An Act about a goods and services tax to implement A New Tax System, and for related purposes

Chapter 1—Introduction

Part 1‑1—Preliminary

Division 1—Preliminary

1‑1 Short title

This Act may be cited as the A New Tax System (Goods and Services Tax) Act 1999.

1‑2 Commencement

(1) This Act commences on 1 July 2000.

1‑3 Commonwealth‑State financial relations

The Parliament acknowledges that the Commonwealth:

(a) will introduce legislation to provide that the revenue from the GST will be granted to the States, the Australian Capital Territory and the Northern Territory; and

(b) will maintain the rate and base of the GST in accordance with the Agreement on Principles for the Reform of Commonwealth‑State Financial Relations endorsed at the Special Premiers’ Conference in Canberra on 13 November 1998.

1‑4 States and Territories are bound by the GST law

The *GST law binds the Crown in right of each of the States, of the Australian Capital Territory and of the Northern Territory. However, it does not make the Crown liable to be prosecuted for an offence.

Part 1‑2—Using this Act

Division 2—Overview of the GST legislation

2‑1 What this Act is about

This Act is about the GST.

It begins (in Chapter 2) with the basic rules about the GST, and then sets out in Chapter 3 the exemptions from the GST and in Chapter 4 the special rules that can apply in particular cases.

It concludes with definitions and other interpretative material.

Note: The GST is imposed by 6 Acts, the most important of which are:

(a) the A New Tax System (Goods and Services Tax Imposition—General) Act 1999; and

(b) the A New Tax System (Goods and Services Tax Imposition—Customs) Act 1999; and

(c) the A New Tax System (Goods and Services Tax Imposition—Excise) Act 1999.

2‑5 The basic rules (Chapter 2)

Chapter 2 has the basic rules for the GST, including:

when and how the GST arises, and who is liable to pay it;

when and how input tax credits arise, and who is entitled to them;

how to work out payments and refunds of GST;

when and how the payments and refunds are to be made.

2‑10 The exemptions (Chapter 3)

Chapter 3 sets out the supplies and importations that are GST‑free or input taxed.

2‑15 The special rules (Chapter 4)

Chapter 4 has special rules which, in particular cases, have the effect of modifying the basic rules in Chapter 2.

Note: There is a checklist of special rules at the end of Chapter 2 (in Part 2‑8).

2‑20 Miscellaneous (Chapter 5)

Chapter 5 deals with miscellaneous matters.

2‑25 Interpretative provisions (Chapter 6)

Chapter 6 contains the Dictionary, which sets out a list of all the terms that are defined in this Act. It also sets out the meanings of some important concepts and rules on how to interpret this Act.

2‑30 Administration, collection and recovery provisions in the Taxation Administration Act 1953

Schedule 1 to the Taxation Administration Act 1953 contains provisions relating to the administration of the GST, and to collection and recovery of amounts of GST.

Division 3—Defined terms

3‑1 When defined terms are identified

(1) Many of the terms used in the law relating to the GST are defined.

(2) Most defined terms in this Act are identified by an asterisk appearing at the start of the term: as in “*enterprise”. The footnote that goes with the asterisk contains a signpost to the Dictionary definitions starting at section 195‑1.

3‑5 When terms are not identified

(1) Once a defined term has been identified by an asterisk, later occurrences of the term in the same subsection are not usually asterisked.

(2) Terms are not asterisked in the non‑operative material contained in this Act.

Note: The non‑operative material is described in Division 4.

(3) The following basic terms used throughout the Act are not identified with an asterisk.

Common definitions that are not asterisked |

Item | This term: |

1 | acquisition |

2 | amount |

3 | Commissioner |

4 | entity |

5 | goods |

6 | GST |

7 | import |

8 | indirect tax zone |

9 | individual |

10 | input tax credit |

11 | supply |

12 | tax period |

13 | thing |

14 | you |

3‑10 Identifying the defined term in a definition

Within a definition, the defined term is identified by bold italics.

Division 4—Status of Guides and other non‑operative material

4‑1 Non‑operative material

In addition to the operative provisions themselves, this Act contains other material to help you identify accurately and quickly the provisions that are relevant to you and to help you understand them.

This other material falls into 2 main categories.

4‑5 Explanatory sections

One category is the explanatory section in many Divisions. Under the section heading “What this Division is about”, a short explanation of the Division appears in boxed text.

Explanatory sections form part of this Act but are not operative provisions. In interpreting an operative provision, explanatory sections may only be considered for limited purposes. They are set out in section 182‑10.

4‑10 Other material

The other category consists of material such as notes and examples. These also form part of the Act. They are distinguished by type size from the operative provisions (except for formulas), but are not kept separate from them.

Chapter 2—The basic rules

Division 5—Introduction

5‑1 What this Chapter is about

This Chapter sets out the basic rules for the GST. In particular, these rules will tell you:

• where liability for GST arises;

• where entitlements to input tax credits arise;

• how the amounts of GST and input tax credits are combined to work out the amount payable by you or to you;

• when and how that amount is to be paid.

5‑5 The structure of this Chapter

The diagram on the next page shows how the basic rules in this Chapter relate to each other. It also shows their relationship with:

• the exemptions (Chapter 3)—these provisions exempt from the GST what would otherwise be taxable; and

• the special rules (Chapter 4)—these provisions modify the basic rules in particular situations, often in quite limited ways.

Part 2‑1—The central provisions

Division 7—The central provisions

7‑1 GST and input tax credits

(1) GST is payable on *taxable supplies and *taxable importations.

(2) Entitlements to input tax credits arise on *creditable acquisitions and *creditable importations.

For taxable supplies and creditable acquisitions, see Part 2‑2.

For taxable importations and creditable importations, see Part 2‑3.

7‑5 Net amounts

Amounts of GST and amounts of input tax credits are set off against each other to produce a *net amount for a tax period (which may be altered to take account of *adjustments).

For net amounts (including adjustments to net amounts), see Part 2‑4.

7‑10 Tax periods

Every entity that is *registered, or *required to be registered, has tax periods applying to it.

For registration, see Part 2‑5.

For tax periods, see Part 2‑6.

7‑15 Payments and refunds

The amount *assessed as being the *net amount for a tax period is the amount that the entity must pay to the Commonwealth, or the Commonwealth must refund to the entity, in respect of the period.

For payments and refunds (and GST returns), see Part 2‑7.

Note 1: For assessment of net amounts, see Division 155 in Schedule 1 to the Taxation Administration Act 1953.

Note 2: Refunds may be set off against your other liabilities (if any) under laws administered by the Commissioner.

Part 2‑2—Supplies and acquisitions

Division 9—Taxable supplies

Table of Subdivisions

9‑A What are taxable supplies?

9‑B Who is liable for GST on taxable supplies?

9‑C How much GST is payable on taxable supplies?

9‑1 What this Division is about

GST is payable on taxable supplies. This Division defines taxable supplies, states who is liable for the GST, and describes how to work out the GST on supplies.

Subdivision 9‑A—What are taxable supplies?

9‑5 Taxable supplies

You make a taxable supply if:

(a) you make the supply for *consideration; and

(b) the supply is made in the course or furtherance of an *enterprise that you *carry on; and

(c) the supply is *connected with the indirect tax zone; and

(d) you are *registered, or *required to be registered.

However, the supply is not a *taxable supply to the extent that it is *GST‑free or *input taxed.

9‑10 Meaning of supply

(1) A supply is any form of supply whatsoever.

(2) Without limiting subsection (1), supply includes any of these:

(a) a supply of goods;

(b) a supply of services;

(c) a provision of advice or information;

(d) a grant, assignment or surrender of *real property;

(e) a creation, grant, transfer, assignment or surrender of any right;

(f) a *financial supply;

(g) an entry into, or release from, an obligation:

(i) to do anything; or

(ii) to refrain from an act; or

(iii) to tolerate an act or situation;

(h) any combination of any 2 or more of the matters referred to in paragraphs (a) to (g).

(3) It does not matter whether it is lawful to do, to refrain from doing or to tolerate the act or situation constituting the supply.

