2C

Schedule 1—Amendment of the A New Tax System (Family Assistance) Act 1999

Part 1—Amendments relating to family tax benefit and maternity immunisation allowance

1 Paragraph 21(1)(b)

Repeal the paragraph, substitute:

(b) the individual:

(i) is an Australian resident; or

(ii) meets the requirements set out in subparagraph 729(2)(f)(ii), (iii), (iv) or (v) of the Social Security Act 1991 and is in Australia; and

2 Subsection 22(3) (second sentence)

Repeal the sentence.

3 Subsections 22(7) and (8)

Repeal the subsections, substitute:

(7) If:

(a) the Secretary is satisfied there has been, or will be, a pattern of care for an individual (the child) over a period such that, for the whole, or for parts (including different parts), of the period, the child was, or will be, an FTB child of more than one other individual under subsection (2), (3), (4), (5) or (6); and

(b) one of those other individuals makes, or has made, a claim under Part 3 of the A New Tax System (Family Assistance) (Administration) Act 1999 for payment of family tax benefit in respect of the child for some or all of the days in that period; and

(c) subsection 25(1) does not require that the child be taken not to be an FTB child of that individual for any part of that period;

the child is to be taken to be an FTB child of that individual for the purposes of this section on each day in that period, whether or not the child was in that individual’s care on that day.

4 After section 22

Insert:

22A Exceptions to the operation of section 22

Exceptions

(1) Despite section 22, an individual cannot be an FTB child of another individual (an adult) in the cases set out in this table:

When the individual is not an FTB child of the adult at a particular time |

| If the individual is aged: | then the individual cannot be an FTB child of the adult if: |

1 | 5 or more and less than 16 | (a) the individual is not undertaking full‑time study and the individual has adjusted taxable income, for the income year in which the particular time occurs, that equals or exceeds the cut‑out amount (see subsection (2)); or (b) the adult is the individual’s partner. |

2 | 16 or more | (a) the individual has adjusted taxable income, for the income year in which the particular time occurs, that equals or exceeds the cut‑out amount (see subsection (2)); or (b) the adult is the individual’s partner; or (c) the individual, or someone on behalf of the individual, is, at the particular time, receiving payments under a prescribed educational scheme. |

3 | any age | the individual, or someone on behalf of the individual, is, at the particular time, receiving: (a) a social security pension; or (b) a social security benefit; or (c) payments under a program included in the programs known as Labour Market Programs. |

Definition

(2) In subsection (1):

cut‑out amount means the sum of:

(a) the amount specified in column 2 of item 2 of the table in clause 30 of Schedule 1 divided by 0.3; and

(b) the amount specified in clause 33 of that Schedule.

5 Subsections 23(1) and (2)

After “22(2) or (3)” (wherever occurring), insert “(including that subsection in its application by virtue of subsection 22(7))”.

6 Subsection 23(3)

Repeal the subsection.

7 Subsection 23(4)

Omit “or (3)”.

8 Section 25

Repeal the section, substitute:

25 Effect of FTB child being in individual’s care for less then 10% of a period

(1) If:

(a) the Secretary is satisfied there has been, or will be, a pattern of care for an individual (the child) over a period such that, for the whole, or for parts (including different parts), of the period, the child was, or will be, an FTB child of more than one other individual in accordance with subsection 22(2), (3), (4), (5) or (6); and

(b) one of those other individuals makes, or has made, a claim under Part 3 of the A New Tax System (Family Assistance) (Administration) Act 1999 for payment of family tax benefit in respect of the child for some or all of the days in that period; and

(c) the Secretary is satisfied that the child was, or will be, in the care of that last‑mentioned individual for less than 10% of that period;

the child is to be taken, despite that subsection, not to be an FTB child of that last‑mentioned individual for any part of that period.

(2) For the purposes of this section, a child cannot be in the care of more than one of the other individuals referred to in subsection (1) on any particular day.

(3) For the purposes of this section, the Secretary must determine which of the other individuals referred to in subsection (1) has the care of the child on any given day having regard to the living arrangements of the child.

9 Paragraph 28(1)(e)

Omit “, such that each of those percentages is a multiple of 5%”.

10 Paragraph 29(e)

Omit “, such that each of those percentages is a multiple of 5%”.

11 Section 30

Repeal the section.

12 Paragraph 33(2)(c)

Omit “the subject amount”, substitute “so much of the subject amount as does not relate to any period before the beginning of the income year preceding the income year in which the individual died”.

13 Paragraph 33(2)(d)

Omit “the subject amount”, substitute “that much of the subject amount”.

14 Subsection 33(2)

Omit “the subject amount and no‑one else is, or can become, eligible for or entitled to be paid that amount”, substitute “that much of the subject amount and no‑one else is, or can become, eligible for or entitled to be paid any of the subject amount”.

15 Subsection 35(1) (table items 2 and 3)

Repeal the items, substitute:

2 | 16 or more | (a) the individual has adjusted taxable income, for the income year in which the particular time occurs, that equals or exceeds the cut‑out amount (see subsection (3)); or (b) the individual, or someone on behalf of the individual, is, at the particular time, receiving payments under a prescribed educational scheme. |

3 | any age | the individual, or someone on behalf of the individual, is, at the particular time, receiving: (a) a social security pension; or (b) a social security benefit; or (c) payments under a program included in the programs known as Labour Market Programs. |

16 Subparagraph 39(2)(b)(v)

Repeal the subparagraph.

17 Paragraph 39(4)(c)

Repeal the paragraph.

18 Paragraphs 59(1)(b) and (c)

Repeal the paragraphs, substitute:

(b) the FTB child is also an FTB child of another individual who is not person A’s partner;

19 Subsection 59(1) (second sentence)

Repeal the sentence.

20 Section 68

Repeal the section, substitute:

68 When the maternity immunisation allowance is shared

If:

(a) apart from this section, more than one individual is eligible for maternity immunisation allowance under subsection 39(2) or (4) in respect of the same child; and

(b) the Secretary, under subsection 59(1), has determined each individual’s percentage of family tax benefit for the child;

each individual is eligible instead only for a percentage of the allowance equal to the percentage of family tax benefit that the Secretary determined in relation to the individual.

21 Clause 3 of Schedule 1

Omit “Subject to clauses 5 and 6”, substitute “Subject to the operation of clause 5”.

22 Clause 5 of Schedule 1

Omit “If”, substitute “Subject to subclause (2), if”.

23 At the end of clause 5 of Schedule 1

Add:

(2) If, at any time, the FTB advance rate in respect of an individual would equal or exceed the individual’s Part A rate were subclause (1) to be disregarded, then, with effect from that time, subclause (1) ceases to have effect.

24 Clause 6 of Schedule 1

Repeal the clause.

