑5

Add:

(2) This section does not apply to an amount payable, by way of penalty, under Subdivision 162‑D of the *GST Act.

Note: See paragraph 25‑5(1)(c) for the deductibility of penalties under Subdivision 162‑D of the GST Act.

Taxation Administration Act 1953

58 Subsection 8AAB(5) (before table item 1A)

Insert:

1AA | 162‑100 | A New Tax System (Goods and Services Tax) Act 1999 |

59 Subsection 22(1)

After “net amount”, insert “, or any part of your net amount,”.

60 Subsection 62(2) (after table item 37A)

Insert:

37B | disallowing an election to pay GST by instalments | subsection 162‑15(2) |

37C | refusing a request to be allowed to make an election on a specified day | subsection 162‑25(3) |

61 Section 298‑5 in Schedule 1

Repeal the section, substitute:

This Division applies if:

(a) an administrative penalty is imposed on an entity by another Division in this Part; or

(b) a penalty is imposed on an entity by Subdivision 162‑C of the *GST Act.

62 Application

(1) The amendments made by this Part of this Schedule (other than the amendments made by items 56 and 57) apply, and are taken to have applied, in relation to net amounts for tax periods starting, or that started, on or after 1 July 2000.

(2) The amendments made by items 56 and 57 apply to assessments for the 2000‑2001 income year and later income years.

Part 3—Substituted accounting periods

A New Tax System (Goods and Services Tax) Act 1999

63 Paragraph 27‑15(1)(c)

Omit “law; or”, substitute “law.”.

64 Paragraph 27‑15(1)(d)

Repeal the paragraph.

65 Subsection 27‑15(2A)

Repeal the subsection.

66 Application

(1) The amendments made by this Part of this Schedule apply in relation to tax periods starting on or after 1 July 2001.

(2) Any determination made under section 27‑15 of the A New Tax System (Goods and Services Tax) Act 1999 that:

(a) is in force immediately before 1 July 2001; and

(b) could not have been made on any ground other than the ground referred to in paragraph 27‑15(1)(d) of that Act;

is taken, on and after 1 July 2001, to have been revoked with effect from the start of that day.

A New Tax System (Goods and Services Tax) Act 1999

67 After section 17‑15

Insert:

17‑20 Determinations relating to how to work out net amounts

(1) The Commissioner may make a determination that, in the circumstances specified in the determination, a *net amount for a tax period may be worked out to take account of other matters in the way specified in the determination.

(2) The matters must relate to correction of errors made in working out *net amounts for the immediately preceding tax period.

(3) If those circumstances apply in relation to a tax period applying to you, you may work out your *net amount for the tax period in that way.

68 Application

The amendment made by this Part of this Schedule applies, and is taken to have applied, in relation to net amounts for tax periods starting, or that started, on or after 1 July 2000.

Part 5—Phasing in input tax credits for motor vehicles etc.

A New Tax System (Goods and Services Tax Transition) Act 1999

69 At the end of subsection 6(2)

Add:

Note: Subsection 20(8) provides a rule stating when motor vehicles and other goods covered by subsection 20(1) are taken to be removed.

70 Subsection 20(2)

Omit “1 July 2001”, substitute “23 May 2001”.

71 Subsection 20(3)

Repeal the subsection.

72 Paragraph 20(3A)(c)

Omit “, (3)”.

73 Subsection 20(4B)

Omit “Neither subsection (2) nor subsection (3) applies if you make the acquisition or importation before 1 July 2002”, substitute “Subsection (2) does not apply if you make the acquisition or importation before 23 May 2001”.

74 Subsection 20(4B) (definition of original input tax credit)

Repeal the definition, substitute:

original input tax credit is the amount that would (but for this section) be the amount of the input tax credit on the acquisition or importation.

75 Subsection 20(4C)

Omit “1 July 2002”, substitute “23 May 2001”.

76 Subsection 20(6)

Repeal the subsection.

77 At the end of section 20

Add:

(8) For the purposes of applying subsection 6(2) to determine when an acquisition to which this section applies is made, the goods in question are not taken to be removed until the goods are physically removed:

(a) by the entity acquiring the goods; or

(b) if the entity acquires the goods for supply by way of lease—by that entity or the lessee of the goods.

(9) Subsection (8) does not by implication affect the application of subsection 6(2) to acquisitions to which this section does not apply.

(10) For the purposes of this section, an importation takes place when it becomes a taxable importation.

78 Application

The amendments made by this Part of this Schedule apply in relation to acquisitions and importations made on or after 23 May 2001.