(3A) For the avoidance of doubt, the delivery of:

(a) livestock for slaughtering or processing into *food; or

(b) game for processing into *food;

under an arrangement under which the entity making the delivery only relinquishes title after food has been produced, is the supply of the livestock or game (regardless of when the entity relinquishes title). The supply does not take place on or after the subsequent relinquishment of title.

(4) However, supply does not include:

(a) a supply of *money unless the money is provided as *consideration for a supply that is a supply of money or *digital currency; or

(b) a supply of digital currency unless the digital currency is provided as consideration for a supply that is a supply of digital currency or money.

9‑15 Consideration

(1) Consideration includes:

(a) any payment, or any act or forbearance, in connection with a supply of anything; and

(b) any payment, or any act or forbearance, in response to or for the inducement of a supply of anything.

(2) It does not matter whether the payment, act or forbearance was voluntary, or whether it was by the *recipient of the supply.

(2A) It does not matter:

(a) whether the payment, act or forbearance was in compliance with an order of a court, or of a tribunal or other body that has the power to make orders; or

(b) whether the payment, act or forbearance was in compliance with a settlement relating to proceedings before a court, or before a tribunal or other body that has the power to make orders.

(2B) For the avoidance of doubt, the fact that the supplier is an entity of which the *recipient of the supply is a member, or that the supplier is an entity that only makes supplies to its members, does not prevent the payment, act or forbearance from being consideration.

9‑17 Certain payments and other things not consideration

(1) If a right or option to acquire a thing is granted, then:

(a) the consideration for the supply of the thing on the exercise of the right or option is limited to any additional consideration provided either for the supply or in connection with the exercise of the right or option; or

(b) if there is no such additional consideration—there is no consideration for the supply.

(2) Making a gift to a non‑profit body is not the provision of consideration.

(3) A payment is not the provision of consideration if:

(a) the payment is made by a *government related entity to another government related entity for making a supply; and

(b) the payment is:

(i) covered by an appropriation under an *Australian law; or

(ii) made under the National Health Reform Agreement agreed to by the Council of Australian Governments on 2 August 2011, as amended from time to time; or

(iii) made under another agreement entered into to implement the National Health Reform Agreement; and

(c) the payment is calculated on the basis that the sum of:

(i) the payment (including the amounts of any other such payments) relating to the supply; and

(ii) anything (including any payment for any act or forbearance) that the other government related entity receives from another entity in connection with, or in response to, or for the inducement of, the supply, or for any other related supply;

does not exceed the supplier’s anticipated or actual costs of making those supplies.

(4) A payment is not the provision of consideration if the payment is made by a *government related entity to another government related entity and the payment is of a kind specified in regulations made for the purposes of this subsection.

(5) This section applies despite section 9‑15.

9‑20 Enterprises

(1) An enterprise is an activity, or series of activities, done:

(a) in the form of a *business; or

(b) in the form of an adventure or concern in the nature of trade; or

(c) on a regular or continuous basis, in the form of a lease, licence or other grant of an interest in property; or

(d) by the trustee of a fund that is covered by, or by an authority or institution that is covered by, Subdivision 30‑B of the *ITAA 1997 and to which deductible gifts can be made; or

(da) by a trustee of a *complying superannuation fund or, if there is no trustee of the fund, by a person who manages the fund; or

(e) by a charity; or

(g) by the Commonwealth, a State or a Territory, or by a body corporate, or corporation sole, established for a public purpose by or under a law of the Commonwealth, a State or a Territory; or

(h) by a trustee of a fund covered by item 2 of the table in section 30‑15 of the ITAA 1997 or of a fund that would be covered by that item if it had an ABN.

(2) However, enterprise does not include an activity, or series of activities, done:

(a) by a person as an employee or in connection with earning *withholding payments covered by subsection (4) (unless the activity or series is done in supplying services as the holder of an office that the person has accepted in the course of or in connection with an activity or series of activities of a kind mentioned in subsection (1)); or

Note: Acts done as mentioned in paragraph (a) will still form part of the activities of the enterprise to which the person provides work or services.

(b) as a private recreational pursuit or hobby; or

(c) by an individual (other than a trustee of a charitable fund, or of a fund covered by item 2 of the table in section 30‑15 of the ITAA 1997 or of a fund that would be covered by that item if it had an ABN), or a *partnership (all or most of the members of which are individuals), without a reasonable expectation of profit or gain; or

(d) as a member of a local governing body established by or under a *State law or *Territory law (except a local governing body to which paragraph 12‑45(1)(e) in Schedule 1 to the Taxation Administration Act 1953 applies).

(3) For the avoidance of doubt, the fact that activities of an entity are limited to making supplies to members of the entity does not prevent those activities:

(a) being in the form of a *business within the meaning of paragraph (1)(a); or

(b) being in the form of an adventure or concern in the nature of trade within the meaning of paragraph (1)(b).

(4) This subsection covers a *withholding payment covered by any of the provisions in Schedule 1 to the Taxation Administration Act 1953 listed in the table.

Withholding payments covered |

Item | Provision | Subject matter |

1 | Section 12‑35 | Payment to employee |

2 | Section 12‑40 | Payment to company director |

3 | Section 12‑45 | Payment to office holder |

4 | Section 12‑60 | Payment under labour hire arrangement, or specified by regulations |

9‑25 Supplies connected with the indirect tax zone

Supplies of goods wholly within the indirect tax zone

(1) A supply of goods is connected with the indirect tax zone if the goods are delivered, or made available, in the indirect tax zone to the *recipient of the supply.

Supplies of goods from the indirect tax zone

(2) A supply of goods that involves the goods being removed from the indirect tax zone is connected with the indirect tax zone.

Supplies of goods to the indirect tax zone

(3) A supply of goods that involves the goods being brought to the indirect tax zone is connected with the indirect tax zone if the supplier imports the goods into the indirect tax zone.

(3A) A supply of goods that is an *offshore supply of low value goods is connected with the indirect tax zone if it is connected with the indirect tax zone under Subdivision 84‑C.

Supplies of real property

(4) A supply of *real property is connected with the indirect tax zone if the real property, or the land to which the real property relates, is in the indirect tax zone.

Supplies of anything else

(5) A supply of anything other than goods or *real property is connected with the indirect tax zone if:

(a) the thing is done in the indirect tax zone; or

(b) the supplier makes the supply through an *enterprise that the supplier *carries on in the indirect tax zone; or

(c) all of the following apply:

(i) neither paragraph (a) nor (b) applies in respect of the thing;

(ii) the thing is a right or option to acquire another thing;

(iii) the supply of the other thing would be connected with the indirect tax zone; or

(d) the *recipient of the supply is an *Australian consumer.

Example: A holiday package for a trip to Queensland that is supplied by a travel operator in Japan will be connected with the indirect tax zone under paragraph (5)(c).

Note: A supply that is connected with the indirect tax zone under this subsection might be GST‑free if it is consumed outside the indirect tax zone: see section 38‑190. For more rules about supplies that are GST‑free, see Division 38.

Supplies of goods involving installation or assembly services

(6) If a supply of goods (other than a *luxury car) (the actual supply) involves the goods being brought to the indirect tax zone and the installation or assembly of the goods in the indirect tax zone, then the actual supply is to be treated as if it were 2 separate supplies in the following way:

(a) the part of the actual supply that involves the installation or assembly of the goods in the indirect tax zone is to be treated as if it were a separate supply of a thing done in the indirect tax zone;

(b) the remainder of the actual supply is to be treated as if it were a separate supply of goods involving the goods being brought to the indirect tax zone but not involving the installation or assembly of the goods.

Note 1: The paragraph (a) supply is connected with the indirect tax zone (see paragraph (5)(a)), unless item 1 or 2 of the table in section 9‑26 applies.

Note 2: The paragraph (b) supply may be a taxable supply (see subsection (3)), or there may be a taxable importation of the goods: see Division 13.

Note 3: For the price of the separate supplies, see subsection 9‑75(4).