25 Paragraph 13(1)(b) of Schedule 1

Repeal the paragraph, substitute:

(b) the individual’s claim for family tax benefit is not a claim to which subclause (2) applies; and

(ba) neither the individual nor the individual’s partner is receiving payments of incentive allowance under clause 36 of Schedule 1A to the Social Security Act 1991; and

26 Paragraph 13(1)(f) of Schedule 1

Repeal the paragraph, substitute:

(f) if the individual is not a relevant shared carer—the rent is payable at a rate of more than:

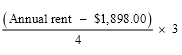

(i) if the individual is not a member of a couple—$2,485.65 per year; or

(ii) if the individual is a member of a couple but is not partnered (partner in gaol) or a member of an illness separated couple, a respite care couple or a temporarily separated couple—$3,675.55 per year; or

(iii) if the individual is partnered (partner in gaol) or is a member of an illness separated couple or a respite care couple—$2,485.65 per year; or

(iv) if the individual is a member of a temporarily separated couple—$2,485.65 per year; and

(fa) if the individual is a relevant shared carer—the rent is payable at a rate of more than:

(i) if the individual is not a member of a couple—$1,898.00 per year; or

(ii) if the individual is a member of a couple but is not partnered (partner in gaol) or a member of an illness separated couple, a respite care couple or a temporarily separated couple—$3,087.90 per year; or

(iii) if the individual is partnered (partner in gaol) or is a member of an illness separated couple or a respite care couple—$1,898.00 per year; or

(iv) if the individual is a member of a temporarily separated couple—$1,898.00 per year; and

27 Subclauses 13(2), (3) and (4) of Schedule 1

Repeal the subclauses, substitute:

(2) This subclause applies to an individual’s claim for family tax benefit if:

(a) the claim is for family tax benefit for a past period that occurs in the income year before the one in which the claim is made; and

(b) when the claim is made the individual:

(i) is eligible for family tax benefit; and

(ii) is not prevented by section 9 of the A New Tax System (Family Assistance) (Administration) Act 1999 from making an effective claim for payment of family tax benefit by instalment; and

(c) the claim is not accompanied by a claim for family tax benefit by instalment.

28 Clause 14 of Schedule 1

After “The rate of rent assistance”, insert “payable to an individual who is not a relevant shared carer”.

29 Clause 14 of Schedule 1 (table)

Repeal the table, substitute:

Rent assistance payable to individual who is not a relevant shared carer (Part A—Method 1) |

| Column 1 Family situation | Column 2 Rate A | Column 3 Rate B |

| | | Column 3A | Column 3B |

| | | 1 or 2 rent assistance children | 3 or more rent assistance children |

1 | Not member of a couple |

| $2,310.45 | $2,606.10 |

2 | Member of a couple other than a person who is partnered (partner in gaol) or a member of an illness separated couple, a respite care couple or a temporarily separated couple |

| $2,310.45 | $2,606.10 |

3 | Person who is partnered (partner in gaol) or a member of an illness separated couple or a respite care couple |

| $2,310.45 | $2,606.10 |

4 | Member of a temporarily separated couple |

| $2,310.45 | $2,606.10 |

Note: The heading to clause 14 of Schedule 1 is replaced by the heading “Rate of rent assistance payable to individual who is not a relevant shared carer”.

30 After clause 14 of Schedule 1

Insert:

14A Rate of rent assistance payable to individual who is a relevant shared carer

The rate of rent assistance payable to an individual who is a relevant shared carer is the higher of:

(a) the rate of rent assistance that would be payable to that individual if that individual were not a relevant shared carer; and

(b) the rate of rent assistance worked out using the following table.

In working out rent assistance, work out the individual’s family situation using column 1 and calculate Rate A for the individual using the corresponding formula in column 2. This will be the individual’s rate of rent assistance in accordance with the table but only up to Rate B specified in column 3.

Rent assistance payable to individual who is a relevant shared carer (Part A—Method 1) |

| Column 1 Family situation | Column 2 Rate A | Column 3 Rate B |

1 | Not member of a couple |

| $1,981.95 |

2 | Member of a couple other than a person who is partnered (partner in gaol) or a member of an illness separated couple, a respite care couple or a temporarily separated couple |

| $1,865.15 |

3 | Person who is partnered (partner in gaol) or a member of an illness separated couple or a respite care couple |

| $1,981.95 |

4 | Member of a temporarily separated couple |

| $1,865.15 |

31 After clause 16 of Schedule 1

Insert:

16A Rent paid by a member of an illness separated, respite care or temporarily separated couple

If an individual is a member of an illness separated, respite care or temporarily separated couple, any rent that the individual’s partner pays or is liable to pay in respect of the premises occupied by the individual is to be treated as paid or payable by the individual.

32 Clause 17 of Schedule 1

After “or a service pension”, insert “or is receiving income support supplement under Part IIIA of the Veterans’ Entitlements Act 1986”.

33 Before clause 20 of Schedule 1

Insert:

19A Extended meaning of receiving maintenance income

In this Division, if the FTB child of an individual receives maintenance income, the individual is taken to have received the maintenance income.

19B Application of maintenance income test to certain pension and benefit recipients and their partners

If the individual, or the individual’s partner, is:

(a) permanently blind; and

(b) receiving:

(i) an age pension (under Part 2.2 of the Social Security Act 1991); or

(ii) a disability support pension (under Part 2.3 of the Social Security Act 1991); or

(iii) a service pension; or

(iv) income support supplement (under Part IIIA of the Veterans’ Entitlements Act 1986);

then:

(c) the individual’s maintenance income excess is nil; and

(d) the individual’s income and maintenance tested rate is the same as the individual’s income tested rate.

34 Clause 20 of Schedule 1

Omit “work out an individual’s reduction for maintenance income:”, substitute “work out an individual’s reduction for maintenance income if clause 19B does not apply:”.

35 Clause 20 of Schedule 1 (method statement, step 1)

Omit “annual rate”, substitute “annualised amount”.

36 After clause 20 of Schedule 1

Insert:

20A Annualised amount of maintenance income

Object of clause

(1) The object of this clause is to annualise the maintenance income (other than capitalised maintenance income) (CMI) of an individual during an income year.

Annualisation of maintenance income other than CMI

(2) If an individual receives maintenance income (other than CMI) from another individual during any period or periods (the relevant period or periods) in an income year, the annualised amount of the maintenance income of the individual is worked out using the following formula:

Commencement of relevant period

(3) If:

(a) an individual (payee) receives maintenance income (other than CMI) from another individual (payer) in an income year under a maintenance liability; and

(b) subsection (4) does not apply;

the relevant period in respect of the maintenance income commences:

(c) in the case where the maintenance liability arises after 1 July of the income year in which the maintenance income is received—on the day that the maintenance liability arises; or

(d) in the case where the maintenance liability exists on 1 July of the income year in which the maintenance income is received—1 July.

(4) If:

(a) a payee receives maintenance income (other than CMI) from a payer in an income year under a maintenance liability; and

(b) the payee has received maintenance income (other than CMI) from that payer previously during a period in the income year, but not under a maintenance liability; and

(c) in between the time the payee receives maintenance income under paragraph (a) and the end of the period referred to in paragraph (b):

(i) the payee and the payer were not members of the same couple; and

(ii) the payee was entitled to claim, or apply for, maintenance from the payer;

the relevant period in respect of the maintenance income commences:

(d) on the day the payee first received the previously received maintenance income in the income year; or

(e) on such earlier day in respect of the previously received maintenance income that the Secretary determines.

(5) If a payee receives maintenance income (other than CMI) from a payer during a period in an income year but not under a maintenance liability, the relevant period, in respect of the maintenance income, commences:

(a) on the day that the payee first received the maintenance income during that period; or

(b) on such earlier day that the Secretary determines.

End of relevant period

(6) A relevant period, in respect of maintenance income (other than CMI) received under a maintenance liability in an income year, ends either when the maintenance liability ceases (if it ceases before the end of the income year) or on 30 June of the income year.

(7) If:

(a) a payee receives maintenance income (other than CMI) in an income year; and

(b) the maintenance income is not received under a maintenance liability;

the relevant period ends in respect of the payee either:

(c) unless subclause (8) applies—when the payee ceases to receive the maintenance income (if the payee ceases to receive the income before the end of the income year); or

(d) on 30 June of the income year.