Schedule 2—Pay as you go instalments

Part 1—Paying instalments using GDP‑adjusted notional tax

Taxation Administration Act 1953

1 Section 45‑1 in Schedule 1

Repeal the section, substitute:

45‑1 What this Division is about

If you have business or investment income, you must pay instalments towards your income tax liability. However, you do not have to do so unless the Commissioner has given you an instalment rate. Generally, instalments are payable for each quarter of your income year.

Your instalments may be based on your previous year’s income tax liability and notified to you by the Commissioner, or on your estimate of your income tax liability for the current income year. (In this case, you are a quarterly payer who pays on the basis of GDP adjusted notional tax). Generally, four quarterly instalments are payable annually on this basis, but you may only be required to pay two.

If you are not eligible to pay instalments on that basis, or if you are so eligible but choose not to do so, you must work out the amount of your quarterly instalment by multiplying your instalment income for an instalment quarter by the rate the Commissioner gave you, or by a rate you choose yourself. (In this case, you are a quarterly payer who pays on the basis of instalment income).

If you are not registered for GST purposes, you may be able to choose to pay an annual instalment after the end of the income year. (In this case, you are an annual payer).

The amount of annual instalment can be your instalment income for the income year multiplied by the rate the Commissioner gave you, or an amount based on your previous year’s income tax liability and notified to you by the Commissioner, or your own estimate of your income tax liability for the income year.

2 Subsection 45‑5(2) in Schedule 1

Omit “quarter. (There are limited exceptions to this).”, substitute “quarter if you are required or choose to work out your instalment on this basis. However, you may be able to pay an amount notified by the Commissioner. (There are exceptions to this).”.

3 Subsection 45‑5(5) in Schedule 1

Omit “The”, substitute “If you are a *quarterly payer who pays on the basis of instalment income, the”.

4 Section 45‑20 in Schedule 1 (heading)

Repeal the heading, substitute:

45‑20 Information to be given to the Commissioner by certain payers

5 Sections 45‑50 and 45‑55 in Schedule 1

Repeal the sections, substitute:

45‑50 Liability to pay instalments

(1) Subject to subsection (4), you are liable to pay an instalment for an *instalment quarter in an income year if, at the end of that instalment quarter, you are:

(a) a *quarterly payer who pays 4 instalments annually on the basis of GDP‑adjusted notional tax; or

(b) a *quarterly payer who pays on the basis of instalment income.

(2) Subject to subsection (4), you are liable to pay an instalment for an *instalment quarter that is the third or fourth instalment quarter in an income year if, at the end of that quarter, you are a *quarterly payer who pays 2 instalments annually on the basis of GDP‑adjusted notional tax.

(3) Subject to subsection (4), you are liable to pay an instalment for an income year if, at the end of the *starting instalment quarter in that year, you are an *annual payer.

Note: You may be liable to pay both an instalment for an income year and instalments for instalment quarters in that income year. See section 45‑150.

(4) You are only liable to pay an instalment for an *instalment quarter or an income year if:

(a) the Commissioner has given you an instalment rate; and

(b) the Commissioner has not withdrawn your instalment rate before the end of that quarter or year.

6 Section 45‑60 in Schedule 1

Repeal the section, substitute:

45‑60 Meaning of instalment quarter

For an income year (whether it ends on 30 June or not), the following are the instalment quarters:

(a) your first instalment quarter consists of the first 3 months of the income year; and

(b) your second instalment quarter consists of the fourth, fifth and sixth months of the income year; and

(c) your third instalment quarter consists of the seventh, eighth and ninth months of the income year; and

(d) your fourth instalment quarter consists of the tenth, 11th and 12th months of the income year.

45‑61 When quarterly instalments are due—payers of quarterly instalments

You are not a deferred BAS payer

(1) Subject to subsection (2), if you are:

(a) a *quarterly payer who pays on the basis of instalment income; or

(b) a *quarterly payer who pays 4 instalments annually on the basis of GDP‑adjusted notional tax; or

(c) a *quarterly payer who pays 2 instalments annually on the basis of GDP‑adjusted notional tax;

the instalment for an *instalment quarter that you are liable to pay is due on or before the 21st day of the month after the end of that quarter.

Note: You are only liable to pay instalments for the third and fourth instalment quarters in an income year if you are a quarterly payer who pays 2 instalments annually on the basis of GDP‑adjusted notional tax. See section 45‑50.