Meaning of Australian consumer

(7) An entity is an Australian consumer of a supply made to the entity if:

(a) the entity is an *Australian resident (other than an entity that is an Australian resident solely because the definition of Australia in the *ITAA 1997 includes the external Territories); and

(b) the entity:

(i) is not *registered; or

(ii) if the entity is registered—the entity does not acquire the thing supplied solely or partly for the purpose of an *enterprise that the entity *carries on.

Note: Suppliers must take reasonable steps to ascertain whether recipients are Australian consumers: see section 84‑100.

9‑26 Supplies by non‑residents that are not connected with the indirect tax zone

(1) A supply is not connected with the indirect tax zone if:

(a) the supplier is a *non‑resident; and

(b) the supplier does not make the supply through an *enterprise that the supplier *carries on in the indirect tax zone; and

(c) the supply is covered by an item in this table:

Offshore supplies that are not connected with the indirect tax zone |

Item | Topic | These supplies are not connected with the indirect tax zone … |

1 | Inbound intangible supply | a supply of anything other than goods or *real property if: (a) the thing is done in the indirect tax zone; and (b) the *recipient is an *Australian‑based business recipient of the supply. |

2 | Intangible supply between non‑residents | a supply of anything other than goods or *real property if: (a) the thing is done in the indirect tax zone; and (b) the *recipient is a *non‑resident that acquires the thing supplied solely for the purpose of an *enterprise that the recipient *carries on outside the indirect tax zone. |

3 | Supply between non‑residents of leased goods | a supply by way of transfer of ownership of leased goods if: (a) the *recipient is a *non‑resident that does not acquire the thing supplied solely or partly for the purpose of an *enterprise that the recipient *carries on in the indirect tax zone; and (b) the lessee: (i) made a *taxable importation of the goods before the supply was made; and (ii) continues to lease the goods on substantially similar terms and conditions after the supply is made. |

4 | Supply by way of continued lease of goods from item 3 | a supply made by way of lease if: (a) the *recipient is the lessee referred to in paragraph (b) of item 3 of this table; and (b) the lease is the lease referred to in subparagraph (ii) of that paragraph. |

Note: This subsection does not apply to supplies made by a non‑resident through a resident agent if they have agreed it is not to apply: see section 57‑7.

(2) An entity is an Australian‑based business recipient of a supply made to the entity if:

(a) the entity is *registered; and

(b) an *enterprise of the entity is *carried on in the indirect tax zone; and

(c) the entity’s acquisition of the thing supplied is not solely of a private or domestic nature.

Note: If a supply is not connected with the indirect tax zone, the Australian‑based business recipient may be subject to a reverse charge: see Subdivision 84‑A.

(3) This section applies despite sections 9‑25 (which is about when supplies are connected with the indirect tax zone) and 85‑5 (which is about telecommunication supplies).

9‑27 When enterprises are carried on in the indirect tax zone

(1) An *enterprise of an entity is carried on in the indirect tax zone if:

(a) the enterprise is *carried on by one or more individuals covered by subsection (3) who are in the indirect tax zone; and

(b) any of the following applies:

(i) the enterprise is carried on through a fixed place in the indirect tax zone;

(ii) the enterprise has been carried on through one or more places in the indirect tax zone for more than 183 days in a 12 month period;

(iii) the entity intends to carry on the enterprise through one or more places in the indirect tax zone for more than 183 days in a 12 month period.

(2) It does not matter whether:

(a) the entity has exclusive use of a place; or

(b) the entity owns, leases or has any other claim or interest in relation to a place.

(3) This subsection covers the following individuals:

(a) if the entity is an individual—that individual;

(b) an employee or *officer of the entity;

(c) an individual who is, or is employed by, an agent of the entity that:

(i) has, and habitually exercises, authority to conclude contracts on behalf of the entity; and

(ii) is not a broker, general commission agent or other agent of independent status that is acting in the ordinary course of the agent’s business as such an agent.

9‑30 Supplies that are GST‑free or input taxed

GST‑free

(1) A supply is GST‑free if:

(a) it is GST‑free under Division 38 or under a provision of another Act; or

(b) it is a supply of a right to receive a supply that would be GST‑free under paragraph (a).

Input taxed

(2) A supply is input taxed if:

(a) it is input taxed under Division 40 or under a provision of another Act; or

(b) it is a supply of a right to receive a supply that would be input taxed under paragraph (a).

Note: If a supply is input taxed, there is no entitlement to an input tax credit for the things that are acquired or imported to make the supply (see sections 11‑15 and 15‑10).

Supplies that would be both GST‑free and input taxed

(3) To the extent that a supply would, apart from this subsection, be both *GST‑free and *input taxed:

(a) the supply is GST‑free and not input taxed, unless the provision under which it is input taxed requires the supplier to have chosen for its supplies of that kind to be input taxed; or

(b) the supply is input taxed and not GST‑free, if that provision requires the supplier to have so chosen.

Note: Subdivisions 40‑E (School tuckshops and canteens) and 40‑F (Fund‑raising events conducted by charities etc.) require such a choice.)

Supply of things used solely in connection with making supplies that are input taxed but not financial supplies

(4) A supply is taken to be a supply that is *input taxed if it is a supply of anything (other than *new residential premises) that you have used solely in connection with your supplies that are input taxed but are not *financial supplies.

9‑39 Special rules relating to taxable supplies

Chapter 4 contains special rules relating to taxable supplies, as follows:

Checklist of special rules |

Item | For this case ... | See: |

1A | Agents and insurance brokers | Division 153 |

1 | Associates | Division 72 |

2 | Cancelled lay‑by sales | Division 102 |

3 | Company amalgamations | Division 90 |

3A | Compulsory third party schemes | Division 79 |

4 | Deposits as security | Division 99 |

5 | Gambling | Division 126 |

5A | GST religious groups | Division 49 |

6 | Insurance | Division 78 |

7 | Offshore supplies | Division 84 |

8 | Payments of taxes, fees and charges | Division 81 |

8AA | Resident agents acting for non‑residents | Division 57 |

8A | Second‑hand goods | Division 66 |

8B | Settlement sharing arrangements | Division 80 |

9 | Supplies and acquisitions made on a progressive or periodic basis | Division 156 |

9A | Supplies in return for rights to develop land | Division 82 |

10 | Supplies in satisfaction of debts | Division 105 |

11 | Supplies partly connected with the indirect tax zone | Division 96 |

12 | Supply under arrangement covered by PAYG voluntary agreement | Division 113 |

12A | Tax‑related transactions | Division 110 |

13 | Telecommunication supplies | Division 85 |

14 | Vouchers | Division 100 |

Subdivision 9‑B—Who is liable for GST on taxable supplies?

9‑40 Liability for GST on taxable supplies

You must pay the GST payable on any *taxable supply that you make.

9‑69 Special rules relating to liability for GST on taxable supplies

Chapter 4 contains special rules relating to liability for GST on taxable supplies, as follows:

Checklist of special rules | |

Item | For this case ... | See: |

1 | Company amalgamations | Division 90 |

2 | GST groups | Division 48 |

3 | GST joint ventures | Division 51 |

4 | Offshore supplies | Division 84 |

4A | Non‑residents making supplies connected with the indirect tax zone | Division 83 |

4B | Representatives of incapacitated entities | Division 58 |

5 | Resident agents acting for non‑residents | Division 57 |

6 | Valuable metals | Division 86 |

Subdivision 9‑C—How much GST is payable on taxable supplies?

9‑70 The amount of GST on taxable supplies

The amount of GST on a *taxable supply is 10% of the *value of the taxable supply.

9‑75 The value of taxable supplies

(1) The value of a *taxable supply is as follows:

where:

price is the sum of:

(a) so far as the *consideration for the supply is consideration expressed as an amount of *money—the amount (without any discount for the amount of GST (if any) payable on the supply); and

(b) so far as the consideration is not consideration expressed as an amount of money—the *GST inclusive market value of that consideration.

Example: You make a taxable supply by selling a car for $22,000 in the course of carrying on an enterprise.