(8) If:

(a) a payee receives maintenance income (other than CMI) from a payer in an income year under a maintenance liability; and

(b) the payee has received maintenance income (other than CMI) from that payer previously during a period in the income year, but not under a maintenance liability; and

(c) in between the time the payee receives maintenance income under paragraph (a) and the end of the period referred to in paragraph (b):

(i) the payee and the payer were not members of the same couple; and

(ii) the payee was entitled to claim, or apply for, maintenance from the payer;

the relevant period ends either when the maintenance liability ceases (if it ceases before the end of the income year) or on 30 June of the income year.

Relevant period where payee elects to end an assessment

(9) If:

(a) a payee receives maintenance income (other than CMI) in an income year from a payer under a maintenance liability which is an assessment under Part 5 of the Child Support (Assessment) Act 1989; and

(b) the payee and payer become members of the same couple; and

(c) the payee elects under the Child Support (Assessment) Act 1989 to end the assessment from a specified day before the day the payee and payer became members of the same couple;

for the purpose of determining the commencement or end of the relevant period, the assessment is taken to end from the day the payee and the payer became a member of the same couple or from such earlier day as the Secretary determines (not being a day earlier than the specified day).

Meaning of maintenance liability

(10) In this clause, maintenance liability means a liability to provide:

(a) child support; or

(b) maintenance (other than child support) that arises as a result of:

(i) the order of a court; or

(ii) a maintenance agreement registered in, or approved by, a court under the Family Law Act 1975 or the law of a State or Territory.

Day a maintenance liability arises

(11) The day a maintenance liability arises is:

(a) if the liability is to provide child support, the day that the liability arises under the Child Support (Assessment) Act 1989; or

(b) if the liability is to provide maintenance that arises as set out in paragraph (10)(b), the day that the order of the court or the maintenance agreement has effect from.

37 Clause 21 of Schedule 1

Repeal the clause, substitute:

21 Maintenance income of members of couple to be added

The annualised amount of the maintenance income of an individual who is a member of a couple is the sum of the amounts that, apart from this clause, would be the respective annualised amounts of each of the members of the couple.

38 After subclause 24(2) of Schedule 1

Insert:

(2A) For the capitalisation period in an income year, the annualised amount of an individual’s capitalised maintenance income is worked out using the following formula:

39 Clause 25 of Schedule 1

Omit “If”, substitute “Subject to the operation of clause 25A, if”.

40 Clause 25 of Schedule 1 (method statement, step 2)

Repeal the step, substitute:

Step 2. Apply the income test in Division 3 of this Part (clause 28) to work out any reduction for adjusted taxable income. Take any reduction away from the individual’s maximum rate: the result is the individual’s provisional Part A rate.

Step 3. The individual’s Part A rate is:

(a) the individual’s provisional Part A rate if that rate is equal to or greater than the rate that would be the individual’s income and maintenance tested rate under step 3 of the method statement in clause 3 if the individual’s Part A rate were to be calculated using Part 2; or

(b) the rate that would the individual’s income and maintenance tested rate as so calculated if it is greater than the individual’s provisional Part A rate.

41 After clause 25 of Schedule 1

Insert:

25A Family tax benefit advance to individual

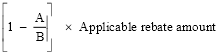

(1) Subject to subclause (2), if family tax benefit advance is paid to an individual, the individual’s Part A rate during the individual’s family tax benefit advance period is to be reduced by the FTB advance rate.

(2) If, at any time, the FTB advance rate in respect of an individual would equal or exceed the individual’s Part A rate were subclause (1) to be disregarded, then, with effect from that time, subclause (1) ceases to have effect.

(3) In subclause (2), the reference to the individual’s Part A rate includes a reference to a nil rate.

Part 2—Amendments relating to child care benefit

42 Subsection 3(1)

Before the definition of absence, insert:

24 hour care has the meaning given in subsection (5).

43 Subsection 3(1)

Before the definition of absence, insert:

24 hour care limit, in respect of a week and child, means a limit of:

(a) one or more 24 hour care periods during which 24 hour care is provided to the child, as certified by an approved child care service under subsection 56(3) or (4) or decided by the Secretary under subsection 56(6) or (8); and

(b) all of the hours in the sessions of care provided by an approved child care service to the child in the week, other than those hours that are included in a 24 hour care period.

44 Subsection 3(1)

Before the definition of absence, insert:

24 hour care period means a period of time that is at least 24 consecutive hours but less than 48 consecutive hours.

45 Subsection 3(1) (definition of absence)

Repeal the definition, substitute:

absence, in relation to care provided by an approved child care service, has a meaning affected by sections 10 and 10A.

46 Subsection 3(1)

Insert:

disabled person means a person who is:

(a) receiving a disability support pension under Part 2.3 of the Social Security Act 1991; or

(b) receiving an invalidity pension under Division 4 of Part III of the Veterans’ Entitlements Act 1986; or

(c) participating in an independent living program provided by CRS Australia or such other body determined by the Minister for the purposes of this paragraph; or

(d) diagnosed by a medical practitioner or a psychologist (see subsection 3(3)) as a person who is impaired to a degree that significantly incapacitates him or her; or

(e) included in a class of persons determined by the Minister to be a disabled person for the purposes of this paragraph.

47 Subsection 3(1)

Insert:

week, in relation to child care benefit, has the meaning given in subsection (6).

48 At the end of section 3

Add:

(3) For the purposes of paragraph (d) of the definition of disabled person, the reference to a psychologist is a reference to a psychologist who:

(a) is registered with a Board established under a law of a State or Territory that registers psychologists in that State or Territory; and

(b) has qualifications or experience in assessing impairment in adults.

(4) A determination by the Minister for the purposes of paragraph (c) or (e) of the definition of disabled person is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

(5) If, in relation to a 24 hour care period and a child:

(a) an approved child care service provides care to the child during the whole of the period; or

(b) an approved child care service:

(i) provides care to the child during more than half of the period; and

(ii) during the remaining part of the period, when the service is not providing care to the child, has responsibility for the child;

the service providing the care, or providing the care and having the responsibility, is providing 24 hour care to the child.

(6) A week, for the purposes of child care benefit, commences on a Monday.

49 Subsection 8(1)

Repeal the subsection, substitute:

(1) The Secretary may determine:

(a) that an individual who is not an Australian resident is to be taken to be an Australian resident for the purposes of Division 4 of Part 3 (eligibility for child care benefit) for a period or indefinitely; and

(b) if the determination is for a period—the period in respect of which the individual is to be taken to be an Australian resident.

50 At the end of paragraphs 8(2)(a) and (b)

Add “for a period or indefinitely”.

51 Subsection 8(4)

Repeal the subsection, substitute:

(4) The Minister may make guidelines:

(a) relating to the making of determinations under subsection (1); and

(b) in particular, setting time limits applicable to the determining of periods under paragraph (1)(b).

52 Section 10

Repeal the section, substitute:

10 Effect of absence of child from care of approved child care service other than an approved occasional care service

Absence from part of a session

(1) For the purposes of this Act, if a child is absent from part only of a session of care provided by an approved child care service (other than an approved occasional care service) the service is taken to have provided that part of the session of care to the child.