You are a deferred BAS payer

(2) If:

(a) subsection (1) would, but for this subsection, have applied to you in relation to an *instalment quarter; but

(b) you are a *deferred BAS payer on the 21st day of the month after the end of that quarter;

the instalment for that quarter is instead due on or before:

(c) the 28th day of the month after the end of that quarter unless all or a part of a December falls within the last month of that quarter; or

(d) if all or a part of a December falls within the last month of that quarter—the next 28 February.

Note: You are only liable to pay instalments for the third and fourth instalment quarters in an income year if you are a quarterly payer who pays 2 instalments annually on the basis of GDP‑adjusted notional tax. See section 45‑50.

7 Section 45‑65 in Schedule 1

Repeal the section.

8 Subsection 45‑90(1) in Schedule 1 (note)

Omit all the words after “If the Commissioner does so,”, substitute “you cease to be liable to pay instalments (even if you have chosen a rate under section 45‑205). See subsection 45‑50(4).”.

9 Subsection 45‑90(2) in Schedule 1

Omit all the words from and including “another one”, substitute:

another one:

(a) you are again liable to pay instalments in accordance with section 45‑50; and

(b) this Division has effect as if the Commissioner has given you an instalment rate for the first time.

10 Subsection 45‑110(1) in Schedule 1

After “follows”, insert “if, at the end of that instalment quarter, you are a *quarterly payer who pays on the basis of instalment income”.

11 Section 45‑110 in Schedule 1 (heading)

Repeal the heading, substitute:

45‑110 How to work out amount of quarterly instalment on instalment income basis

12 Subsection 45‑112(1) in Schedule 1

After “*quarterly payer who pays on the basis of GDP‑adjusted notional tax”, insert “who is liable to pay an instalment for that quarter”.

13 Subdivision 45‑D in Schedule 1 (heading)

Repeal the heading, substitute:

Subdivision 45‑D—Quarterly payers

14 Sections 45‑125 and 45‑130 in Schedule 1

Repeal the sections, substitute:

45‑125 Quarterly payer who pays instalments on the basis of instalment income

(1) You are a quarterly payer who pays on the basis of instalment income if:

(a) at the end of the *starting instalment quarter in an income year, you are not a *quarterly payer who pays on the basis of GDP‑adjusted notional tax and you are not an *annual payer; or

(b) but for this section, you would be a quarterly payer who pays on the basis of GDP‑adjusted notional tax at the end of the starting instalment quarter in an income year but you choose to pay quarterly instalments on the basis of your instalment income.

Note: The entity must make the choice mentioned in paragraph (b) in accordance with subsection (4).

(2) The starting instalment quarter in an income year (the current year) is:

(a) if the Commissioner gives you an instalment rate for the first time during an *instalment quarter in the current year—that instalment quarter (even if it is not the first instalment quarter in the current year); or

(b) if the Commissioner has given you an instalment rate during a previous income year and your instalment rate has not been withdrawn—the first instalment quarter in the current year; or

(c) if you become liable to pay an instalment for an instalment quarter in the current year because of subsection 45‑150(2)—that instalment quarter (even if it is not the first instalment quarter in the current year).

How and when you become such a payer

(3) You become a *quarterly payer who pays on the basis of instalment income just before the end of the *starting instalment quarter if paragraph (1)(a) or (b) is satisfied.

(4) You must make the choice mentioned in paragraph (1)(b) by notifying the Commissioner in the *approved form on or before the day on which the instalment for that quarter is due (disregarding subsection 45‑112(3)).

How and when you stop being such a payer

(5) If you are a *quarterly payer who pays on the basis of instalment income because of paragraph (1)(a), you stop being such a payer at the start of the first *instalment quarter in the next income year if, at the end of that quarter, you become:

(a) a *quarterly payer who pays on the basis of GDP‑adjusted notional tax; or

(b) an *annual payer.

(6) If you are a *quarterly payer who pays on the basis of instalment income because of paragraph (1)(b), you stop being such a payer at the start of the first *instalment quarter in the next income year if:

(a) you become an *annual payer at the end of that quarter; or

(b) both of the following conditions apply:

(i) you choose not to be a quarterly payer who pays on the basis of instalment income;

(ii) you become a *quarterly payer who pays on the basis of GDP‑adjusted notional tax at the end of that quarter.

(7) You may only make the choice mentioned in paragraph (6)(b) if you would otherwise satisfy paragraph 45‑130(1)(a), (b) or (c) at the end of that quarter. You must make that choice by notifying the Commissioner in the *approved form on or before the day on which the instalment for that quarter is due (disregarding subsection 45‑112(3)).