The value of the supply is:

The GST on the supply is therefore $2,000 (i.e. 10% of $20,000).

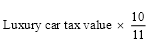

(2) However, if the taxable supply is of a *luxury car, the value of the taxable supply is as follows:

where:

luxury car tax value has the meaning given by section 5‑20 of the A New Tax System (Luxury Car Tax) Act 1999.

(3) In working out under subsection (1) the value of a *taxable supply made in a *tax period, being a supply that is a *fringe benefit, the price is taken to be the sum of:

(a) to the extent that, apart from this subsection, paragraph(a) of the definition of price in subsection (1) would be applicable:

(i) if the fringe benefit is a car fringe benefit—so much of the amount that would be worked out under that paragraph as represented the *recipient’s payment made in that period; or

(ii) if the fringe benefit is a benefit other than a car fringe benefit—so much of the amount that would be worked out under that paragraph as represented the *recipients contribution made in that period; and

(b) to the extent that, apart from this subsection, paragraph(b) of the definition of price in subsection (1) would be applicable:

(i) if the fringe benefit is a car fringe benefit—so much of the amount that would be worked out under that paragraph as represented the recipient’s payment made in that period; or

(ii) if the fringe benefit is a benefit other than a car fringe benefit—so much of the amount that would be worked out under that paragraph as represented the recipients contribution made in that period.

(4) Despite subsection (1), if a supply of goods (the actual supply) is to be treated as separate supplies because of subsection 9‑25(6) or 84‑79(2), then the price of each such separate supply is so much of the price of the actual supply, worked out under subsection (1), as reasonably represents the price of the separate supply.

9‑80 The value of taxable supplies that are partly GST‑free or input taxed

(1) If a supply (the actual supply) is:

(a) partly a *taxable supply; and

(b) partly a supply that is *GST‑free or *input taxed;

the value of the part of the actual supply that is a taxable supply is the proportion of the value of the actual supply that the taxable supply represents.

(2) The value of the actual supply, for the purposes of subsection (1), is as follows:

where:

taxable proportion is the proportion of the value of the actual supply that represents the value of the *taxable supply (expressed as a number between 0 and 1).

9‑85 Value of taxable supplies to be expressed in Australian currency

(1) For the purposes of this Act, the *value of a *taxable supply is to be expressed in Australian currency.

(2) In working out the *value of a *taxable supply, any amount of the *consideration for the supply that is expressed in:

(a) a currency other than Australian currency; or

(b) *digital currency;

is to be treated as if it were an amount of Australian currency worked out in the manner determined by the Commissioner.

9‑90 Rounding of amounts of GST

One taxable supply recorded on an invoice

(1) If the amount of GST on a *taxable supply that is the only taxable supply recorded on a particular *invoice would, apart from this section, be an amount that includes a fraction of a cent, the amount of GST is rounded to the nearest cent (rounding 0.5 cents upwards).

Several taxable supplies recorded on an invoice

(2) If 2 or more *taxable supplies are recorded on the same *invoice, the total amount of GST on the supplies is:

(a) what would be the amount of GST if it were worked out by:

(i) working out the GST on each of the supplies (without rounding the amounts to the nearest cent); and

(ii) adding the amounts together and, if the total is an amount that includes a fraction of a cent, rounding it to the nearest cent (rounding 0.5 cents upwards); or

(b) the amount worked out using the following method statement:

Method statement

Step 1. Work out, for each *taxable supply, what would, apart from this section, be the amount of GST on the supply.

Step 2. If the amount for the supply has more decimal places than the number of decimal places allowed by the accounting system used to work out the amount, round the amount (up or down as appropriate) to that number of decimal places.

Note: Subsection (4) gives further details of this rounding.

Step 3. Work out the sum of the amounts worked out under step 1 and (if applicable) step 2 for each supply.

Step 4. If the sum under step 3 includes a fraction of a cent, round the sum to the nearest cent (rounding 0.5 cents upwards).

(3) Whether to use paragraph (2)(a) or paragraph (2)(b) to work out the total amount of GST on the supplies is a matter of choice for:

(a) the supplier if the amount is being worked out to ascertain the supplier’s liability for GST; or

(b) the *recipient of the supplies if the amount is being worked out to ascertain the recipient’s entitlement to input tax credits.

(4) In applying step 2 of the method statement in subsection (2), if:

(a) the number of decimal places in the amount for the supply exceeds by one decimal place the number of decimal places allowed by the accounting system used to work out the amount; and

(b) the last digit of the amount (before rounding) is 5;

the amount is rounded upwards to that number of decimal places.

Taxable supplies divided into items

(5) If one or more *taxable supplies recorded on the same *invoice are divided into 2 or more items:

(a) subsection (1) does not apply; and

(b) subsection (2) applies as if each such item represented a separate taxable supply.

Taxable supplies recorded on documents other than invoices

(6) If one or more *taxable supplies, none of which are recorded on an *invoice, are recorded on a document that is not an invoice, this section applies as if the document were an invoice.

9‑99 Special rules relating to the amount of GST on taxable supplies

Chapter 4 contains special rules relating to the amount of GST on taxable supplies, as follows:

Checklist of special rules |

Item | For this case ... | See: |

1A | Agents and insurance brokers | Division 153 |

1 | Associates | Division 72 |

2 | Company amalgamations | Division 90 |

2A | Compulsory third party schemes | Division 79 |

3 | Gambling | Division 126 |

4 | Long‑term accommodation in commercial residential premises | Division 87 |

4AA | Non‑residents making supplies connected with the indirect tax zone | Division 83 |

4A | Offshore supplies | Division 84 |

5 | Sale of freehold interests etc. | Division 75 |

7 | Supplies partly connected with the indirect tax zone | Division 96 |

8 | Transactions relating to insurance policies | Division 78 |

8A | Valuable metals | Division 86 |

9 | Valuation of taxable supplies of goods in bond | Division 108 |

10 | Excess GST | Division 142 |

Note: There are other laws that may affect the amount of GST on taxable supplies. For example, see subsection 357‑60(3) in Schedule 1 to the Taxation Administration Act 1953 (about the effect of rulings made under Part 5‑5 in that Schedule).

Division 11—Creditable acquisitions

11‑1 What this Division is about

You are entitled to input tax credits for your creditable acquisitions. This Division defines creditable acquisitions, states who is entitled to the input tax credits and describes how to work out the input tax credits on acquisitions.

11‑5 What is a creditable acquisition?

You make a creditable acquisition if:

(a) you acquire anything solely or partly for a *creditable purpose; and

(b) the supply of the thing to you is a *taxable supply; and

(c) you provide, or are liable to provide, *consideration for the supply; and

(d) you are *registered, or *required to be registered.

11‑10 Meaning of acquisition

(1) An acquisition is any form of acquisition whatsoever.

(2) Without limiting subsection (1), acquisition includes any of these:

(a) an acquisition of goods;

(b) an acquisition of services;

(c) a receipt of advice or information;

(d) an acceptance of a grant, assignment or surrender of *real property;

(e) an acceptance of a grant, transfer, assignment or surrender of any right;

(f) an acquisition of something the supply of which is a *financial supply;

(g) an acquisition of a right to require another person:

(i) to do anything; or

(ii) to refrain from an act; or

(iii) to tolerate an act or situation;

(h) any combination of any 2 or more of the matters referred to in paragraphs (a) to (g).

(3) However, acquisition does not include:

(a) an acquisition of *money unless the money is provided as *consideration for a supply that is a supply of money or *digital currency; or

(b) an acquisition of digital currency unless the digital currency is provided as consideration for a supply that is a supply of digital currency or money.

11‑15 Meaning of creditable purpose

(1) You acquire a thing for a creditable purpose to the extent that you acquire it in *carrying on your *enterprise.

(2) However, you do not acquire the thing for a creditable purpose to the extent that:

(a) the acquisition relates to making supplies that would be *input taxed; or

(b) the acquisition is of a private or domestic nature.

(3) An acquisition is not treated, for the purposes of paragraph (2)(a), as relating to making supplies that would be *input taxed to the extent that the supply is made through an *enterprise, or a part of an enterprise, that you *carry on outside the indirect tax zone.