Absence from all of a session

(2) For the purposes of this Act, if:

(a) a child is absent from all of a session of care that would otherwise have been provided to the child by an approved child care service (other than an approved occasional care service); and

(b) one of the following applies:

(i) the absence is due to the illness of the child, the individual in whose care the child is, that individual’s partner, or another individual with whom the child lives and a medical certificate covering that illness is obtained from a medical practitioner and given to the service;

(ii) the absence is due to the child’s attendance at a pre‑school;

(iii) the absence is due to alternative care arrangements being made for the child because the child does not have to be at school on a pupil‑free day;

(iv) the absence occurs in circumstances specified in a determination under subsection 11(1) as permitted circumstances for the purpose of this subparagraph;

(v) the absence occurs on a permitted absence day (see subsection (3));

the service is taken to have provided the session of care to the child.

Permitted absence days

(3) For the purposes of subparagraph (2)(b)(v), a permitted absence day is a day that meets the following requirements:

(a) the day is not a day:

(i) before the day the service has started providing care for the child; or

(ii) after the day the service has stopped providing care for the child (otherwise than temporarily);

(b) the child is absent from all of one or more sessions of care that would otherwise have been provided to the child by the approved child care service on the day (even if the child is not absent from some or all of another session or sessions of care provided by the service or another service on the day);

(c) the child’s absence from all of the one or more sessions of care is not covered by subparagraph (2)(b)(i), (ii), (iii) or (iv);

(d) before the day, not more than 29 permitted absence days in relation to the child have elapsed in the same financial year.

10A Effect of absence of child from care of approved child care service that is an approved occasional care service

Absence from part of a session

(1) For the purposes of this Act, if a child is absent from part only of a session of care provided by an approved child care service that is an approved occasional care service, the service is taken to have provided that part of the session of care to the child.

Absence from all of a session

(2) For the purposes of this Act, if:

(a) a child is absent from all of a session of care that would otherwise have been provided to the child by an approved child care service that is an approved occasional care service; and

(b) the absence occurs in circumstances specified in a determination under subsection 11(1) as permitted circumstances for the purpose of this paragraph;

the service is taken to have provided the session of care to the child.

53 Subsection 11(1)

Omit “subsection 10(2) or subparagraph 10(3)(b)(iv)”, substitute “subparagraph 10(2)(b)(iv) or paragraph 10A(2)(b)”.

54 Division 4 of Part 3

Repeal the Division, substitute:

Division 4—Eligibility for child care benefit

41 Overview of Division

(1) This Division deals with eligibility for child care benefit. Before a person may be determined under Division 4 of Part 3 of the Family Assistance Administration Act to be entitled to be paid child care benefit, the person must first be eligible for it.

Eligibility of individual for child care benefit

(2) An individual may be eligible for child care benefit:

(a) by fee reduction for care provided by an approved child care service (see section 43, Subdivision A); or

(b) for a past period for care provided by an approved child care service (see section 44, Subdivision B); or

(c) for a past period for care provided by a registered carer (see section 45, Subdivision C); or

(d) by single payment/in substitution because of the death of another individual (see section 46, Subdivision D).

Before an individual can be eligible under section 43, the individual must be conditionally eligible under section 42.

Eligibility of an approved child care service for child care benefit

(3) An approved child care service may be eligible for child care benefit by fee reduction for care provided by the service to a child at risk (see section 47, Subdivision E).

Subdivision A—Eligibility of an individual for child care benefit by fee reduction for care provided by an approved child care service

42 When an individual is conditionally eligible for child care benefit by fee reduction for care provided by an approved child care service

(1) An individual is conditionally eligible for child care benefit by fee reduction for care provided by an approved child care service to a child if:

(a) the child is an FTB child of the individual, or the individual’s partner; and

(b) the individual, or the individual’s partner:

(i) is an Australian resident; or

(ii) meets the requirements set out in subparagraph 729(2)(f)(ii), (iii), (iv) or (v) of the Social Security Act 1991 and is in Australia; or

(iii) is undertaking a course of study in Australia and receiving financial assistance directly from the Commonwealth for the purpose of undertaking that study; and

(c) where the FTB child is under 7 and born on or after 1 January 1996, either:

(i) the child meets the immunisation requirements set out in section 6; or

(ii) a pre‑notice period is operating in respect of the individual and the child (see subsection (3)); or

(iii) a 63 day notice period is operating in respect of the individual and the child (see section 57E of the Family Assistance Administration Act).

Secretary may determine that child is an FTB child

(2) The Secretary may determine that a child who is not an FTB child of an individual at a particular time is taken to be an FTB child of the individual at that time for the purposes of paragraph (1)(a).

(3) In subparagraph (1)(c)(ii), the reference to a pre‑notice period is a reference to the period of time that ends on the day before a 63 day notice period begins to operate in respect of the individual and the child.

Section subject to Subdivision F

(4) This section is subject to Subdivision F (which deals with limits on eligibility).

43 When an individual is eligible for child care benefit by fee reduction for care provided by an approved child care service

(1) An individual is eligible for child care benefit by fee reduction for a session of care provided by an approved child care service to a child if:

(a) when the session of care is provided, a determination is in force under Part 3 of the Family Assistance Administration Act with the effect that the individual is conditionally eligible for child care benefit by fee reduction in respect of the child; and

(b) the care is provided in Australia; and

(c) the individual, or the individual’s partner, has incurred a liability to pay for the session (whether or not the liability has been discharged).

Section subject to Subdivisions F and G

(2) This section is subject to Subdivisions F and G (which deal with limits on eligibility).

Subdivision B—Eligibility of an individual for child care benefit for a past period for care provided by an approved child care service

44 When an individual is eligible for child care benefit for a past period for care provided by an approved child care service

(1) An individual is eligible for child care benefit for a past period for a session of care provided by an approved child care service to a child if:

(a) the child is an FTB child of the individual, or the individual’s partner, during the session; and

(b) the care is provided in Australia; and

(c) the individual, or the individual’s partner, has incurred a liability to pay for the session (whether or not the liability has been discharged); and

(d) when a claim by the individual for payment of child care benefit in respect of the session is determined in accordance with Part 3 of the Family Assistance Administration Act, the individual, or the individual’s partner:

(i) is an Australian resident; or

(ii) meets the requirements set out in subparagraph 729(2)(f)(ii), (iii), (iv) or (v) of the Social Security Act 1991 and is in Australia; or

(iii) is undertaking a course of study in Australia and receiving financial assistance directly from the Commonwealth for the purpose of undertaking that study; and

(e) when a claim by the individual for payment of child care benefit in respect of the session is determined in accordance with Part 3 of the Family Assistance Administration Act, the requirement relating to immunisation set out in subsection (2) is met in respect of the child; and

(f) the session starts on or after the commencement of this Act.

Requirement relating to immunisation referred to in paragraph (1)(e)

(2) For the purposes of paragraph (1)(e), the requirement relating to immunisation is that, if the child is under 7 and is born on or after 1 January 1996, the child must meet the immunisation requirements set out in section 6.

Secretary may determine that child is an FTB child

(3) The Secretary may determine that a child who is not an FTB child of an individual during the session of care is taken to be an FTB child of the individual during that session for the purposes of paragraph (1)(a).

Section subject to Subdivisions F and G

(4) This section is subject to Subdivisions F and G (which deal with limits on eligibility).