45‑130 Quarterly payer who pays on the basis of GDP‑adjusted notional tax

(1) You are a quarterly payer who pays on the basis of GDP‑adjusted notional tax if, at the end of the *starting instalment quarter in an income year:

(a) you are an individual who is not an *annual payer or a *quarterly payer who pays on the basis of instalment income; or

(b) you are a *full self‑assessment taxpayer:

(i) that is not an *annual payer or a *quarterly payer who pays on the basis of instalment income; and

(ii) your base assessment instalment income (within the meaning of section 45‑320) for the *base year is $1 million or less; or

(c) you satisfy all of the following conditions:

(i) you are a *full self‑assessment taxpayer whose base assessment instalment income (within the meaning of section 45‑320) for the *base year is more than $1 million;

(ii) you are not an annual payer, but you satisfy the conditions set out in subsection 45‑140(1) for an annual payer;

(iii) you are not a quarterly payer who pays on the basis of instalment income.

Note: Paragraph (a) may apply to you if you are a multi‑rate trustee. See section 45‑468.

How and when you become such a payer

(2) You become such a payer just before the end of the *starting instalment quarter if paragraph (1)(a), (b) or (c) is satisfied.

How and when you stop being such a payer

(3) You stop being a *quarterly payer who pays on the basis of GDP‑adjusted notional tax at the start of the first *instalment quarter in the next income year if you fail to satisfy paragraph (1)(a), (b) or (c) at the end of that quarter.

(4) In addition, you stop being such a payer at the start of the first *instalment quarter in the next income year if, at the end of that quarter, you become:

(a) a *quarterly payer who pays on the basis of instalment income; or

(b) an *annual payer.

45‑132 Quarterly payer who pays 4 instalments annually on the basis of GDP‑adjusted notional tax

(1) You are a quarterly payer who pays 4 instalments annually on the basis of GDP‑adjusted notional tax if, at the end of the *starting instalment quarter in an income year:

(a) you satisfy the conditions to be a *quarterly payer who pays on the basis of GDP‑adjusted notional tax under section 45‑130; and

(b) you do not satisfy the conditions to be a *quarterly payer who pays 2 instalments annually on the basis of GDP‑adjusted notional tax under section 45‑134.

How and when you become such a payer

(2) You become such a payer just before the end of the *starting instalment quarter if paragraphs (1)(a) and (b) are satisfied.

How and when you stop being such a payer

(3) You stop being a *quarterly payer who pays 4 instalments annually on the basis of GDP‑adjusted notional tax at the start of the first *instalment quarter in the next income year if you fail to satisfy paragraphs (1)(a) and (b) at the end of that quarter.

(4) In addition, you stop being such a payer at the start of the first *instalment quarter in the next income year if, at the end of that quarter, you become:

(a) a *quarterly payer who pays on the basis of instalment income; or

(b) an *annual payer.

45‑134 Quarterly payer who pays 2 instalments annually on the basis of GDP‑adjusted notional tax

(1) You are a quarterly payer who pays 2 instalments annually on the basis of GDP‑adjusted notional tax if, at the end of the *starting instalment quarter in an income year, you are an individual that is a *quarterly payer who pays on the basis of GDP‑adjusted notional tax and one or more of the following paragraphs apply:

(a) both of the following conditions are satisfied:

(i) you are carrying on a *primary production business in the income year;

(ii) the assessable income that was *derived from, or resulted from, a primary production business that you carried on in the *base year exceeded the amount of so much of your deductions in that year that are reasonably related to that income;

(b) both of the following conditions are satisfied:

(i) you are a *special professional in the income year;

(ii) your *assessable professional income in the base year exceeded the amount of so much of your deductions in that year that are reasonably related to that income.

Note: This section may apply to you if you are a multi‑rate trustee. See section 45‑468.

How and when you become such a payer

(2) You become such a payer just before the end of the *starting instalment quarter if subsection (1) is satisfied.

How and when you stop being such a payer

(3) You stop being a *quarterly payer who pays 2 instalments annually on the basis of GDP‑adjusted notional tax at the start of the first *instalment quarter in the next income year if you fail to satisfy subsection (1) at the end of that quarter.

(4) In addition, you also stop being such a payer at the start of the first *instalment quarter in the next income year if, at the end of that quarter, you become:

(a) a *quarterly payer who pays on the basis of instalment income; or

(b) an *annual payer.

15 Subsection 45‑140(1) in Schedule 1

Omit “first *instalment quarter in an income year for which you would otherwise be liable to pay a quarterly instalment”, substitute “*starting instalment quarter”.