(4) An acquisition is not treated, for the purposes of paragraph (2)(a), as relating to making supplies that would be *input taxed if:

(a) the only reason it would (apart from this subsection) be so treated is because it relates to making *financial supplies; and

(b) you do not *exceed the financial acquisitions threshold.

(5) An acquisition is not treated, for the purposes of paragraph (2)(a), as relating to making supplies that would be *input taxed to the extent that:

(a) the acquisition relates to making a *financial supply consisting of a borrowing (other than through a *deposit account you make available); and

(b) the borrowing relates to you making supplies that are not input taxed.

11‑20 Who is entitled to input tax credits for creditable acquisitions?

You are entitled to the input tax credit for any *creditable acquisition that you make.

11‑25 How much are the input tax credits for creditable acquisitions?

The amount of the input tax credit for a *creditable acquisition is an amount equal to the GST payable on the supply of the thing acquired. However, the amount of the input tax credit is reduced if the acquisition is only *partly creditable.

Note: The basic rule for working out the GST payable on the supply is in Subdivision 9‑C. However, the GST payable may be affected by other provisions in:

(a) this Act (for a list of provisions, see section 9‑99); and

(b) other GST laws (for example, see subsection 357‑60(3) in Schedule 1 to the Taxation Administration Act 1953 (about the effect of rulings made under Part 5‑5 in that Schedule)).

11‑30 Acquisitions that are partly creditable

(1) An acquisition that you make is partly creditable if it is a *creditable acquisition to which one or both of the following apply:

(a) you make the acquisition only partly for a *creditable purpose;

(b) you provide, or are liable to provide, only part of the *consideration for the acquisition.

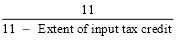

(3) The amount of the input tax credit on an acquisition that you make that is *partly creditable is as follows:

where:

extent of consideration is the extent to which you provide, or are liable to provide, the *consideration for the acquisition, expressed as a percentage of the total consideration for the acquisition.

extent of creditable purpose is the extent to which the *creditable acquisition is for a *creditable purpose, expressed as a percentage of the total purpose of the acquisition.

full input tax credit is what would have been the amount of the input tax credit for the acquisition if it had been made solely for a creditable purpose and you had provided, or had been liable to provide, all of the consideration for the acquisition.

(4) For the purpose of working out the extent of the *consideration, so far as the consideration is not expressed as an amount of *money, take into account the *GST inclusive market value of the consideration.

(5) The Commissioner may determine, in writing, one or more ways in which to work out, for the purpose of subsection (3), the extent to which a *creditable acquisition is for a *creditable purpose.

11‑99 Special rules relating to acquisitions

Chapter 4 contains special rules relating to acquisitions, as follows:

Checklist of special rules |

Item | For this case ... | See: |

1A | Agents and insurance brokers | Division 153 |

1B | Annual apportionment of creditable purpose | Division 131 |

1 | Associates | Division 72 |

2 | Company amalgamations | Division 90 |

2A | Compulsory third party schemes | Division 79 |

3 | Financial supplies (reduced credit acquisitions) | Division 70 |

3A | Fringe benefits provided by input taxed suppliers | Division 71 |

4 | Gambling | Division 126 |

5 | GST groups | Division 48 |

6 | GST joint ventures | Division 51 |

6A | GST religious groups | Division 49 |

7 | Insurance | Division 78 |

7A | Limited registration entities | Division 146 |

8 | Non‑deductible expenses | Division 69 |

8A | Offshore supplies | Division 84 |

9 | Pre‑establishment costs | Division 60 |

10 | Reimbursement of employees etc. | Division 111 |

10A | Representatives of incapacitated entities | Division 58 |

11 | Resident agents acting for non‑residents | Division 57 |

13 | Sale of freehold interests etc. | Division 75 |

14 | Second‑hand goods | Division 66 |

15 | Settlement sharing arrangements | Division 80 |

16 | Time limit on entitlements to input tax credits | Division 93 |

Part 2‑3—Importations

Division 13—Taxable importations

13‑1 What this Division is about

GST is payable on taxable importations. This Division defines taxable importations, states who is liable for the GST and describes how to work out the GST on importations.

Note 1: This Division applies whether or not you are registered.

Note 2: Things other than goods that are supplied overseas for use in the indirect tax zone (and are therefore in that sense “imported”) are not taxable importations, but they can attract GST under Subdivision 84‑A.

13‑5 What are taxable importations?

(1) You make a taxable importation if:

(a) goods are imported; and

(b) you enter the goods for home consumption (within the meaning of the Customs Act 1901).

However, the importation is not a taxable importation to the extent that it is a *non‑taxable importation.

Note: There is no registration requirement for taxable importations, and the importer need not be carrying on an enterprise.

(3) However, an importation of *money is not an importation of goods into the indirect tax zone.

13‑10 Meaning of non‑taxable importation

An importation is a non‑taxable importation if:

(a) it is a non‑taxable importation under Part 3‑2; or

(b) it would have been a supply that was *GST‑free or *input taxed if it had been a supply.

13‑15 Who is liable for GST on taxable importations?

You must pay the GST payable on any *taxable importation that you make.

13‑20 How much GST is payable on taxable importations?

(1) The amount of GST on the *taxable importation is 10% of the *value of the taxable importation.

(2) The value of a *taxable importation is the sum of:

(a) the *customs value of the goods imported; and

(b) the amount paid or payable:

(i) for the *international transport of the goods to their *place of consignment in the indirect tax zone; and

(ii) to insure the goods for that transport;

to the extent that the amount is not already included under paragraph (a); and

(ba) the amount paid or payable for a supply to which item 5A in the table in subsection 38‑355(1) applies, to the extent that the amount:

(i) is not an amount, the payment of which (or the discharging of a liability to make a payment of which), because of Division 81 or regulations made under that Division, is not the provision of *consideration; and

Note: Division 81 excludes certain taxes, fees and charges from the provision of consideration.

(ii) is not already included under paragraph (a) or (b); and

(c) any *customs duty payable in respect of the importation of the goods; and

(d) any *wine tax payable in respect of the *local entry of the goods.

(2A) If an amount to be taken into account under paragraph (2)(b) or (ba) is not an amount in Australian currency, the amount so taken into account is the equivalent in Australian currency of that amount, ascertained in the way provided in section 161J of the Customs Act 1901.

(3) The Commissioner may, in writing:

(a) determine the way in which the amount paid or payable for a specified kind of transport or insurance is to be worked out for the purposes of paragraph (2)(b); and

(b) determine the way in which the amount paid or payable for a specified kind of supply referred to in paragraph (2)(ba) is to be worked out for the purposes of that paragraph; and

(c) in relation to importations of a specified kind or importations to which specified circumstances apply—determine that:

(i) the amount paid or payable for a specified kind of transport or insurance is taken, for the purposes of paragraph (2)(b), to be zero; or

(ii) the amount paid or payable for a specified kind of supply referred to in paragraph (2)(ba) is taken, for the purposes of that paragraph, to be zero.

(4) For a *taxable importation that you make, you may choose to treat the amount under paragraph (2)(b), (or, if paragraph (2)(ba) applies, the sum of the amounts under paragraphs (2)(b) and (ba)), as an amount equal to:

(a) the percentage prescribed by the regulations of the *customs value of the goods imported; or

(b) if no percentage is prescribed—10% of their customs value.

(5) However, subsection (4) does not apply if:

(a) you are not *registered; or

(b) the *local entry of the goods is a *taxable dealing in relation to *wine; or

(c) the importation of the goods is a *taxable importation of a luxury car.

13‑25 The value of taxable importations that are partly non‑taxable importations

If an importation (the actual importation) is:

(a) partly a *taxable importation; and

(b) partly a *non‑taxable importation;

the value of the part of the actual importation that is a taxable importation is the proportion of the value of the actual importation (worked out as if it were solely a taxable importation) that the taxable importation represents.

13‑99 Special rules relating to taxable importations

Chapter 4 contains special rules relating to taxable importations, as follows:

Checklist of special rules |

Item | For this case ... | See: |

1 | GST groups | Division 48 |

2 | GST joint ventures | Division 51 |

3 | Importations without entry for home consumption | Division 114 |

4 | Representatives of incapacitated entities | Division 58 |

5 | Resident agents acting for non‑residents | Division 57 |

6 | Valuation of re‑imported goods | Division 117 |

Note: There are other laws that may affect the amount of GST on taxable importations. For example, see subsection 357‑60(3) in Schedule 1 to the Taxation Administration Act 1953 (about the effect of rulings made under Part 5‑5 in that Schedule).

Division 15—Creditable importations

15‑1 What this Division is about

You are entitled to input tax credits for your creditable importations. This Division defines creditable importations, states who is entitled to the input tax credits and describes how to work out the input tax credits on importations.

15‑5 What are creditable importations?

You make a creditable importation if:

(a) you import goods solely or partly for a *creditable purpose; and

(b) the importation is a *taxable importation; and

(c) you are *registered, or *required to be registered.

15‑10 Meaning of creditable purpose

(1) You import goods for a creditable purpose to the extent that you import the goods in *carrying on your *enterprise.

(2) However, you do not import the goods for a creditable purpose to the extent that:

(a) the importation relates to making supplies that would be *input taxed; or

(b) the importation is of a private or domestic nature.

(3) An importation is not treated, for the purposes of paragraph (2)(a), as relating to making supplies that would be *input taxed to the extent that the supply is made through an *enterprise, or a part of an enterprise, that you *carry on outside the indirect tax zone.

(4) An importation is not treated, for the purposes of paragraph (2)(a), as relating to making supplies that would be *input taxed if:

(a) the only reason it would (apart from this subsection) be so treated is because it relates to making *financial supplies; and

(b) you do not *exceed the financial acquisitions threshold.

(5) An importation is not treated, for the purposes of paragraph (2)(a), as relating to making supplies that would be *input taxed to the extent that:

(a) the importation relates to making a *financial supply consisting of a borrowing; and

(b) the borrowing relates to you making supplies that are not input taxed.

15‑15 Who is entitled to input tax credits for creditable importations?

You are entitled to the input tax credit for any *creditable importation that you make.

15‑20 How much are the input tax credits for creditable importations?

The amount of input tax credit for a *creditable importation is an amount equal to the GST payable on the importation. However, the amount of the input tax credit is reduced if the importation is only *partly creditable.

Note: The basic rule for working out the GST payable on the importation is in section 13‑20. However, the GST payable may be affected by other provisions in:

(a) this Act (for a list of provisions, see section 13‑99); and

(b) other GST laws (for example, see subsection 357‑60(3) in Schedule 1 to the Taxation Administration Act 1953 (about the effect of rulings made under Part 5‑5 in that Schedule)).

15‑25 Importations that are partly creditable

(1) An importation that you make is partly creditable if it is a *creditable importation that you make only partly for a *creditable purpose.

(3) The amount of the input tax credit on an importation that you make that is *partly creditable is as follows:

where:

extent of creditable purpose is the extent to which the importation is for a *creditable purpose, expressed as a percentage of the total purpose of the importation.

full input tax credit is what would have been the amount of the input tax credit for the importation if it had been made solely for a creditable purpose.

(4) The Commissioner may determine, in writing, one or more ways in which to work out, for the purpose of subsection (3), the extent to which an importation is for a *creditable purpose.

15‑99 Special rules relating to creditable importations

Chapter 4 contains special rules relating to creditable importations, as follows:

Checklist of special rules |

Item | For this case ... | See: |

1AA | Annual apportionment of creditable purpose | Division 131 |

1A | Fringe benefits provided by input taxed suppliers | Division 71 |

1 | GST groups | Division 48 |

2 | GST joint ventures | Division 51 |

2AA | Importations without entry for home consumption | Division 114 |

2A | Non‑deductible expenses | Division 69 |

3 | Pre‑establishment costs | Division 60 |

3A | Representatives of incapacitated entities | Division 58 |

4 | Resident agents acting for non‑residents | Division 57 |

Part 2‑4—Net amounts and adjustments

Division 17—Net amounts and adjustments

17‑1 What this Division is about

A net amount is worked out for each tax period that applies to you.

Adjustments can be made to the net amount. Increasing adjustments increase your net amount, and decreasing adjustments decrease your net amount.

Note: GST on taxable importations is not included in the net amount. It is dealt with separately under section 33‑15.

17‑5 Net amounts

(1) The net amount for a tax period applying to you is worked out using the following formula:

where:

GST is the sum of all of the GST for which you are liable on the *taxable supplies that are attributable to the tax period.

input tax credits is the sum of all of the input tax credits to which you are entitled for the *creditable acquisitions and *creditable importations that are attributable to the tax period.

Note 1: For the basic rules on what is attributable to a particular period, see Division 29.

Note 2: For further rules if you have excess GST for the period, see Division 142.

(2) However, the *net amount for the tax period:

(a) may be increased or decreased if you have any *adjustments for the tax period; and

(b) may be increased or decreased under Subdivision 21‑A of the *Wine Tax Act; and

(c) may be increased or decreased under Subdivision 13‑A of the A New Tax System (Luxury Car Tax) Act 1999.

Note 1: Under Subdivision 21‑A of the Wine Tax Act, amounts of wine tax increase the net amount, and amounts of wine tax credits reduce the net amount.

Note 2: Under Subdivision 13‑A of the A New Tax System (Luxury Car Tax) Act 1999, amounts of luxury car tax increase the net amount, and luxury car tax adjustments alter the net amount.

17‑10 Adjustments

If you have any *adjustments that are attributable to a tax period applying to you, alter your *net amount for the period as follows:

(a) add to the amount worked out under subsection 17‑5(1) for the period the sum of all the *increasing adjustments (if any) that are attributable to the period;

(b) subtract from that amount the sum of all the *decreasing adjustments (if any) that are attributable to the period.

For the basic rules on what adjustments are attributable to a particular period, see Division 29.

17‑20 Determinations relating to how to work out net amounts

(1) The Commissioner may make a determination that, in the circumstances specified in the determination, a *net amount for a tax period may be worked out to take account of other matters in the way specified in the determination.

(2) The matters must relate to correction of errors that were made in working out *net amounts for tax periods to which subsection (2A) applies.

(2A) This subsection applies to a *net amount for a tax period (the earlier tax period) if:

(a) the earlier tax period precedes the tax period mentioned in subsection (1); and

(b) the tax period mentioned in subsection (1) starts during the *period of review for the *assessment of the *net amount.

(3) If those circumstances apply in relation to a tax period applying to you, you may work out your *net amount for the tax period in that way.

17‑99 Special rules relating to net amounts or adjustments

Chapter 4 contains special rules relating to net amounts or adjustments, as follows:

Checklist of special rules |

Item | For this case ... | See: |

1A | Annual apportionment of creditable purpose | Division 131 |

1 | Anti‑avoidance | Division 165 |

2 | Cessation of registration | Division 138 |

3 | Changes in the extent of creditable purpose | Division 129 |

4 | Company amalgamations | Division 90 |

4AA | Compulsory third party schemes | Division 79 |

4A | Distributions from deceased estates | Division 139 |

5 | Gambling | Division 126 |

5A | Goods applied solely to private or domestic use | Division 130 |

6 | GST branches | Division 54 |

7 | GST groups | Division 48 |

8 | GST joint ventures | Division 51 |

8A | GST religious groups | Division 49 |

9 | Insurance | Division 78 |

9AA | Non‑deductible expenses | Division 69 |

9A | Non‑profit sub‑entities | Division 63 |

9B | Payment of GST by instalments | Division 162 |

9C | Providing additional consideration under gross‑up clauses | Division 133 |

10 | Representatives of incapacitated entities | Division 58 |

11 | Resident agents acting for non‑residents | Division 57 |

11A | Sale of freehold interests etc. | Division 75 |

12 | Second‑hand goods | Division 66 |

12AA | Settlement sharing arrangements | Division 80 |

12A | Simplified accounting methods for retailers and small enterprise entities | Division 123 |

12B | Stock on hand on becoming registered etc. | Division 137 |

13 | Supplies in satisfaction of debts | Division 105 |

14 | Supplies of going concerns | Division 135 |

15 | Supplies of things acquired etc. without full input tax credits | Division 132 |

15A | Third party payments | Division 134 |

16 | Tradex scheme goods | Division 141 |

17 | Vouchers | Division 100 |

Division 19—Adjustment events

Table of Subdivisions

19‑A Adjustment events

19‑B Adjustments for supplies

19‑C Adjustments for acquisitions

19‑1 What this Division is about

Adjustments can arise because of adjustment events. They are events such as a cancellation of a supply or acquisition, or a change in the consideration for a supply or acquisition (for example, because of a volume discount).

Note: Importations do not give rise to adjustment events.

19‑5 Explanation of the effect of adjustment events

The following diagram shows how an *adjustment event for a supply or acquisition can give rise to an *increasing adjustment or a *decreasing adjustment.

Note: This section is an explanatory section.

Subdivision 19‑A—Adjustment events

19‑10 Adjustment events

(1) An adjustment event is any event which has the effect of:

(a) cancelling a supply or acquisition; or

(b) changing the *consideration for a supply or acquisition; or

(c) causing a supply or acquisition to become, or stop being, a *taxable supply or *creditable acquisition.

Example: If goods that are supplied for export are not exported within the time provided in section 38‑185, the supply is likely to become a taxable supply after originally being a supply that was GST‑free.

(2) Without limiting subsection (1), these are *adjustment events:

(a) the return to a supplier of a thing, or part of a thing, supplied (whether or not the return involves a change of ownership of the thing);

(b) a change to the previously agreed *consideration for a supply or acquisition, whether due to the offer of a discount or otherwise;

(c) a change in the extent to which an entity that makes an acquisition provides, or is liable to provide, consideration for the acquisition (unless the entity *accounts on a cash basis).

(3) An *adjustment event:

(a) can arise in relation to a supply even if it is not a *taxable supply; and

(b) can arise in relation to an acquisition even if it is not a *creditable acquisition.

(4) However, the return of a thing supplied, or part of a thing supplied, to its supplier is not an *adjustment event if the return is for the purpose of repair or maintenance.

Subdivision 19‑B—Adjustments for supplies

19‑40 Where adjustments for supplies arise

You have an adjustment for a supply for which you are liable to pay GST (or would be liable to pay GST if it were a *taxable supply) if:

(a) in relation to the supply, one or more *adjustment events occur during a tax period; and

(b) GST on the supply was attributable to an earlier tax period (or, if the supply was not a taxable supply, would have been attributable to an earlier tax period had the supply been a taxable supply); and

(c) as a result of those adjustment events, the *previously attributed GST amount for the supply (if any) no longer correctly reflects the amount of GST (if any) on the supply (the corrected GST amount), taking into account any change of circumstances that has given rise to an adjustment for the supply under this Subdivision or Division 21 or 134.

19‑45 Previously attributed GST amounts

The previously attributed GST amount for a supply is:

(a) the amount of any GST that was attributable to a tax period in respect of the supply; plus

(b) the sum of any *increasing adjustments, under this Subdivision or Division 21, that were previously attributable to a tax period in respect of the supply; minus

(c) the sum of any *decreasing adjustments, under this Subdivision or Division 21 or 134, that were previously attributable to a tax period in respect of the supply.

19‑50 Increasing adjustments for supplies

If the *corrected GST amount is greater than the *previously attributed GST amount, you have an increasing adjustment equal to the difference between the corrected GST amount and the previously attributed GST amount.

19‑55 Decreasing adjustments for supplies

If the *corrected GST amount is less than the *previously attributed GST amount, you have a decreasing adjustment equal to the difference between the previously attributed GST amount and the corrected GST amount.

Subdivision 19‑C—Adjustments for acquisitions

19‑70 Where adjustments for acquisitions arise

(1) You have an adjustment for an acquisition for which you are entitled to an input tax credit (or would be entitled to an input tax credit if the acquisition were a *creditable acquisition) if:

(a) in relation to the acquisition, one or more *adjustment events occur during a tax period; and

(b) an input tax credit on the acquisition was attributable to an earlier tax period (or, if the acquisition was not a creditable acquisition, would have been attributable to an earlier tax period had the acquisition been a creditable acquisition); and

(c) as a result of those adjustment events, the *previously attributed input tax credit amount for the acquisition (if any) no longer correctly reflects the amount of the input tax credit (if any) on the acquisition (the corrected input tax credit amount).

(2) In working out the *corrected input tax credit amount for the acquisition:

(a) take into account any change of circumstances that has given rise to an adjustment for the acquisition under this Subdivision or Division 21, 129, 133 or 134; and

(b) if an adjustment relating to the acquisition under Division 131 was attributable to an earlier tax period:

(i) do not take into account that adjustment; and

(ii) treat the acquisition as one in relation to which Division 131 had not applied.

19‑75 Previously attributed input tax credit amounts

The previously attributed input tax credit amount for an acquisition is:

(a) the amount of any input tax credit that was attributable to a tax period in respect of the acquisition; minus

(b) the sum of any *increasing adjustments, under this Subdivision or Division 21, 129, 131 or 134, that were previously attributable to a tax period in respect of the acquisition; plus

(c) the sum of any *decreasing adjustments, under this Subdivision or Division 21, 129 or 133, that were previously attributable to a tax period in respect of the acquisition.

19‑80 Increasing adjustments for acquisitions

If the *previously attributed input tax credit amount is greater than the *corrected input tax credit amount, you have an increasing adjustment equal to the difference between the previously attributed input tax credit amount and the corrected input tax credit amount.

19‑85 Decreasing adjustments for acquisitions

If the *previously attributed input tax credit amount is less than the *corrected input tax credit amount, you have a decreasing adjustment equal to the difference between the corrected input tax credit amount and the previously attributed input tax credit amount.

19‑99 Special rules relating to adjustment events

Chapter 4 contains special rules relating to *adjustment events in particular cases, as follows:

Checklist of special rules |

Item | For this case ... | See: |

1AA | Compulsory third party schemes | Division 79 |

1AB | Excess GST and cancelled supplies | Division 142 |

1A | GST religious groups | Division 49 |

1 | Insurance | Division 78 |

2 | Non‑deductible expenses | Division 69 |

2A | Providing additional consideration under gross‑up clauses | Division 133 |

3 | Settlement sharing arrangements | Division 80 |

4 | Third party payments | Division 134 |

Division 21—Bad debts

21‑1 What this Division is about

If debts are written off as bad or are outstanding after 12 months, adjustments (for the purpose of working out net amounts) are made. They can arise both for amounts written off or outstanding and for recovery of amounts previously written off or outstanding.

Note: This Division does not apply to supplies and acquisitions that you account for on a cash basis (except in the limited circumstances referred to in Division 159).

21‑5 Writing off bad debts (taxable supplies)

(1) You have a decreasing adjustment if:

(a) you made a *taxable supply; and

(b) the whole or part of the *consideration for the supply has not been received; and

(c) you write off as bad the whole or a part of the debt, or the whole or a part of the debt has been *overdue for 12 months or more.

The amount of the decreasing adjustment is 1/11 of the amount written off, or 1/11 of the amount that has been overdue for 12 months or more, as the case requires.

(2) However, you cannot have an *adjustment under this section if you *account on a cash basis.

21‑10 Recovering amounts previously written off (taxable supplies)

You have an increasing adjustment if:

(a) you made a *taxable supply in relation to which you had a *decreasing adjustment under section 21‑5 for a debt; and

(b) you recover the whole or a part of the amount written off, or the whole or a part of the amount that has been *overdue for 12 months or more, as the case requires.

The amount of the increasing adjustment is 1/11 of the amount recovered.

21‑15 Bad debts written off (creditable acquisitions)

(1) You have an increasing adjustment if:

(a) you made a *creditable acquisition for *consideration; and

(b) the whole or part of the consideration is *overdue, but you have not provided the consideration overdue; and

(c) the supplier of the thing you acquired writes off as bad the whole or a part of the debt, or the whole or a part of the debt has been overdue for 12 months or more.

The amount of the increasing adjustment is 1/11 of the amount written off, or 1/11 of the amount that has been overdue for 12 months or more, as the case requires.

(2) However, you cannot have an *adjustment under this section if you *account on a cash basis.

21‑20 Recovering amounts previously written off (creditable acquisitions)

You have a decreasing adjustment if:

(a) you made a *creditable acquisition in relation to which you had an *increasing adjustment under section 21‑15 for a debt; and

(b) you pay to the supplier of the thing you acquired the whole or a part of the amount written off, or the whole or a part of the amount that has been *overdue for 12 months or more, as the case requires.

The amount of the decreasing adjustment is 1/11 of the amount recovered.

21‑99 Special rules relating to adjustments for bad debts

Chapter 4 contains special rules relating to adjustments for bad debts, as follows:

Checklist of special rules |

Item | For this case ... | See: |

1A | Bad debts relating to transactions that are not taxable or creditable to the fullest extent | Division 136 |

1 | Changing your accounting basis | Division 159 |

2 | Gambling | Division 126 |

2A | Representatives of incapacitated entities | Division 58 |

3 | Sale of freehold interests etc. | Division 75 |

Part 2‑5—Registration

Division 23—Who is required to be registered and who may be registered

23‑1 Explanation of Division

This diagram shows when you are required to be, and when you may, be registered.

Note: This section is an explanatory section.

23‑5 Who is required to be registered

You are required to be registered under this Act if:

(a) you are *carrying on an *enterprise; and

(b) your *GST turnover meets the *registration turnover threshold.

Note: It is the entity that carries on the enterprise that is required to be registered (and not the enterprise).

23‑10 Who may be registered

(1) You may be *registered under this Act if you are carrying on an *enterprise (whether or not your *GST turnover is at, above or below the *registration turnover threshold).

(2) You may be *registered under this Act if you intend to carry on an *enterprise from a particular date.

23‑15 The registration turnover threshold

(1) Your registration turnover threshold (unless you are a non‑profit body) is:

(a) $50,000; or

(b) such higher amount as the regulations specify.

(2) Your registration turnover threshold if you are a non‑profit body is:

(a) $100,000; or

(b) such higher amount as the regulations specify.

23‑20 Not registered for 4 years

Despite section 23‑5, you are treated as not having been *required to be registered under this Act on a day if your *registration could not take effect from that day because of subsection 25‑10(1A).

Note: Subsection 25‑10(1A) provides that the date of effect of your registration must not be a day that occurred more than 4 years before the day of the Commissioner’s decision to register you, unless the Commissioner is of the opinion there has been fraud or evasion.

23‑99 Special rules relating to who is required to be registered or who may be registered

Chapter 4 contains special rules relating to who is *required to be registered, or who may be *registered, as follows:

Checklist of special rules |

Item | For this case ... | See: |

1A | Government entities | Division 149 |

1B | Non‑profit sub‑entities | Division 63 |

1 | Representatives of incapacitated entities | Division 58 |

2 | Resident agents acting for non‑residents | Division 57 |

3 | Taxis | Division 144 |

Division 25—How you become registered, and how your registration can be cancelled

Table of Subdivisions

25‑A How you become registered

25‑B How your registration can be cancelled

Subdivision 25‑A—How you become registered

25‑1 When you must apply for registration

You must apply, in the *approved form, to be *registered under this Act if:

(a) you are not registered under this Act; and

(b) you are *required to be registered.

You must make your application within 21 days after becoming required to be registered.

25‑5 When the Commissioner must register you

(1) The Commissioner must *register you if:

(a) you have applied for registration in an *approved form; and

(b) the Commissioner is satisfied that you are *carrying on an *enterprise, or you intend to carry on an enterprise from a particular date specified in your application.

Note: Refusing to register you under this subsection is a reviewable GST decision (see Subdivision 110‑F in Schedule 1 to the Taxation Administration Act 1953).

(2) The Commissioner must *register you (even if you have not applied for registration) if the Commissioner is satisfied that you are *required to be registered.

Note: Registering you under this subsection is a reviewable GST decision (see Subdivision 110‑F in Schedule 1 to the Taxation Administration Act 1953).

(3) The Commissioner must notify you in writing of any decision he or she makes in relation to you under this section. If the Commissioner decides to register you, the notice must specify the following:

(a) the date of effect of your registration;

(b) your registration number;

(c) the tax periods that apply to you.

25‑10 The date of effect of your registration

(1) The Commissioner must decide the date from which your *registration takes effect, or took effect. However:

(a) if you did not apply for registration and the Commissioner is satisfied that you are *required to be registered—the date of effect must not be a day before the day on which you became required to be registered; or

(b) if you applied for registration—the date of effect must not be a day before:

(i) the day specified in your application; or

(ii) if the Commissioner is satisfied that you became required to be registered on an earlier day—the day that the Commissioner is satisfied is that earlier day; or

(c) if you are being registered only because you intend to *carry on an *enterprise—the date of effect must not be a day before the day specified, in your application for registration, as the day from which you intend to carry on the enterprise.

Note: Deciding the date of effect of your registration is a reviewable GST decision (see Subdivision 110‑F in Schedule 1 to the Taxation Administration Act 1953).

(1A) The date of effect must not be a day that occurred more than 4 years before the day of the decision, unless the Commissioner is of the opinion there has been fraud or evasion.

(2) The *Australian Business Registrar must enter in the *Australian Business Register the date on which your *registration takes or took effect.

25‑15 Effect of backdating your registration

If the Commissioner decides under section 25‑10, as the date of effect of your *registration (your registration day), a day before the day of the decision, then you are taken:

(a) for the purpose of determining whether a supply you made on or after your registration day was a *taxable supply; and

(b) for the purpose of determining whether an acquisition you made on or after that day was a *creditable acquisition; and

(c) for the purpose of determining whether an importation you made on or after that day was a *creditable importation;

to have been registered from and including your registration day.

Note: This section ensures that backdating your registration enables your supplies and acquisitions made on or after the date of effect to be picked up by the GST system. Section 25‑10 limits the extent to which your registration can be backdated.

25‑49 Special rules relating to registration

Chapter 4 contains special rules relating to *registration in particular cases, as follows:

Checklist of special rules |

Item | For this case ... | See: |

1A | Government entities | Division 149 |

1 | GST branches | Division 54 |

1AA | Limited registration entities | Division 146 |

2 | Non‑profit sub‑entities | Division 63 |

3 | Non‑residents making supplies connected with the indirect tax zone | Division 83 |

Subdivision 25‑B—How your registration can be cancelled

25‑50 When you must apply for cancellation of registration

If you are *registered and you are not *carrying on any *enterprise, you must apply to the Commissioner in the *approved form for cancellation of your *registration. You must lodge your application within 21 days after the day on which you ceased to be carrying on any *enterprise.

25‑55 When the Commissioner must cancel registration

(1) The Commissioner must cancel your *registration if:

(a) you have applied for cancellation of registration in the *approved form; and

(b) at the time you applied for cancellation of registration, you had been registered for at least 12 months; and

(c) the Commissioner is satisfied that you are not *required to be registered.

Note: Refusing to cancel your registration under this subsection is a reviewable GST decision (see Subdivision 110‑F in Schedule 1 to the Taxation Administration Act 1953).

(2) The Commissioner must cancel your *registration (even if you have not applied for cancellation of your registration) if:

(a) the Commissioner is satisfied that you are not *carrying on an *enterprise; and

(b) the Commissioner believes on reasonable grounds that you are not likely to carry on an enterprise for at least 12 months.

Note: Cancelling your registration under this subsection is a reviewable GST decision (see Subdivision 110‑F in Schedule 1 to the Taxation Administration Act 1953).