Subdivision C—Eligibility of an individual for child care benefit for a past period for care provided by a registered carer

45 When an individual is eligible for child care benefit for a past period for care provided by a registered carer

(1) An individual is eligible for child care benefit for a past period for care provided (see section 12) by a registered carer to a child if:

(a) the child is an FTB child of the individual, or the individual’s partner, during the period; and

(b) the care is provided in Australia; and

(c) the child is not an FTB child of the registered carer, or the partner of the carer; and

(d) the individual, or the individual’s partner, is liable to pay for the care and the care has been paid for; and

(e) the individual, and the individual’s partner, satisfy the work/training/study test at some time during the week in which the care is provided; and

(f) when a claim by the individual for payment of child care benefit in respect of the period is determined in accordance with Part 3 of the Family Assistance Administration Act, the individual, or the individual’s partner:

(i) is an Australian resident; or

(ii) meets the requirements set out in subparagraph 729(2)(f)(ii), (iii), (iv) or (v) of the Social Security Act 1991 and is in Australia; or

(iii) is undertaking a course of study in Australia and receiving financial assistance directly from the Commonwealth for the purpose of undertaking that study; and

(g) when a claim by the individual for payment of child care benefit in respect of the period is determined in accordance with Part 3 of the Family Assistance Administration Act, the requirement relating to immunisation set out in subsection (2) is met in respect of the child; and

(h) the care is not provided as part of the compulsory education program in the State or Territory where the care is provided; and

(i) the care starts on or after the commencement of this Act.

Requirement relating to immunisation referred to in paragraph (1)(g)

(2) For the purposes of paragraph (1)(g), the requirement relating to immunisation is that, if:

(a) the child is under 7 and is born on or after 1 January 1996; and

(b) the individual has previously made a claim for payment of child care benefit under Part 3 of the Family Assistance Administration Act in respect of a period of care provided by a registered carer to the child;

the child must meet the immunisation requirements set out in section 6.

Secretary may determine that child is an FTB child

(3) The Secretary may determine that a child who is not an FTB child of an individual during the period of care is taken to be an FTB child of the individual during that period for the purposes of paragraph (1)(a).

Section subject to sections 48 and 49

(4) This section is subject to sections 48 and 49 (which deal with limits on eligibility).

Subdivision D—Eligibility of an individual for child care benefit by single payment/in substitution because of the death of another individual

46 Eligibility for child care benefit if a conditionally eligible or eligible individual dies

If deceased eligible for child care benefit

(1) If:

(a) an individual is eligible for an amount of child care benefit in respect of a child (the subject amount) under section 43, 44 or 45; and

(b) the individual dies; and

(c) before the individual died, the subject amount had not been paid to the individual (whether or not a claim under Part 3 of the Family Assistance Administration Act had been made); and

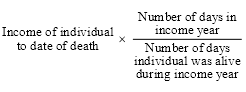

(d) another individual makes a claim under that Part for payment of child care benefit in respect of the child because of the death of a person, stating that he or she wishes to become eligible for so much of the subject amount as does not relate to any period before the beginning of the income year preceding the income year in which the individual died; and

(e) the Secretary considers that the other individual ought to be eligible for that much of the subject amount;

the other individual is eligible for that much of the subject amount and no‑one else is, or can become, eligible for or entitled to be paid any of the subject amount.

If deceased conditionally eligible for child care benefit by fee reduction

(2) If:

(a) a determination of conditional eligibility under section 50F of the Family Assistance Administration Act is in force in respect of an individual with the effect that an individual is conditionally eligible for child care benefit by fee reduction in respect of a child; and

(b) the individual dies; and

(c) before the individual died, the individual’s entitlement to be paid child care benefit by fee reduction had not been determined under section 51B of the Family Assistance Administration Act; and

(d) another individual makes a claim under Part 3 of that Act for payment of child care benefit in respect of the child because of the death of an individual, stating that he or she wishes to become eligible for such amount (if any) of child care benefit that the first individual would have been entitled to be paid as does not relate to any period before the beginning of the income year preceding the income year in which the first individual died; and

(e) the Secretary considers that the other individual ought to be eligible for the amount;

the other individual is eligible for the amount and no‑one else is, or can become, eligible for or entitled to be paid that amount.

Subdivision E—Eligibility of an approved child care service for child care benefit by fee reduction for care provided by the service to a child at risk

47 When an approved child care service is eligible for child care benefit by fee reduction for care provided to a child at risk

(1) An approved child care service is eligible for child care benefit by fee reduction for a session of care provided by the service to a child if:

(a) at the time the care is provided, the service believes the child is at risk of serious abuse or neglect; and

(b) the care is provided in Australia.

Section subject to Subdivisions F and G

(2) This section is subject to Subdivisions F and G (which deal with limits on eligibility).

Subdivision F—Limitations on conditional eligibility or eligibility for child care benefit for care provided by an approved child care service or a registered carer that do not relate to hours

48 No multiple eligibility for same care

(1) If, apart from this section, more than one individual would be eligible, or conditionally eligible, for child care benefit in respect of the same session, or period, of care for the same child under Subdivision A, B or C, the only individual who is eligible, or conditionally eligible, is the one whom the Secretary determines to be eligible.

Determination to be in accordance with any Ministerial rules

(2) The Secretary must make the determination under subsection (1) in accordance with any rules in force under subsection (3).

Ministerial rules

(3) The Minister may make rules in accordance with which the Secretary is to make determinations under subsection (1).

Disallowable instrument

(4) The rules are a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

49 Person not conditionally eligible or eligible for child care benefit if child in care under a welfare law or child in exempt class of children

(1) A person is not eligible, or conditionally eligible, for child care benefit as mentioned in Subdivision A, B, C or E if the child concerned:

(a) is under the care (however described) of a person under:

(i) a child welfare law of a State or Territory; or

(ii) a law of a State or Territory that is taken to be a child welfare law of the State or Territory in a determination under subsection (2); or

(b) is a member of a class specified in a determination under subsection (3).

Child welfare law

(2) The Minister may determine that a specified law of a State or Territory is taken to be a child welfare law of the State or Territory for the purposes of subparagraph (1)(a)(ii).

Exempt class of children

(3) The Minister may determine that children included in a specified class are children in respect of whom no‑one is eligible for child care benefit under this Division.

Disallowable instrument

(4) A determination under this section is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

50 Person not eligible for child care benefit while an approved child care service’s approval is suspended

(1) If:

(a) except for the operation of this section, a person would be eligible for child care benefit for care provided by an approved child care service to a child as mentioned in Subdivision A, B or E; and

(b) at the time a session of care is provided to the child, the service’s approval under section 195 of the Family Assistance Administration Act has been suspended under section 200 of that Act;

the person is not eligible for child care benefit for the sessions of care provided by the service during the period when the service’s approval is suspended.

(2) For the purposes of subsection (1), an approved child care service’s approval is suspended for the period beginning when that suspension takes effect and ending on the day with effect from which that suspension is revoked.

51 Approved child care service not eligible for care provided to a child at risk if Minister so determines

Limit on eligibility under section 47

(1) The Minister may determine that, in specified circumstances, after a specified period or specified periods of eligibility of approved child care services for child care benefit by fee reduction in respect of a child under section 47, the services are not able to be eligible under that section for any further period in respect of the child.

Disallowable instrument

(2) A determination under this section is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

Subdivision G—Limitations on eligibility for child care benefit for care provided by an approved child care service relating to hours

52 Limit on eligibility for child care benefit relating to hours

Limit on eligibility

(1) Despite:

(a) an individual or an approved child care service (a fee reduction claimant) being eligible for child care benefit by fee reduction under section 43 or 47 respectively; or

(b) an individual (a past period claimant) being eligible under section 44 for child care benefit for a past period;

the number of hours, in sessions of care in a week for which the claimant is eligible, is limited.

How limit is worked out

(2) The limit is worked out using this Subdivision. The Minister’s determination under section 57A deals with the hours that are to count towards that limit in certain circumstances.

If fee reduction claimant is an individual—how the limit is used

(3) If a fee reduction claimant who is an individual, the Secretary determines the limit under section 50H of the Family Assistance Administration Act while the claimant is conditionally eligible for child care benefit by fee reduction.

(4) The limit may be varied under:

(a) section 59F, 62C or 65D of the Family Assistance Administration Act; or

(b) Subdivision U of Division 4 of Part 3 of that Act.

The limit, and variations to it made under Subdivision U of Division 4 of Part 3 of the Family Assistance Administration Act or section 65D of that Act, are worked out using this Subdivision as if the reference in subsection (1) to an individual being eligible under section 43 for child care benefit was a reference to the individual being conditionally eligible under section 42. The Secretary applies the limit when determining, under section 51B of the Family Assistance Administration Act, the amount of child care benefit the claimant is entitled to be paid.

If fee reduction claimant is a service—how the limit is used

(5) If a fee reduction claimant that is an approved child care service, the limit is taken to be determined under section 54C of the Family Assistance Administration Act. The Secretary applies the limit when determining, under section 54B of the Family Assistance Administration Act, the amount of child care benefit the claimant is entitled to be paid.

Past period claimant—how the limit is used

(6) If a past period claimant, the Secretary applies the limit when determining, under section 52E of the Family Assistance Administration Act, the amount the claimant is entitled to be paid.

53 Weekly limit of hours

Weekly limit for fee reduction claimants

(1) The weekly limit of hours applicable to a fee reduction claimant is as provided for in this Subdivision:

(a) a limit of 20 hours; or

(b) a limit of 50 hours: or

(c) a limit of more than 50 hours; or

(d) a 24 hour care limit (but see section 56 which provides that this limit can only apply if the care is not provided by an approved occasional care service).

Weekly limit for past period claimants

(2) The weekly limit of hours applicable to a past period claimant is, as provided for in this Subdivision:

(a) a limit of 20 hours; or

(b) a limit of 50 hours.

20 hour limit applies if no other limit does

(3) In a week, a limit of 20 hours applies to a claimant if:

(a) in the case of a fee reduction claimant—a limit of 50 hours, a limit of more than 50 hours or a 24 hour care limit does not apply in respect of the week; and

(b) in the case of a past period claimant—a limit of 50 hours does not apply in respect of the week.

Weekly limit of hours must not include unauthorised 24 hour care

(4) The weekly limit of hours applicable to a claimant under this section, other than a 24 hour care limit under paragraph (1)(d), must not include hours during which an approved child care service is providing 24 hour care to the child.

54 Circumstances when a limit of 50 hours applies

Overview of section

(1) This section sets out the circumstances in which a limit of 50 hours for sessions of care provided by an approved child care service to a child applies in a week to the eligibility of:

(a) a fee reduction claimant (see paragraph 52(1)(a)); or

(b) a past period claimant (see paragraph 52(1)(b)).

If claimant is an individual and work/training/study test satisfied

(2) A limit of 50 hours in the week applies to a fee reduction claimant who is an individual or to a past period claimant if that claimant, and that claimant’s partner (if any), satisfy the work/training/study test at some time in the week.

If fee reduction claimant is an approved child care service and work/training/study test satisfied

(3) A limit of 50 hours in the week applies to a fee reduction claimant that is an approved child care service if:

(a) the person in whose care the child last was before the first session of care in the week is an individual; and

(b) the individual, and the individual’s partner (if any), satisfy the work/training/study test at some time in the week.

If claimant is an individual and carer allowance is payable

(4) A limit of 50 hours in the week applies to a fee reduction claimant who is an individual, or to a past period claimant, if carer allowance for a disabled child (within the meaning of section 952 of the Social Security Act 1991) is payable to the claimant or the claimant’s partner (if any) for some or all of the week:

(a) in respect of an FTB child of the claimant or that claimant’s partner; and

(b) pursuant to a claim under that Act that was determined before the week.

If fee reduction claimant is an approved child care service and carer allowance is payable

(5) A limit of 50 hours in the week applies to a fee reduction claimant that is an approved child care service if:

(a) the person in whose care the child last was before the first session of care in the week is an individual; and

(b) carer allowance for a disabled child (within the meaning of section 952 of the Social Security Act 1991) is payable to the individual or the individual’s partner (if any) for some or all of the week:

(i) in respect of an FTB child of the individual or the individual’s partner; and

(ii) pursuant to a claim under that Act that was determined before the week.

If claimant and partner are disabled persons

(6) A limit of 50 hours in the week applies to a fee reduction claimant who is an individual or to a past period claimant if, during the week:

(a) the child is an FTB child of the claimant and that claimant is a disabled person (see subsection 3(1)); and

(b) the claimant’s partner (if any) is also a disabled person.

If fee reduction claimant is an approved child care service—disabled persons

(7) A limit of 50 hours in the week applies to a fee reduction claimant that is an approved child care service if:

(a) the person in whose care the child last was before the first session of care in the week is an individual; and

(b) during the week, the child is an FTB child of the individual and that individual is a disabled person (see subsection 3(1)); and

(c) during the week, the individual’s partner (if any) is also a disabled person.

If fee reduction claimant is an individual and Secretary considers that exceptional circumstances exist

(8) A limit of 50 hours in the week applies to a fee reduction claimant who is an individual if the Secretary considers that, for a specified period that includes, or is the same as, the week, the child needs or needed more than 20, up to a maximum of 50, hours of care in a week because exceptional circumstances exist or existed in the period in relation to the claimant.

If fee reduction claimant is an approved child care service and Secretary considers that exceptional circumstances exist

(9) A limit of 50 hours in the week applies to a fee reduction claimant that is an approved child care service if:

(a) the person in whose care the child last was before the first session of care in the week is an individual; and

(b) the Secretary considers that, for a specified period that includes, or is the same as, the week, the child needs or needed more than 20, up to a maximum of 50, hours of care in a week because exceptional circumstances exist or existed in the period in relation to the individual.

Service considers that child at risk

(10) Subject to subsection (11), a limit of 50 hours in the week applies to a fee reduction claimant if:

(a) in the case where the claimant is an individual—the approved child care service providing care to the child; or

(b) in the case where the claimant is an approved child care service—the service;

certifies that, for a specified period that includes, or is the same as, the week, the child needs or needed more than 20, up to a maximum of 50, hours of care in a week because the child is or has been at risk of serious abuse or neglect.

Limitation on service giving certificates under subsection (10)

(11) An approved child care service providing care to a child may only give a certificate under subsection (10) if the period specified in the certificate, and the period specified in each other certificate (if any) given by the service under subsection (10) in respect of the child and the same financial year, do not in total exceed 13 weeks.

Secretary considers that child at risk

(12) A limit of 50 hours in the week applies to a fee reduction claimant if:

(a) either:

(i) in the case where the claimant is an individual—the approved child care service providing care to the child; or

(ii) in the case where the claimant is an approved child care service—the service;

has given one or more certificates under subsection (10), such that the total period specified in the certificates in respect of the child in the same financial year equals 13 weeks; and

(b) the Secretary considers that the child needs or needed more than 20, up to a maximum of 50, hours of care in a week in a specified period beginning at any time after those 13 weeks, because the child is or has been at risk of serious abuse or neglect; and

(c) the week falls within, or is the same as, the period specified by the Secretary.

Determination that service is sole provider in area

(13) A limit of 50 hours in the week applies to a fee reduction claimant or past period claimant if a determination is in force under section 57 (sole provider) during the week in respect of the approved child care service providing the care to the child.

Approved outside school hours care service providing care to child

(14) A limit of 50 hours in the week applies to a fee reduction claimant or past period claimant:

(a) who is an individual; or

(b) that is an approved outside school hours care service providing care to the child;

if the Secretary considers that, during the week, the claimant needs or needed care before or after school for the child from an approved outside school hours care service.

55 Circumstances when a limit of more than 50 hours applies

Overview of section

(1) This section sets out the circumstances in which a limit of more than 50 hours for sessions of care provided by an approved child care service to a child applies in a week to the eligibility of a fee reduction claimant (see paragraph 52(1)(a)).

Work/disability test satisfied if fee reduction claimant is an individual

(2) A limit of more than 50 hours in the week applies to a fee reduction claimant who is an individual if:

(a) the Secretary considers that for a specified period or indefinitely (if no period is specified), the claimant needs or needed care for the child for a particular number of hours in a week more than 50; and

(b) the Secretary considers that the amount of care is needed because the individual, and that individual’s partner (if any), satisfy the work/disability test (see subsections 57E(1), (2) and (3)) for the particular number of hours during the period or indefinitely, as the case may be; and

(c) the week falls within, or is the same as, the period or, if no period is specified, the week is one after the start of the indefinite period.

The amount of the limit is the particular number of hours more than 50.

Work/disability test satisfied if fee reduction claimant is an approved child care service

(3) A limit of more than 50 hours in the week applies to a fee reduction claimant that is an approved child care service if:

(a) the person in whose care the child last was before the first session of care in the week is an individual; and

(b) the Secretary considers:

(i) that for a specified period the individual needs or needed care for the child for a particular number of hours in a week more than 50; and

(ii) that the amount of care is needed because the individual, and that individual’s partner (if any), satisfy the work/disability test (see subsections 57E(1), (2) and (3)) for the particular number of hours during the period; and

(c) the week falls within, or is the same as, the period.

The amount of the limit is the particular number of hours more than 50.

If fee reduction claimant is an individual and Secretary considers that exceptional circumstances exist

(4) A limit of more than 50 hours in the week applies to a fee reduction claimant who is an individual if the Secretary considers:

(a) that for a specified period that includes, or is the same as, the week, the child needs or needed care, for a particular number of hours in a week more than 50; and

(b) the reason the child needs or needed the care is because exceptional circumstances exist or existed in the period in relation to the claimant.

The amount of the limit is the particular number of hours more than 50.

If fee reduction claimant is an approved child care service and Secretary considers that exceptional circumstances exist

(5) A limit of more than 50 hours in the week applies to a fee reduction claimant that is an approved child care service if:

(a) the person in whose care the child last was before the first session of care in the week is an individual; and

(b) the Secretary considers:

(i) that, for a specified period that includes, or is the same as, the week, the child needs or needed care, for a particular number of hours in a week more than 50; and

(ii) that the reason the child needs or needed the care is because exceptional circumstances exist or existed in the period in relation to the individual.

The amount of the limit is the particular number of hours more than 50.

Service considers that child at risk

(6) Subject to subsection (7), a limit of more than 50 hours in the week applies to a fee reduction claimant if:

(a) in the case where the claimant is an individual—the approved child care service providing care to the child; or

(b) in the case where the claimant is an approved child care service—the service;

certifies that, for a specified period that includes, or is the same as, the week, the child needs or needed a particular number of hours of care in a week more than 50 because the child is or has been at risk of serious abuse or neglect. The amount of the limit is the particular number of hours more than 50 that the service specifies.

Limitation on service giving certificates under subsection (6)

(7) An approved child care service providing care to a child may only give a certificate under subsection (6) if the period specified in the certificate, and the period specified in each other certificate (if any) given by the service under that subsection in relation to the child and the same financial year, does not in total exceed 13 weeks.

Secretary considers that child at risk

(8) A limit of more than 50 hours in the week applies to a fee reduction claimant if:

(a) either:

(i) in the case where the claimant is an individual—the approved child care service providing care to the child; or

(ii) in the case where the claimant is an approved child care service—the service;

has given one or more certificates under subsection (6) such that the total period specified in the certificates in respect of the child in the same financial year equals 13 weeks; and

(b) the Secretary considers that the child needs or needed a particular number of hours of care in a week more than 50 in a specified period beginning at any time after those 13 weeks, because the child is or has been at risk of serious abuse or neglect; and

(c) the week falls within, or is the same as, the period specified by the Secretary.

The amount of the limit is the particular number of hours more than 50.

56 Circumstances when 24 hour care limit applies

Overview of section

(1) This section sets out the circumstances in which a 24 hour care limit for sessions of care provided to a child applies in a week to the eligibility of certain fee reduction claimants (see paragraph 52(1)(a)). A 24 hour care limit can only apply if the care is provided by an approved child care service other than an approved occasional care service.

Meaning of fee reduction claimant and approved child care service

(2) In this section (other than subsection (1)):

(a) fee reduction claimant does not include an individual if the care the individual is eligible for is provided by an approved occasional care service; and

(b) approved child care service does not include an approved occasional care service.

24 hour care certified by a service—if claimant is an individual

(3) Subject to subsection (5), a 24 hour care limit applies in the week to a fee reduction claimant who is an individual if the approved child care service providing care to the child certifies that the child needs, or needed, 24 hour care in the week for one or more 24 hour care periods specified in the certificate, because neither the claimant, nor the claimant’s partner (if any), is able to care for the child during those periods for the reason that:

(a) both the claimant and the claimant’s partner (if any) have work related commitments during those periods; or

(b) exceptional circumstances exist during those periods.

24 hour care certified by a service—if claimant is a service

(4) Subject to subsection (5), a 24 hour care limit applies in the week to a fee reduction claimant that is an approved child care service if:

(a) the person in whose care the child last was before the first session of care in the week is an individual; and

(b) the service certifies that the child needs, or needed, 24 hour care in the week for one or more 24 hour care periods specified in the certificate, because neither the individual, nor the individual’s partner (if any), is able to care for the child during those periods for the reason that:

(i) both the individual and that individual’s partner (if any) have work related commitments during those periods; or

(ii) exceptional circumstances exist during those periods.

Limitation on service giving certificates under subsection (3) or (4)

(5) An approved child care service may only give a certificate under subsection (3) or (4) if the number of 24 hour care periods specified in the certificate in relation to a child, together with the number of 24 hour care periods specified in each other certificate (if any) given by the service, or any other approved child care service, in relation to the child and the same financial year, does not in total exceed 14.

24 hour care decided by the Secretary

(6) Subject to subsection (7), a 24 hour care limit applies in the week to a fee reduction claimant if:

(a) the approved child care service providing care to the child has given a certificate under subsection (3) or (4) such that the total of the 24 hour care periods specified in that certificate and other certificates (if any) given by the service, or any other approved child care service, in respect of the child in the same financial year equals 14; and

(b) the Secretary considers that, at some time after those 14 24 hour care periods, the child needs or needed 24 hour care for one or more specified 24 hour care periods in the week because:

(i) in the case where the claimant is an individual—neither the claimant nor the claimant’s partner (if any); or

(ii) in the case where the claimant is the approved child care service providing care to the child—neither the individual in whose care the child last was before the first session of care in the week nor the individual’s partner (if any);

is able to care for the child during those periods; and

(c) the Secretary considers that the reason for that inability is:

(i) because both the individual and the individual’s partner (if any) have work related commitments during those periods; or

(ii) because exceptional circumstances exist during those periods.

Limitation on Secretary’s decision making under subsection (5)

(7) Subject to subsection (8), in respect of a child during a financial year, the Secretary may make a decision under subsection (6) in respect of only 14 24 hour care periods.

Maximum of 28 24 hour care periods may be lifted in certain circumstances

(8) If:

(a) in respect of the child during a financial year, there have already been certificates given, and decisions of the Secretary made, in which the total of the 24 hour care periods specified is 28; and

(b) the Secretary is satisfied that it is essential in the circumstances that the child receive one or more further periods of 24 hour care during the financial year;

a 24 hour care limit applies in the week to a fee reduction claimant if:

(c) the Secretary considers that, at some time after those 28 24 hour care periods, the child needs or needed 24 hour care for one or more specified 24 hour care periods in the week because:

(i) in the case where the claimant is an individual—neither the claimant nor the claimant’s partner (if any); or

(ii) in the case where the claimant is the approved child care service providing care to the child—neither the individual in whose care the child last was before the first session of care in the week nor the individual’s partner (if any);

is able to care for the child during those periods; and

(d) the Secretary considers that the reason for that inability is:

(i) because both the individual and the individual’s partner (if any) have work related commitments during those periods; or

(ii) because exceptional circumstances exist during those periods.

57 Minister’s determination of sole provider

(1) If the Minister considers that:

(a) an approved child care service is the sole provider in an area of the kind of care the service provides; and

(b) the service would be likely to close if the Minister were not to make a determination that would be in force for a period of one or more weeks under this subsection in relation to the service;

the Minister may make a determination to that effect (while a determination is in force, a weekly limit of 50 hours applies under subsection 54(13)).

(2) The determination:

(a) may be expressed to be subject to conditions, and

(b) must specify the period of one or more weeks; and

(c) is in force during the period specified.

(3) The determination may be varied by the Minister from a date, or for a period, specified in the revocation.

(4) The determination may be revoked by the Minister from a date specified in the revocation.

(5) The determination, or a variation of a determination, may only be made on application by the approved child care service concerned.

(6) The application must:

(a) be made in a form and manner; and

(b) contain any information; and

(c) be accompanied by any documents;

required by the Secretary.

(7) The Secretary must give notice of the determination, or of a variation or revocation of a determination, to the approved child care service the subject of the determination. A determination, variation or revocation is not ineffective by reason only that the notice is not given, or if given, that all of the requirements are not complied with.

57A Minister to determine which hours in sessions of care are to count towards the limits

(1) The Minister must determine rules relating to how to work out the hours in sessions of care provided by an approved child care service to a child in a week that are to count towards:

(a) the limit of 20 hours; or

(b) the limit of 50 hours; or

(c) the limit of more than 50 hours.

(2) For the purposes of subsection (1), sessions of care means sessions other than sessions for which:

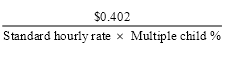

(a) the standard hourly rate set out in item 1 of the table in subclause 4(1) of Schedule 2 applies; and

(b) a part‑time % is 100% under subclause 2(2) of Schedule 2.

57B Minister may determine rules

The Minister may determine rules relating to:

(a) the giving of certificates by an approved child care service under subsection 54(10), 55(6) or subsection 56(3) or (4); and

(b) the making of decisions by the Secretary under section 54 or 55 or subsection 56(6) or (8); and

(c) the making of the Minister’s determinations under section 57; and

(d) the meaning of terms used in this Subdivision.

57C Certificates to be given and decisions and determinations to be made in accordance with rules

All of the following must be made in accordance with rules (if any) in force under section 57B:

(a) a certificate given by an approved child care service under subsection 54(10), 55(6) or subsection 56(3) or (4);

(b) a decision made by the Secretary under section 54 or 55 or subsection 56(6) or (8);

(c) a determination made by the Minister under section 57.

57D Minister’s determinations subject to disallowance

A determination under section 57A or 57B is a disallowable instrument for the purposes of section 46A of the Acts Interpretation Act 1901.

57E Meaning of work/disability test

Meaning of satisfying the work/disability test for individual without partner

(1) An individual who does not have a partner satisfies the work/disability test in relation to care provided by an approved child care service to a child if the individual is unable to care for the child because of work related commitments.

Meaning of satisfying the work/disability test for individual and partner where one of the individuals has work related commitments and the other is a disabled person

(2) An individual who has a partner and the partner satisfy the work/disability test in relation to care provided by an approved child care service to a child if:

(a) one of the individuals is unable to care for the child because of work related commitments; and

(b) the other individual is a disabled person.

Meaning of satisfying the work/disability test for individual and partner where both of the individuals have work related commitments

(3) An individual who has a partner and the partner satisfy the work/disability test in relation to care provided by an approved child care service if both of the individuals are unable to care for the child at the same time because of work related commitments.

55 Divisions 4 and 5 of Part 4

Repeal the Divisions, substitute:

Division 4—Child care benefit

Subdivision A—Overview of Division

69 Overview of Division

(1) Subdivisions B and C deal with the rate of fee reductions and child care benefit applicable if care is provided by an approved child care service.

(2) Subdivision B sets out the circumstances in which the rate of fee reductions and child care benefit for care provided by an approved child care service are calculated using Schedule 2 and when they are calculated under Subdivision C.

(3) Subdivision C deals with the rate applicable in respect of a session of care provided by an approved child care service to a child if:

(a) the service gives a certificate under section 76; or

(b) the Secretary makes a determination under subsection 81(2), (3) or (4).

(4) Subdivision C applies if:

(a) a determination of conditional eligibility is in force in respect of an individual with the effect that the individual is conditionally eligible for child care benefit by fee reduction; or

(b) an approved child care service is eligible under section 47 for child care benefit by fee reduction for care provided by the service to the child.

(5) Subdivision D deals with the rate of child care benefit applicable to an individual who is eligible under section 45 for child care benefit for a past period for care provided by a registered carer.

Subdivision B—General provisions relating to rate of fee reductions and child care benefit for care provided by an approved child care service

70 Application of Subdivision to parts of sessions of care

This Subdivision applies to a rate of fee reductions or child care benefit for a part of a session of care as if a reference in this Subdivision to a session of care included a reference to a part of a session of care.

71 Weekly limit on child care benefit for care provided by an approved child care service

The total amount of child care benefit for sessions of care provided by an approved child care service to a child in a week is not to exceed:

(a) if an individual is eligible under section 43 for child care benefit by fee reduction for sessions of care provided to the child in the week—the amount that the service would have charged the individual, if the individual was not so eligible, for the sessions; or

(b) if an individual is eligible under section 44 for child care benefit for a past period for sessions of care provided to the child in the week—the amount charged by the service for the sessions; or

(c) if the service is eligible under section 47 for child care benefit by fee reduction for sessions of care provided in the week—the amount that, if the service had not been so eligible, the service would have charged the individual in whose care the child last was before the first session of care provided to the child in that week for the sessions.

72 Weekly limit on rate of fee reductions while individual is conditionally eligible for care provided by an approved child care service

(1) If a determination of conditional eligibility under section 50F of the Family Assistance Administration Act is in force in respect of an individual and a child for child care benefit by fee reduction for care provided by an approved child care service to the child, the rate of fee reductions for sessions of care provided by the service to the child in a week is limited.

(2) The rate is not to exceed the amount that the service would have charged the individual, if the individual were not so conditionally eligible, for sessions of care provided by the service to the child in that week, up to the weekly limit of hours determined as applicable to the individual under section 50H of the Family Assistance Administration Act.

73 Rate of fee reductions or child care benefit—individual conditionally eligible or eligible under section 43

Individual conditionally eligible for child care benefit