16 Subsection 45‑140(3) in Schedule 1

Repeal the subsection, substitute:

(3) You become an annual payer just before the end of the *starting instalment quarter if:

(a) you satisfy the conditions in subsection (1); and

(b) you choose to pay instalment annually.

17 Subsection 45‑150(2) in Schedule 1

Repeal the subsection, substitute;

(2) You must pay an instalment for that or a later *instalment quarter if subsection 45‑50(1) or (2) requires you to do so.

18 Subsection 45‑155(1) in Schedule 1

Repeal the subsection, substitute:

(1) You stop being an *annual payer at the start of the first *instalment quarter in an income year (the current year) if:

(a) after the end of the first instalment quarter in the previous income year and before the end of the first instalment quarter in the current year, the Commissioner notifies you of your *notional tax, and it is $8,000 or more; or

(b) you choose to pay instalments quarterly instead of annually.

19 After subsection 45‑155(1) in Schedule 1

Insert:

(1A) You must make the choice by notifying the Commissioner, in the *approved form, on or before the day on which the instalment for the first *instalment quarter for the current year would otherwise be due (disregarding subsection 45‑112(3)).

20 Subsection 45‑155(3) in Schedule 1

Omit “the income year”, substitute “the previous income year”.

21 Subsection 45‑155(4) in Schedule 1

Repeal the subsection, substitute:

(4) You may again become an *annual payer at the end of the first *instalment quarter in a later income year if:

(a) at that time, you again satisfy the conditions in section 45‑140; and

(b) you again choose under that section to pay annually.

22 Subsection 45‑180(2) in Schedule 1

Repeal the subsection, substitute:

(2) You must pay an instalment for the first *instalment quarter in the next income year and instalments for later instalment quarters if subsection 45‑50(1) or (2) requires you to do so.

23 Subdivision 45‑F in Schedule 1 (heading)

Repeal the heading, substitute:

24 Section 45‑200 in Schedule 1

Omit “*quarterly payer”, substitute “*quarterly payer who pays on the basis of instalment income at the end of an *instalment quarter”.

25 Paragraph 45‑215(1)(b) in Schedule 1

Repeal the paragraph, substitute:

(b) that rate is lower than the instalment rate you used to work out the amount of your instalment for the previous instalment quarter (if any) in the same income year; and

26 Section 45‑400 in Schedule 1

Omit all the words before the table, substitute:

(1) This section applies if you are a *quarterly payer who pays 4 instalments annually on the basis of GDP‑adjusted notional tax at the end of an *instalment quarter in an income year (the current year).

(2) The amount of your instalment for that *instalment quarter which the Commissioner must work out and notify to you under paragraph 45‑112(1)(a) is:

(a) the amount worked out in accordance with the table if it is positive; or

(b) otherwise—nil.

27 Section 45‑400 in Schedule 1 (heading)

Repeal the heading, substitute:

45‑400 Working out amount of instalment—payers of 4 quarterly instalments

28 At the end of section 45‑400 in Schedule 1

Add:

Note: Your instalments for earlier instalment quarters may have been worked out on a basis other than GDP‑adjusted notional tax.

29 After section 45‑400 in Schedule 1

Insert:

45‑402 Working out amount of instalment—payers of 2 quarterly instalments

(1) This section applies if you are a *quarterly payer who pays 2 instalments annually on the basis of GDP‑adjusted notional tax at the end of an *instalment quarter in an income year.

(2) If you are liable to pay an instalment for that *instalment quarter, the amount of that instalment which the Commissioner must work out and notify to you under paragraph 45‑112(1)(a) is:

(a) the amount worked out in accordance with this section if it is positive; or

(b) otherwise—nil.

Amount of instalment

(3) Subject to subsections (4) to (6), the amount of that instalment is worked out in accordance with the following table:

Amount of quarterly instalment | ||

Item | If the *instalment quarter is: | the amount of the instalment is: |

1 | the third *instalment quarter in the income year | 75% of your *GDP‑adjusted notional tax |

2 | the fourth *instalment quarter in the income year | 100% of your *GDP‑adjusted notional tax, reduced by your instalment for earlier instalment quarter in that income year |

You receive instalment rate for the first time in second quarter

(4) If the Commissioner gives you an instalment rate for the first time during the second *instalment quarter in that income year, the amount of the instalment is worked out in accordance with the following table:

Amount of quarterly instalment | ||

Item | If the *instalment quarter is: | the amount of the instalment is: |

1 | the third *instalment quarter in the income year | 50% of your *GDP‑adjusted notional tax |

2 | the fourth *instalment quarter in the income year | 75% of your *GDP‑adjusted notional tax, reduced by your instalment for the earlier instalment quarter in that income year |

You receive instalment rate for the first time in third quarter

(5) If the Commissioner first gives you an instalment rate during the third *instalment quarter in that income year, the amount of the instalment is worked out in accordance with the following table:

Amount of quarterly instalment | ||

Item | If the *instalment quarter is: | the amount of the instalment is: |

1 | the third *instalment quarter in the income year | 25% of your *GDP‑adjusted notional tax |

2 | the fourth *instalment quarter in the income year | 50% of your *GDP‑adjusted notional tax, reduced by your instalment for the earlier instalment quarter in that income year |

You receive instalment rate for the first time in fourth quarter

(6) If the Commissioner first gives you an instalment rate during the fourth *instalment quarter in that income year, the amount of the instalment must be equal to 25% of your *GDP‑adjusted notional tax.

30 Subsection 45‑405(1) in Schedule 1

After “45‑400”, insert “or 45‑402 (as appropriate)”.

31 Before subsection 45‑410(1) in Schedule 1

Insert:

(1A) This section applies if you are a *quarterly payer who pays 4 instalments annually on the basis of GDP‑adjusted notional tax at the end of an *instalment quarter in an income year (the current year).

32 Section 45‑410 in Schedule 1 (heading)

Repeal the heading, substitute:

45‑410 Working out amount of instalment—payers of 4 quarterly instalments

33 Subsection 45‑410(1) in Schedule 1

Omit “an *instalment”, substitute “that *instalment”.

34 After section 45‑410 in Schedule 1

Insert:

45‑412 Working out amount of instalment—payers of 2 quarterly instalments

(1) This section applies if you are a *quarterly payer who pays 2 instalments annually on the basis of GDP‑adjusted notional tax at the end of an *instalment quarter in an income year.

(2) If you are liable to pay an instalment for that quarter, the amount of that instalment for the purposes of paragraph 45‑112(1)(b) or (c) is:

(a) the amount worked out, in accordance with this section, on the basis of the estimate of your *benchmark tax for that income year that section 45‑415 requires to be used, if that amount is positive; or

(b) otherwise—nil.

Note: If the amount is negative, you can claim a credit under section 45‑420.

Instalment for third quarter

(3) Subject to subsections (5) to (9), the amount of the instalment for the third *instalment quarter in that year is 75% of the estimate of your *benchmark tax.

Instalment for fourth quarter

(4) Subject to subsections (5) to (9), the amount of the instalment for the fourth *instalment quarter in that year is worked out by subtracting:

(a) the amount of your instalment for the earlier instalment quarter in that year;

from:

(b) the estimate of your *benchmark tax.

You receive instalment rate for the first time in second quarter

(5) If the Commissioner gives you an instalment rate for the first time during the second *instalment quarter in the income year, the amount of the instalment for the third *instalment quarter in that year is 50% of the estimate of your *benchmark tax.

(6) If the Commissioner gives you an instalment rate for the first time during the second *instalment quarter in the income year, the amount of the instalment for the fourth instalment quarter in that year is worked out by subtracting:

(a) the amount of your instalment for the earlier instalment quarter in that year;

from:

(b) 75% of the estimate of your *benchmark tax.

You receive instalment rate for the first time in third quarter

(7) If the Commissioner gives you an instalment rate for the first time during the third *instalment quarter in the income year, the amount of the instalment for the third instalment quarter in that year is 25% of the estimate of your *benchmark tax.

(8) If the Commissioner gives you an instalment rate for the first time during the third *instalment quarter in the income year, the amount of the instalment for the fourth instalment quarter in that year is worked out by subtracting:

(a) the amount of your instalment for the earlier instalment quarter in that year;

from:

(b) 50% of the estimate of your *benchmark tax.

You receive instalment rate for the first time in fourth quarter

(9) If the Commissioner gives you an instalment rate for the first time during the fourth *instalment quarter in the income year, the amount of the instalment for that quarter is 25% of the estimate of your *benchmark tax.

35 Subsection 45‑420(1) in Schedule 1

After “45‑410”, insert “or 45‑412 (as appropriate)”.

36 Section 45‑468 in Schedule 1

Omit “who pays on the basis of GDP‑adjusted notional tax”.

37 Section 45‑468 in Schedule 1 (heading)

Repeal the heading, substitute: